US CPI inflation cooled to +2.5% in August

According to a report released by the Bureau of Labor Statistics (BLS) earlier today, headline US CPI inflation (Consumer Price Index) eased to +2.5% in August (YoY), testing levels not seen since February 2021. The latest inflation data sent US Treasury yields and the US Dollar Index northbound, with major US equity index futures trading on the back foot.

This is the last tier-1 release before the US Federal Reserve (Fed) makes the airwaves next week, with a 25 basis point reduction firmly on the table.

Inflationary pressures pulled back from July’s reading of +2.9% and was marginally south of the economists’ median estimate of +2.6% (as per a poll by Reuters). On a MoM basis, headline CPI inflation rose +0.2% in August, matching both market expectations and prior data.

According to the BLS, the index for shelter rose +0.5% in August, its highest level since the beginning of the year, and was the most significant contributor to headline inflation. Excluding energy, services rose +0.4% in August from +0.3% in July. Airfares also increased in August, rising a beefy +3.9% after five consecutive declining months. On the other hand, energy prices fell -0.8% (after July came in unchanged), helping to bring down overall inflation.

Core inflation remains firm

Underlying inflation, or ‘core’ inflation, which excludes volatile food and energy components, rose +3.2% in August, as expected, and unchanged from July’s release. However, core CPI was slightly higher than expected between July and August, increasing +0.3% from +0.2% (+0.2% consensus). Interestingly, according to Bloomberg, five out of 65 economists’ estimates called for a +0.3% rise in monthly core CPI; the majority were at the median +0.2%. The monthly measure also marks the largest rise in four months, with most of this upside from shelter costs. This will likely help nudge the Fed towards a 25 basis point cut.

Fed gearing up for a rate cut

The latest data comes as the Fed prepares to turn a corner next week and reduce the Fed funds target rate, which has stood at a 23-year high at 5.25%-5.50% since late 2023.

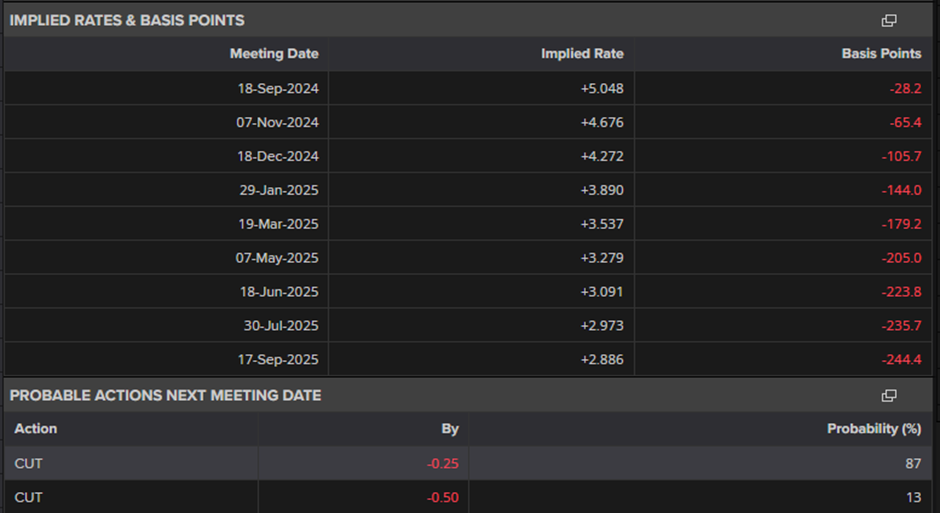

While it is clear to most analysts that the central bank will reduce policy at next week’s meeting, recent data has seen investors pare back rate bets. Markets are still fully pricing in a 25 basis point rate reduction and have significantly priced out the possibility that the Fed will opt for a bulkier 50 basis point cut.

Simply put, markets are pricing in an 87% probability of a 25 basis point reduction next week over a 13% chance of a 50 basis point cut.

US Fed Chair Jerome Powell and his colleagues have made it clear that confidence has grown regarding inflation heading towards the central bank’s 2.0% target. Consequently, the focus has shifted to the other side of their dual mandate: the labour market.

Last week’s US Employment Situation Report for August revealed that a little over 140,000 jobs were added to the US economy in August, up from 114,000 the month prior. Albeit displaying growth, the report did come in lower than expected (160,000). Average hourly earnings continued to rise on a MoM and YoY basis for August, while the unemployment rate dipped to +4.2% in August from +4.3% in July.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,