US CPI July Preview: Inflation loses its cachet

- Core CPI predicted to rise 0.2% on the month unchanged from June.

- Annual core CPI expected to slip to 1.1% from 1.2% in June.

- Inflation quiet despite Federal Reserve emergency liquidity.

- CPI and PCE have not been a major policy or market concern since the financial crisis.

Consumer prices are forecast to stabilize in July following the pandemic collapse in March and April and the partial recovery in the three months since.

The core CPI rate plunged from 2.4% in February to 2.1% in March, 1.4% in April and 1.2% in May and June. It is forecast to dip to 1.1% in July which would be the lowest for this price measure since February 2011. The monthly core rate is expected to be unchanged at 0.2% after three months of deflation at -0.1% in March, -0.4% in March and -0.1% in May.

The headline inflation rate is projected to rise 0.3% in July after June’s 0.6% gain. The closure of most of the US economy forced all CPI prices into deflation at -0.4% in March, -0.8% in April and -0.1 May. The yearly rate should rise to 0.8% from 0.6% in June. This measure of prices fell from 2.5% in January to 1.5% in March, 0.3% in April and 0.1% in May for the lowest reading since -0.1% in March 2015.

Fed, QE, CPI and PCE

The Fed’s 2% core PCE target, official since the Bernanke years, has been a theoretical goal. Inflation has not been symmetric around the target and except for a few months in 2012 and again in 2018 with nine of 12 months that year at or above 2%, the core PCE target has been a rhetorical exercise.

The gains in 2018 may have been aided by the Fed’s three quantitative easing programs over the prior decade that had added trillions in liquidity to the economy but the main energy for returning prices was the buoyant economy and rising wages.

Core PCE prices averaged 1.983% in 2018, but that increase in inflation, years and trillions of dollars in the making, did not last. Inflation fell throughout 2019 ending at a 1.692% average for the year.

The precipitous fall in core PCE inflation this year from 1.7% in March to 0.9% In April, 1% in May and 0.9% in June is due to the pandemic collapse in demand.

Since the onset of the Covid pandemic the Fed and the Federal government have flooded the US economy with more than $6 trillion in financial, economic and payroll support. Mortgage rates are at their lowest in history courtesy of the Fed’s bond purchases. Chairman Powell has said the central bank will continue its programs unit the economy is fully recovered.

Monetarist inflation, globalization and demand shocks

Prices have stopped falling. The outright CPI deflation of March, April and May has reversed.

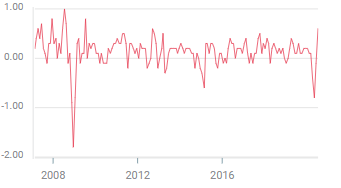

CPI, M/M

But QE has proven that the monetarist equation that ‘prices are always and everywhere a monetary phenomenon’ has two caveats that were not evident when it was formulated.

The first is the globalization of production. Price competition in goods is no longer set in an individual economy but in toto around the world. The ability of US manufacturers to raise prices is not determined in Ohio and Michigan but in Shanghai, Vientiane, Turkey and a dozen other places. Global manufacturing is a powerful restraint on inflation.

The second is demand. If consumers aren’t buying the amount of money in the system is irrelevant. The collapse of demand after the financial crisis and again in March and April under the lockdowns showed just how vulnerable factories, retailers and prices are to customer abstinence

Conclusion and markets

Inflation will not return to its pre-pandemic range until consumer spending stabilizes.

Crashing and rebounding sales cannot provide the security for business planning that is a necessary condition for hiring.

The Fed’s focus before the pandemic was maintaining the then excellent labor market. Its goal now is to do all it can to revive that employment picture. In the economic order jobs come first, then consumer demand and last, inflation. Without a tight job market and rising consumption, there can be no upward pressure on prices.

Inflation is a distant third in central bank proprieties. Flooding the economy with cash and credit will not raise prices unless people are working and spending. Markets know this and that no CPI or PCE result will change Fed policy.

When that link is if broken, inflation is no longer a relevant statistic for trading.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.