US Initial Jobless Claims Preview: Marking time on the bottom

- Initial claims at 2.5 million will be the lowest in two months.

- Continuing claims to rise 2.4 million to 25.1 million.

- Claims filings will total 36 million in eight weeks.

- Business closures and social restrictions are still prevalent in many states.

- Claims will not have market impact unless substantially different that forecast.

Even while many states are beginning to ease the restrictions that have crippled the US economy and created the greatest surge in unemployment since the Depression the damage already done to the labor market continues to mount with each passing week.

Initial jobless claims are forecast to rise 2.5 million the May 8 week bringing the total since layoffs began in earnest on March 21 to 35.983 million, or 21.8% of the US labor force. Continuing claims are predicted to climb to 25.1 million from 22.647.

New filings peaked in the second week of the pandemic layoffs, March 28 at 6.867 million and will have fallen 63.5% if the Thursday estimate is correct.

Markets and labor statistics

April payrolls and unemployment rate, as other-otherworldly as they were at -20.5 million and 14.7%, brought almost no reaction from the currency, equities or credit markets when they were released on May 8.

The by now well limned labor market disaster from the coronavirus shutdown of large portions of the US economy has been priced into trading levels of all markets for many weeks. Unless statistics bring news of further deterioration market attention will remain focused on the attempts by several states and countries to restart their moribund economies.

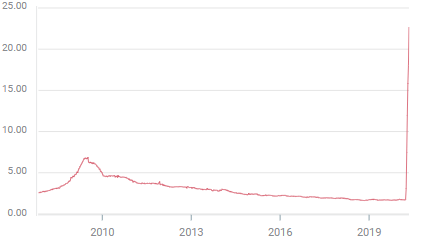

Continuing claims

The continuing claims numbers run one week behind initial filings and give a slightly different view of the number of people who are receiving government assistance.

There are several reasons that the numbers on the continuing rolls are less than the total initial claims filings.

Most unemployment insurance runs for 26 weeks, people drop from the rolls as their eligibility expires. In early March before the layoffs began there were 1.7 million receiving unemployment insurance. Some portion of those have left as their six months ran out. People who find new jobs are automatically removed, in addition not everyone who applies for jobless benefits--the initial claims number--qualifies.

If the states that are lifting business restrictions are successful in bringing people back to work improvement will surface here before it registers in non-farm payrolls. The first week that initial claims goes up and continuing claims fall will be one sign that the recovery has started.

Continuing claims

Conclusion

Markets are fully priced on the labor market catastrophe of the coronavirus shutdowns.

What has not been priced is the shape and speed of the recovery, or in the worst caste, a deeper economic collapse. Risk-aversion remains the basic scenario for the dollar until there is a concrete sign of recovery. So far there have been none.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.