US CPI November Preview: A long time ago in an economy far far away

- Core annual rate forecast to rise 1.8%, overall to fall to 1.1%.

- Strong retail sales recovery from May has not restored pricing power.

- Federal Reserve inflation averaging and rate hold eliminates CPI policy input.

- Inflation statistics are no longer market moving events.

For more than a generation inflation was at the center of Federal Reserve interest rate policy. From the appointment of Paul Volcker as Chairman in 1979 with core inflation at 10% and rising to Ben Bernanke's first term before the financial crisis and recession collapsed consumer prices, the taming of inflation was the great success of US central bank policy.

It is easy to forget that one of the chief concerns over the Fed's quantitative easing programs was that the liquidity addition to the US financial system and economy would create inflation.

Milton Friedman's famous 1963 formulation that “Inflation is always and everywhere a monetary phenomenon,” did not survive its clash with the with the destruction of retail pricing power from a globalized supply chain

The Federal Reserve's adoption of inflation averaging this year was a recognition that employment and the labor market have replaced consumer prices as the main interests of policy. Inflation averaging permits the FOMC to keep interest rates as low as necessary for a long as necessary to promote economic expansion, even if prices begin to increase.

Briefly, that is why the Consumer Price Index (CPI) and its Fed favorite sibling the Personal Consumption Expenditure Price Index (PCE) have become second-tier economic statistics, informative but no longer able to move markets.

That said, CPI is forecast to rise 0.2% in November after October's flat result and to fade to 1.1% on the year following 1.2% prior. Core CPI, excluding food and energy prices, is projected to gain 0.1% after flat and to rise to 1.8% from 1.6% in October.

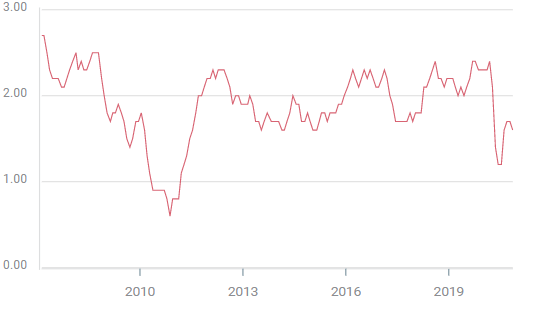

Core CPI

Retail Sales: Collapse and pricing

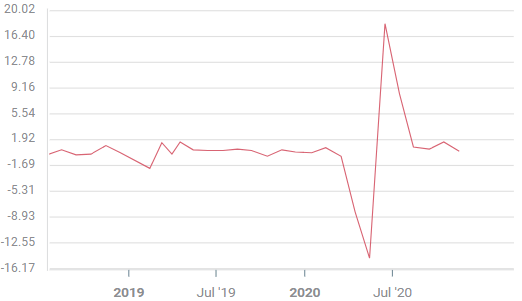

The March and April lockdown collapse of Retail Sales and its GDP component Retail Sales Control Group has been followed by a surprisingly strong six months. For the entire eight months Retail Sales have averaged 0.89% and the Control Group 1.06%. In comparison the 2019 monthly averages were 0.51% for Sales and 0.46% for Control.

Retail Sales

Consumer prices have recovered from the outright declines of March, April and May which averaged -0.43% for CPI and -0.20% for core. The annual rate dropped to 0.3% in April and 0.1% in May and has bounced to 1.2% in October and the predicted 1.1% in November. Core annual prices fell to 1.2% in May and June and were 1.6% in October and the projected 1.8% in November.

These rates are well below their immediate pre-pandemic scores of 2.5% in January for CPI and 2.3% for Core CPI. The swift and sustained revival in consumer spending has not returned inflation to the levels that it took almost a decade after the 2008 financial crisis to produce.

Conclusion and markets

Inflation and consumer prices are the step-children of Federal Reserve policy. While the governors would welcome price changes at or above at their 2% target, not only as the achievement of a policy goal but also as an indication that the economy and the labor market had recovered from the lockdown catastrophe, they will take no measures to hurry the process.

The recent dollar weakness will not be ended by Fed interest rate fiat.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.