US Durable Goods February Preview: Consumption to reflect labor market recovery

- Durable Goods Orders expected to remain positive at 0.8% after 3.4% in January.

- February Retail Sales fell 3% but January revised to 7.6% from 5.3%.

- Nonfarm Payrolls in February strong at 379,000, for March 500,000 are forecast.

- Markets attending and trading on US economic data.

- Dollar and US interest rates are responding to improving American statistics.

Purchases of long-duration consumer goods are expected to remain positive in February, enabled by the improving labor market, despite the plunge in Retail Sales after the expiration of December stimulus payments.

New Orders for Durable Goods are forecast to have climbed 0.8% last month after January's 3.4% jump. Orders outside of the transportation sector, in practice the civilian aircraft business of Boeing Corporation of Chicago, are predicted to add 0.6% following a 1.3% gain in January. Nondefense Capital Goods orders ex Aircraft, the business investment analog, are projected to rise 0.5% after 0.4% in January.

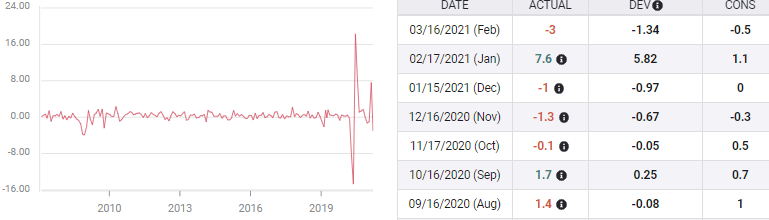

Retail Sales

The December stimulus payment of $600 to individual translated into the largest one month gain in consumption, excepting the rebound from the March and April lockdown, in almost two decades. All three categories of Sales saw large increases that were revised even higher two weeks later.

Overall Retail Sales initially rose 5.3%, that jumped to 7.6%, Sales ex Autos added 5.9% revised to 8.3%, and the Control Group, which closely mimics the consumption component of GDP, rose 6% originally, 8.7% after adjustment.

Retail Sales

The revisions, 2.3% for Sales, 2.4% for ex Autos and 2.7% for Control, erased most of the losses in the three groups in February, respectively, 3%, 2.7% and 3.5%. The February Sales results will themselves be revised by the US Census Bureau at the end of March.

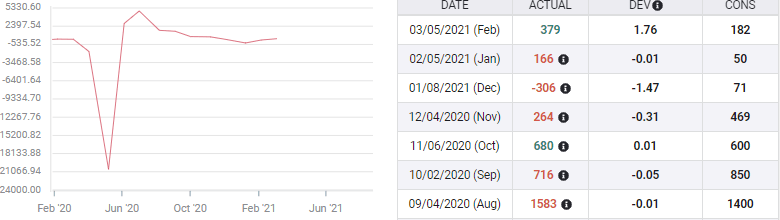

Nonfarm Payrolls

Payrolls shed 306,00 jobs in December as California's second general lockdown pummeled employment in the nation's largest economy. Despite this reversal consumers were not deterred from spending their stimulus checks.

Jobs rebounded smartly in January and February adding 545,000, more than twice as many as the combined 232,00 forecast.

Nonfarm Payrolls

March payrolls are due on Friday April 2 and the consensus estimate of 500,000 would put the economy firmly back on the path to pandemic recovery.

Conclusion

The resilience of the American consumer is one of the bulwarks of the US economy.

With nearly one million people expected to be re-employed in the first quarter and a $1400 stimulus hitting bank accounts this month, more than double the payment in January, two assumptions seem reasonable.

First, the February Retail Sales figures will likely be revised higher as were the January results.

Second, if Sales were stronger in February, then their Durable Goods subset will prove better than expected also.

Americans can read about and more importantly sense, the daily improvement in the economy and the labor market. With more than 2.5 million vaccines delivered daily, private, if not public optimism is right around the corner.

It would be highly uncharacteristic of the US consumer, if that optimism was not immediately fulfilled.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.