US Initial Jobless Claims Preview: Running on parallel tracks

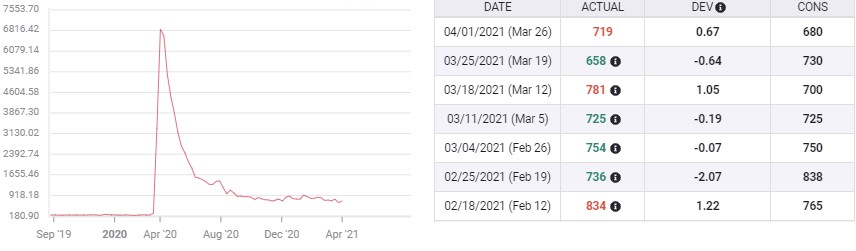

- Initial Jobless claims forecast to dip to 680,000 in the April 2 week from 719,000.

- Continuing Claims should fall to 3.65 million from 3.794 million.

- Nonfarm Payrolls had an exceptional March and an excellent first quarter.

- Payrolls and claims seem to report on two different economies.

- Markets have demoted the importance of Initial Claims.

The American job market shifted into overdrive in March, giving more new people a regular paycheck than any time since last August, yet three times as many filed for unemployment claims as the fallout from the pandemic lockdowns continues to upend lives.

Initial Jobless claims are forecast to drop to 680,000 in the April 2 week from 719,000 prior. Continuing Claims are expected to fall to 3.65 million in the March 26 week from 3.794 million.

Initial Jobless Claims

The incongruity of large numbers of hirees and layoffs at the same time has become a commonplace in the past 13 months. While the US labor economy is creating jobs at an exceptional clip, small businesses, especially in the restaurant and retail sectors in cities continue to fail as they reach the end of their resources, keeping the unemployment rolls high.

Nonfarm Payrolls and PMI

Employers added 916,000 workers in March, almost double the 468,000 in February and far ahead of the 647,000 forecast. Revisions to the first two months of the year increased their totals by another 156,000, bringing the quarter to 1.617 million.

The December loss of 306,000 in the renewed California lockdown is history as the vast majority of the country has reopened, encouraged by the waning pandemic and vaccination rates that are among the best in the world.

Businesses are as optimistic as their customers and employees. The Manufacturing Purchasing Managers Index (PMI) from the Institute for Supply Management scored 64.7 in March, its highest reading in 38 years. The Services PMI at 63.7 was the highest in the series history.

Employment Indexes in both polls were equally and unexpectedly, strong.

Consumer Confidence

The most important factor in consumer sentiment is employment and the March figures from the Conference Board and the University of Michigan reflect the robust hiring.

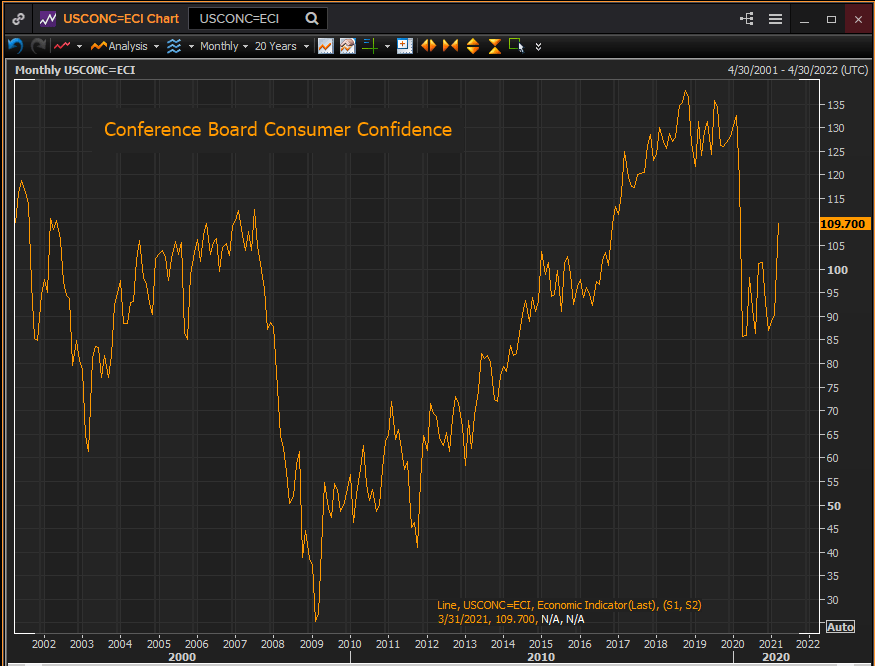

The Conference Board (CB) Consumer Confidence Index rose to 109.7 in March from February’s 91.3. The consensus prediction was 96.9. Consumer outlook in March was at its highest level since the onset of the pandemic and is about half-way between the February 2020 score of 132.6 and the April panic low of 85.7.

Reuters

Separate CB gauges for the Present Situation and Expectations also increased last month to 110.0 from 89.6 and to 109.6 from 90.9 respectively.

The Michigan Consumer Sentiment Survey rose to 84.9 in March, its highest score in a year, from 76.8 in February. The forecast had been 78.5. This index is also about half-way between its February 2020 reading of 101 and the April low at 71.8.

Americans would not be rating the improvement in the economy and their own personal financial situation so highly if they did not see an active jobs recovery.

Conclusion

The slow and somewhat disappointing improvement in Initial Claims is an indicator of the long-term damage wrought by the economic lockdown approach to the pandemic. Jobs losses continue at high levels because life has not returned to normal in several sectors of the economy and in many urban areas.

However, unemployment claims are no longer an indicator of the direction of the overall economy which is recovering employment at a remarkable pace.

Losing one’s job is a personal hardship. It is no longer an economic symbol.

Whether the claims number is higher, lower or as expected, markets have moved on and will pay it no more attention than they do to another expired favorite, the international trade balance.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.