US Fourth Quarter GDP Final Revision Preview: “This is a very different animal than the Great Depression”

- Economic activity expected to be unchanged at 2.1% after the third revision.

- Growth averaged 2.4% across the first three quarters.

- Ben Bernanke compares Coronavirus to a natural disaster but not the Depression.

The Bureau of Economic Analysis (BEA) , a division of the Commerce Department will release its third and final figure for gross domestic product (GDP) in the fourth quarter on Thursday, March 26 at 12:30 GMT, 8:30 EDT.

Forecast

Annualized GDP is predicted to be unchanged at 2.1%. Last year the economy expanded 3.1% in the first quarter, 2.0% in the second, and 2.1% in the third. The initial estimate for the first quarter of 2020 will be issued by the BEA on April 29.

US economy in 2019

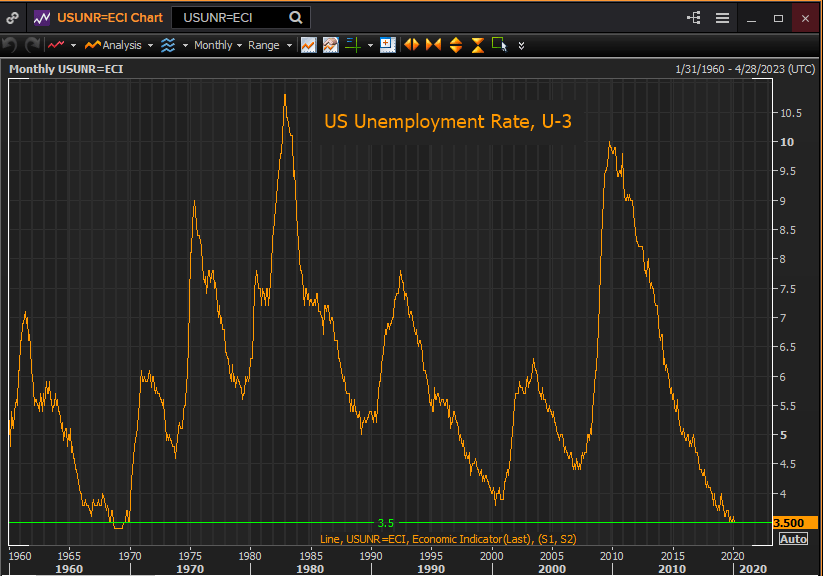

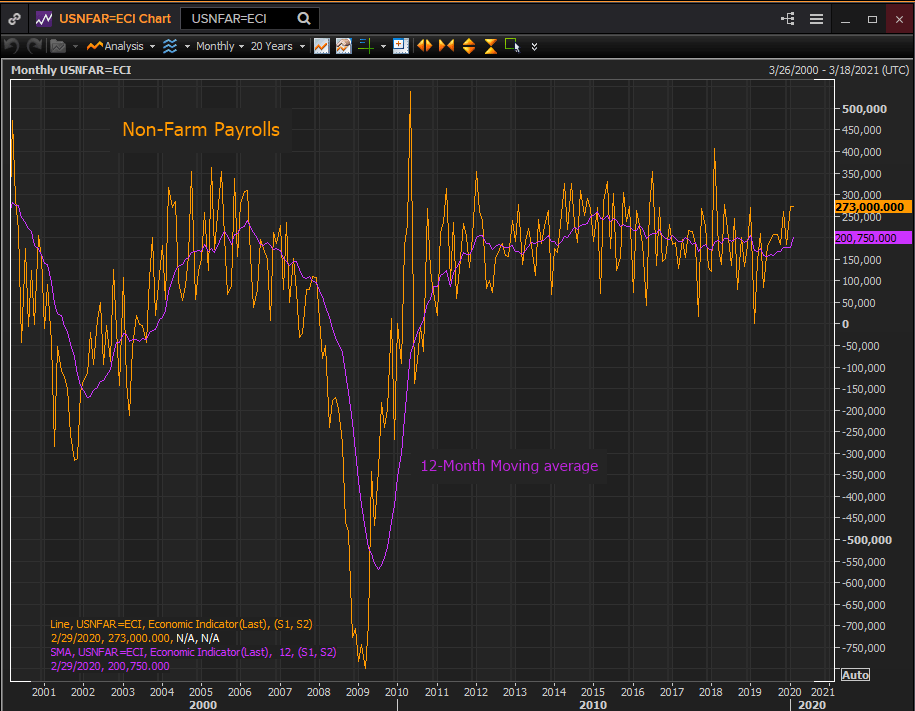

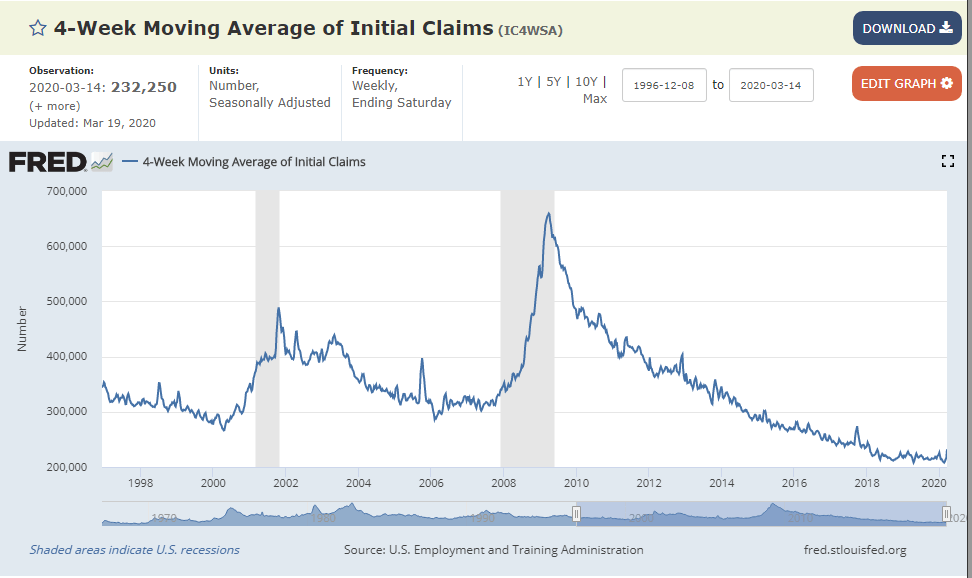

The American economy had a good year, the labor economy had an excellent one. Last year’s statistics and averages are well known: Non-farm payrolls 177,750 per month, annual average hourly earnings 3.3%, unemployment 3.7%, initial jobless claims 218,300 weekly, the last two at five decade lows.

These are somewhat surprising figures for an economy that if the final version of Q4 GDP is as forecast averaged 2.325% across the year and just 2.07% after the first three months.

These good times for workers and the economy continued in January and February with payrolls averaging 273,000, earnings strong and initial claims and unemployment near their records.

Atlanta Fed GDPNow

The GDP forecast from the Atlanta Fed GDPNow model was still estimating a 3.1% annualized first quarter expansion on March 25, albeit with a stark warning in red on the homepage that it does not capture the impact of the Coronavirus beyond what is in the source data.

That GDP rate will drop as more data from the final month of the quarter becomes available but the upshot is that until the viral strike at employment the US economy was headed for another year of its longest expansion on record.

There are eight more updates to the GDPNow figure for the first quarter before the final estimate on April 28, including the February numbers for durable goods, the trade balance and construction spending and March numbers for ISM manufacturing, retail sales, durable goods and industrial production.

The first estimate for the second quarter will be issued on April 30 to be followed by 22 others until the final version on July 29.

Second quarter 2020 GDP

With the first quarter divided at the 10 week mark, when the first statistical impact of the virus began in initial jobless claims, it is going to be difficult to judge the effect of the business closures and layoffs on the US economy until well into April after sufficient March economic numbers are released.

While a substantial number of workers have been furloughed or laid off in March, and anecdotal numbers are extraordinarily high, it is unknown whether the job losses will continue into April and what effect this and the widespread store closures will have on consumer spending.

Even more important will be the perceived length of the economic shutdown and the success of the government’s stimulus measures in preventing a collapse in consumption and a continuing reduction in payrolls.

Conclusion

The normal continuity of economic growth from quarter to quarter has probably received one of its sharpest shocks in US history this month. The last quarter of 2019 and the first two-and-a-half months of this year will provide little guidance for the weeks and months head.

Even the rapid rise in initial jobless claims which began in February 2008 from 339,750 in the four-week moving average to its peak at 656,000 in March 2009 and signaled the real beginning of the financial crisis, had begun when the US economy was already in a recession, according to the Bureau of Economic Analysis.

The US economy was clearly not in recession in the first quarter and if the next half year proves to be an end to the longest expansion in American history it will not be a classic business cycle or financial crisis downturn.

"It's really much closer to a major snowstorm or a natural disaster than it is to a classic 1930s-style depression," said Federal Reserve Chairman Ben Bernanke recently.

"This is a very different animal than the Great Depression. The Great Depression, for one thing, lasted for 12 years, and it came from human problems: monetary and financial shocks that hit the system."

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.