US ISM Manufacturing PMI May Preview: Gloom persists despite an US expanding economy

- PMI forecast to slip to 54.5 from 55.4, new orders expected to rise to 53.6.

- Markets monitoring US economy for signs of inflation’s impact on consumers.

- S&P Global May manufacturing PMI was as forecast, services weaker.

- Treasury yields, equities and the dollar vulnerable to poor ISM results.

All eyes are on the US economy, alert for signs that businesses are beginning to feel the impact of an inflation-weakened US consumer on their bottom line.

The Purchasing Managers’ Index (PMI) for manufacturing from the Institute for Supply Management (ISM) is expected to slip to 54.5 in May from 55.4. The New Orders Index is forecast to rise to 53.6 from 53.5 and the Employment Index should reach 53.6 from 50.9. Prices are predicted to climb to 86.2 from 84.6 in April.

In April, overall PMI fell from its recent high in February of 58.6. New Orders had faded from 61.7 in the same month and employment was down from 56.3 in March, its best level since 57.7 a year earlier.

Inflation, consumer spending and the saving rate

Inflation has been taking an ever-increasing bite of US wages for more than a year. With the Consumer Price Index at 8.3% annually in April, the headline Personal Consumption Expenditure Price Index (PCE) at 6.3% and the core rate at 4.9%, the purchasing power of wages declined 2.6% in April and 2.7% in March. Salaries have been losing ground to inflation for 14 months.

CPI

While Retail Sales and Personal Spending, the two main gauges of consumption, have been relatively stable, consumers have been forced to dig deep into savings in order to maintain their purchasing habits. The US saving rate fell to 4.4% in April, the lowest since 2008, according to a Commerce Department report.

Almost two-thirds of US economic activity is tied to the consumer. It is an open question how long families and households will continue to deplete their savings. To put it another way, unless either wages rise or inflation falls, people will soon be forced to reduce discretionary spending in order to maintain the necessities, food, shelter and transportation, all of which have increased in price more than the general inflation rates. When that shift occurs, it should be readily apparent in the New Orders Index.

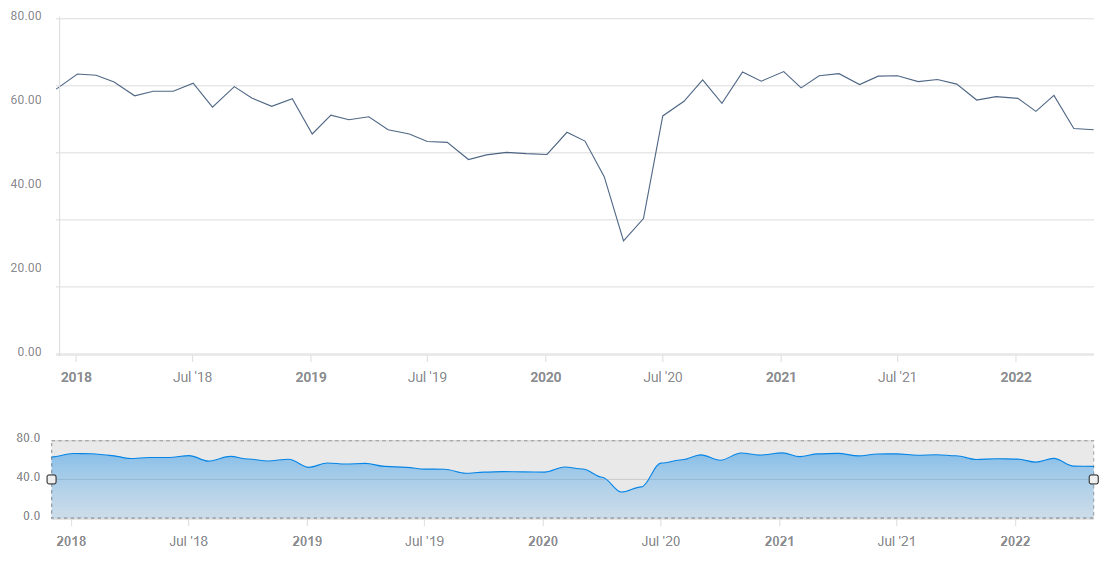

New Orders PMI

The New Orders Index reached its post-lockdown peak at 67.4, an all-time record, in December 2021 almost two years after the government ordered shutdown upended the US economy. For 15 months in the recovery, from October 2020 to December 2021, the index averaged 64.8, its highest sustained performance in the series history. This year, however, the index has dropped sharply, falling to 57.9 in January, recovering to 61.7 in February but plunging to 53.5 in April. The projected mimimal increase to 53.6 in May would leave the index at its lowest level since the nadir of the 2020 economic collapse in April and May 2020.

The drastic drop in new orders in the last four months suggests that the US consumer has already begun to pullback on discretionary spending for factory goods. Manufacturing is considered a leading indicator for the economy as a whole. The decline does not bode well for second quarter growth.

New Orders PMI

FXStreet

Federal Reserve

The Federal Reserve’s newly minted inflation policy is expected to hike the fed funds rate by an additional 200 basis points to 3.0% by the end of the year, now just seven months distant.

The US economy contracted 1.5% in the first three months. Second quarter growth is running at 1.9% in the Atlanta Fed GDPNow estimate with one month to go.

Rate increases are designed to curb inflation by reducing economic growth. Can the Fed maintain its hard line against inflation if the US economy slips into a traditional recession in the second quarter?

The answer to that question will not be known until GDP is reported in late July, after the next two Fed meetings. A 50 basis point increase is expected on June 15 and again on July 27.

It will be the US consumer who determines second quarter growth. At the moment it appears Americans have decided on the optimistic course, hoping for economic improvement. May Retail Sales will be released on June 15 and Personal Spending on June 30.

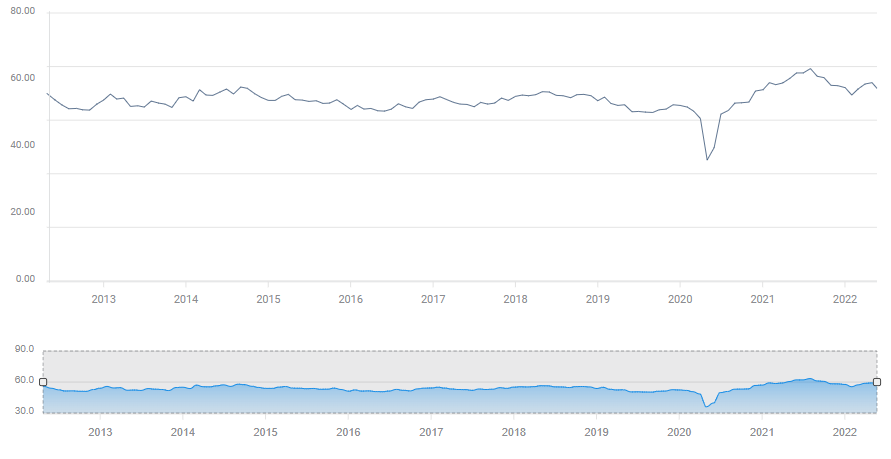

S&P Global PMI

Indexes for May from S&P Global came in as expected for the service sector at 57.5, though down from 59.2 in April. Manufacturing PMI was lower at 53.5 than the 55.2 forecast and April’s 55.6 reading. The Composite Index dropped to 53.8 from 56.0.

The services index has been lower than manufacturing over the past six months, and both have bounced around but neither have exhibited a negative trend.

S&P Global Manufacturing PMI

Market Conclusion

Markets are primed for negative economic US news that has not yet arrived.

Equities are flirting with bear market averages, concerned that inflation will force the US consumer to curtail spending precipitating a recession. Or, that Fed rate increases will push a feeble economy into a decline. There is, as yet, little evidence for either theory, but that has not dissuaded the credit, equity and currency markets from speculating on the outcome.

Treasury yields have fallen from their early May highs as credit markets have factored in the impending inflationary drag on consumption. The dollar has been sold as Treasury yields peaked and then reversed. Earlier safety trade flows to the greenback have been withdrawn as the Ukraine war has subsided into stalemate and its immediate threat to the global economy has waned.

Market risk for the ISM manufacturing report, especially focused on the orders index, is heavily on the downside as a poor results will tend to confirm existing fears. If orders fall below 50 into contraction, it will reinforce the short positions already taken in equities, Treasury yields and the dollar.

Readings at or better than forecast will do little to improve the market's economic outlook. While better PMI results will mitigate immediate fears, they cannot on their own, provide confidence in the future. Traders require proof of a strengthening recovery in order to abandon the current negative trends.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.