US Dollar Weekly Forecast: Powell and NFP take centre stage

- US Dollar Index clinches its fourth weekly drop in a row.

- Investors price in around 75 bps of easing by year-end.

- NFP and Chair Powell grab all the attention next week.

Pessimism surrounding the US Dollar (USD) persisted this week, pushing the US Dollar Index (DXY) to new lows near the psychological 100.00 level on Friday, its weakest point since the summer of 2023.

It was not over for the Greenback’s downtrend after the Federal Reserve's (Fed) unexpected jumbo rate cut on September 18.

Strong speculation of additional rate cuts at the next two Federal Reserve meetings, coupled with ongoing optimism about a soft landing for the US economy, is expected to sustain a positive tone in risk-sensitive markets. This, in turn, is likely to keep the US Dollar under continued pressure for the time being.

So far, the Dollar’s price movement highlights a key resistance area just below the 102.00 level. The broader bearish trend is likely to persist as long as the DXY remains below the critical 200-day Simple Moving Average (SMA) at 103.73.

Bets on a US soft landing remained on the rise

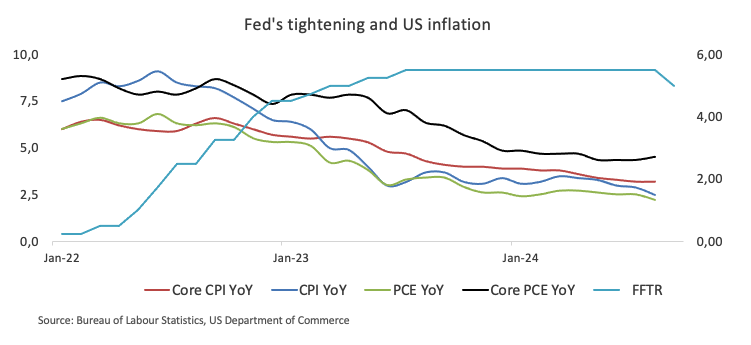

After the unexpected rate cut in September, market participants are now focusing on the performance of the US economy to better assess the likelihood of further rate reductions. Last Wednesday’s event marked the Fed’s first interest rate cut since 2020, with a larger-than-expected 0.5 percentage point decrease in the Fed Funds Target Range (FFTR), now set at 4.75%-5.00%. The Fed described this move as a “recalibration” aimed at sustaining economic momentum.

The Committee’s projections following the meeting indicated that additional rate cuts could occur before the end of the year. Policymakers now expect inflation to decline more quickly and unemployment to rise higher than previously anticipated.

During his press conference, Fed Chair Jerome Powell expressed optimism, stating that he does not foresee a recession or economic downturn in the near future, citing robust growth, falling inflation and a stable labour market. He downplayed the likelihood of a recession.

Investors are still pricing in around 75 basis points of further rate cuts for the remainder of the year. Although recession concerns have diminished, upcoming economic data will be crucial in shaping the Fed's monetary policy in the coming months.

According to the CME Group's FedWatch Tool, there is currently a 52% chance of a half-point rate cut at the Fed's November 7 meeting, with a 25-basis-point reduction favoured for December.

Not all Fed officials seem to lean towards further easing

Markets listened to the first voices in the wake of the Fed’s 50 bps rate cut.

That said, Atlanta Fed President Raphael Bostic, a noted hawk, and Chicago Fed President Austan Goolsbee, a dove, have both expressed support for the recent interest rate cut, citing progress on inflation and rising unemployment.

In contrast, Fed Governor Adriana Kugler argued that while the fight against inflation is ongoing, it is not yet a victory.

Fed Governor Michelle Bowman emphasized the need for caution as key inflation measures remain above the 2% core target, suggesting it may be time for the Fed to adjust its monetary policy. She dissented from last week's half-point rate reduction, advocating for a more "measured" quarter-point cut due to potential risks to inflation, such as disruptions in global supply chains, aggressive fiscal policies, and a mismatch between housing supply and demand.

Interest rates on the rise or fall? A global view

The Eurozone, Japan, Switzerland, and the United Kingdom are facing growing deflationary pressure, with economic activity taking an erratic path.

In response, the European Central Bank (ECB) executed its second interest rate cut earlier this month and maintained a cautious stance on further actions for October. While ECB policymakers have not confirmed additional cuts, markets are anticipating two more reductions by the end of the year.

Similarly, the Swiss National Bank (SNB) reduced its rates by another 25 basis points this week. The Bank of England (BoE) held its policy rate steady at 5.00% last week, citing persistent inflation and elevated prices in the services sector, combined with strong consumer spending and stable GDP data.

Meanwhile, the Reserve Bank of Australia (RBA) opted to keep rates unchanged at its latest meeting on September 24, while signaling a continued hawkish narrative in its subsequent remarks. Analysts see the possibility of easing starting early in 2025. The Bank of Japan (BoJ) maintained a dovish hold at its September 20 meeting, with money markets predicting only 25 basis points of tightening over the next 12 months.

The intersection of politics and economics

Despite Vice President Kamala Harris, the Democratic Party's presidential candidate, being viewed as the winner of the recent debate against Republican contender and former President Donald Trump, recent polls still show a tight race as the November 5 election approaches.

If Trump wins the election, his administration could reinstate tariffs, potentially disrupting or reversing the current disinflationary trend in the US economy and shortening the window for Fed rate cuts.

On the other hand, some analysts suggest that a Harris administration might implement higher taxes and possibly pressure the Fed to ease monetary policy, especially if signs of slowing economic growth emerge.

What’s up next week?

Next week promises to be eventful on the US economic calendar. With the Fed shifting its focus from inflation to the labour market, the upcoming Nonfarm Payrolls (NFP) report is set to take centre stage toward the end of the week.

Also drawing attention will be the ADP report, which measures job growth in the US private sector, alongside the JOLTs Job Openings and ISM reports for both the manufacturing and services sectors.

Techs on the US Dollar Index

Since the US Dollar Index (DXY) dropped below the key 200-day Simple Moving Average (SMA) at 103.73, it has managed gains in only one of the past seven weeks.

The DXY is now facing considerable downward pressure, with a strong support level at its year-to-date (YTD) low of 100.15 (set on September 27). Further bouts of selling pressure could trigger a move to the psychological 100.00 mark, with a potential retest of the 2023 low at 99.57 (recorded on July 14) emerging on a breach of that level.

On the upside, the index could experience a short-term recovery. Initial resistance would likely come at the September high of 101.91 (set on September 3), followed by the 55-day SMA at 102.28 and the weekly peak of 103.54 (reached on August 8). The 200-day SMA would act as a critical barrier if the latter is surpassed.

Additionally, the Relative Strength Index (RSI) on the daily chart has confirmed the recent lows, hovering around 40. This suggests there is still room for further losses before reaching the oversold threshold at 30. Meanwhile, the Average Directional Index (ADX) remains close to 41, signalling that the ongoing downtrend is moderately strong but not yet at extreme levels.

Economic Indicator

Nonfarm Payrolls

The Nonfarm Payrolls release presents the number of new jobs created in the US during the previous month in all non-agricultural businesses; it is released by the US Bureau of Labor Statistics (BLS). The monthly changes in payrolls can be extremely volatile. The number is also subject to strong reviews, which can also trigger volatility in the Forex board. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish, although previous months' reviews and the Unemployment Rate are as relevant as the headline figure. The market's reaction, therefore, depends on how the market assesses all the data contained in the BLS report as a whole.

Read more.Next release: Fri Oct 04, 2024 12:30

Frequency: Monthly

Consensus: 145K

Previous: 142K

Source: US Bureau of Labor Statistics

America’s monthly jobs report is considered the most important economic indicator for forex traders. Released on the first Friday following the reported month, the change in the number of positions is closely correlated with the overall performance of the economy and is monitored by policymakers. Full employment is one of the Federal Reserve’s mandates and it considers developments in the labor market when setting its policies, thus impacting currencies. Despite several leading indicators shaping estimates, Nonfarm Payrolls tend to surprise markets and trigger substantial volatility. Actual figures beating the consensus tend to be USD bullish.

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Canadian Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.22% | 0.22% | -1.55% | 0.36% | -0.25% | -0.26% | -0.46% | |

| EUR | -0.22% | 0.00% | -1.80% | 0.10% | -0.46% | -0.50% | -0.66% | |

| GBP | -0.22% | 0.00% | -1.76% | 0.12% | -0.44% | -0.47% | -0.65% | |

| JPY | 1.55% | 1.80% | 1.76% | 1.92% | 1.34% | 1.31% | 1.15% | |

| CAD | -0.36% | -0.10% | -0.12% | -1.92% | -0.61% | -0.60% | -0.80% | |

| AUD | 0.25% | 0.46% | 0.44% | -1.34% | 0.61% | -0.01% | -0.21% | |

| NZD | 0.26% | 0.50% | 0.47% | -1.31% | 0.60% | 0.01% | -0.19% | |

| CHF | 0.46% | 0.66% | 0.65% | -1.15% | 0.80% | 0.21% | 0.19% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.