US Consumer Inflation in 2022: The uninvited guest takes up residence

- US consumer prices race to 40-year highs in 2021.

- Inflation forces a reversal of Federal Reserve policy.

- COVID-19, lockdowns, supply and labor shortages and government liquidity are culprits.

- Inflation prospects for 2022 depend on the economic changes from the pandemic.

- US dollar will benefit from the Fed's inflation conversion.

Inflation hit the American economy like a bolt from the blue in 2021. In January consumer prices were trundling along at 1.4% a year. The Federal Reserve’s warning the prior September in conjunction with its move to inflation-averaging, that prices might get a bit effusive in the second half as the base effect from the lockdowns played out, turned out to be accurate but wholly inadequate.

The combination of pandemic induced labor and supply shortages, reviving consumer demand and massive monetary stimulus from Washington and the Federal Reserve, fueled a quadrupling of the Consumer Price Index (CPI) in just ten months.

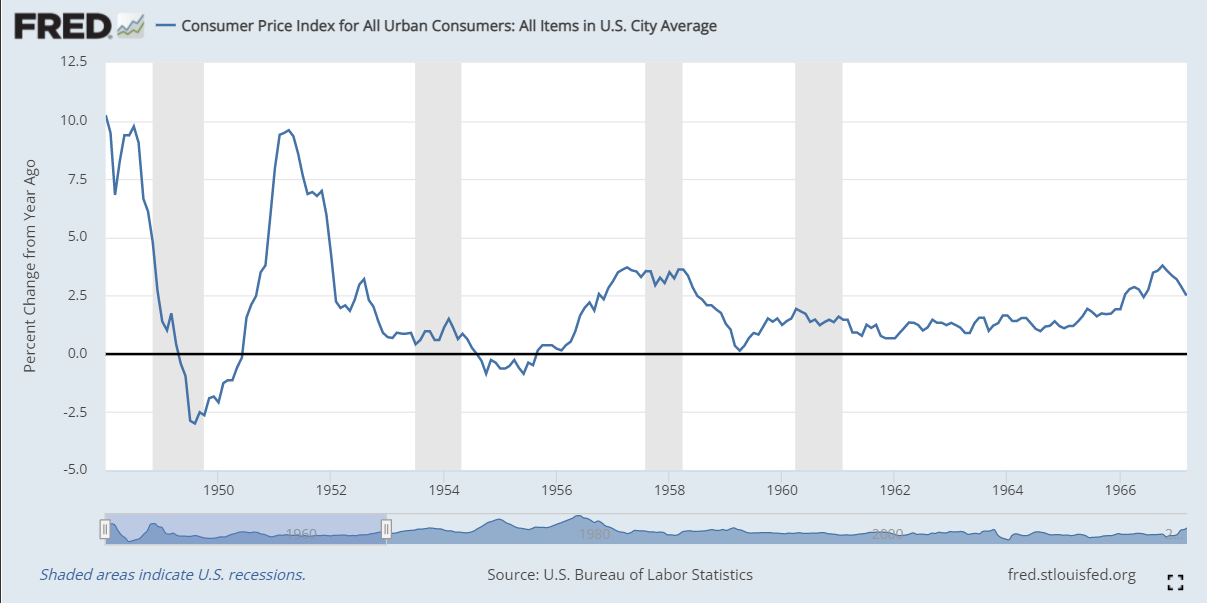

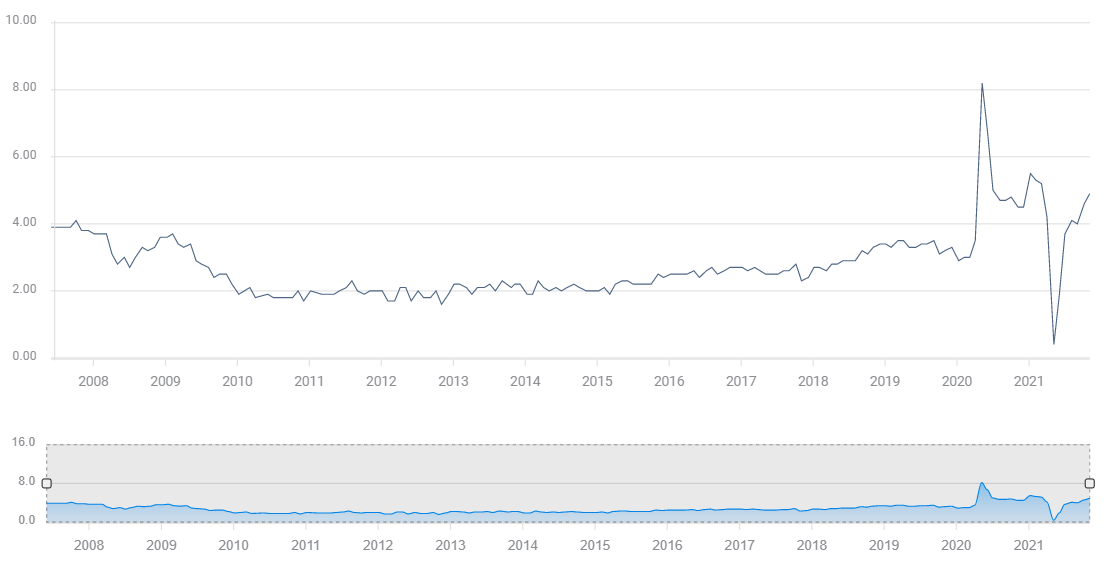

CPI

Though the particulars of this year’s price surge were different than the two previous bouts of inflation, the steep and relatively brief surge in 1950 and 1951 and the prolonged bout in the 1970s, the logic is the same – more money chasing fewer goods.

In 1948 the aftermath of the withdrawal of the enormous war-time spending and the return of millions of soldiers to the labor force fronted an 11-month recession and a collapse in consumer prices that reversed just as violently as it had begun.

The Consumer Price Index (CPI, YoY) plunged to -3% in August 1949, peaked at 9.6% in April 1951 and by May 1952 was back at 1.8%. In total CPI spent 20 months, from August 1950 to March 1952 above 2%.

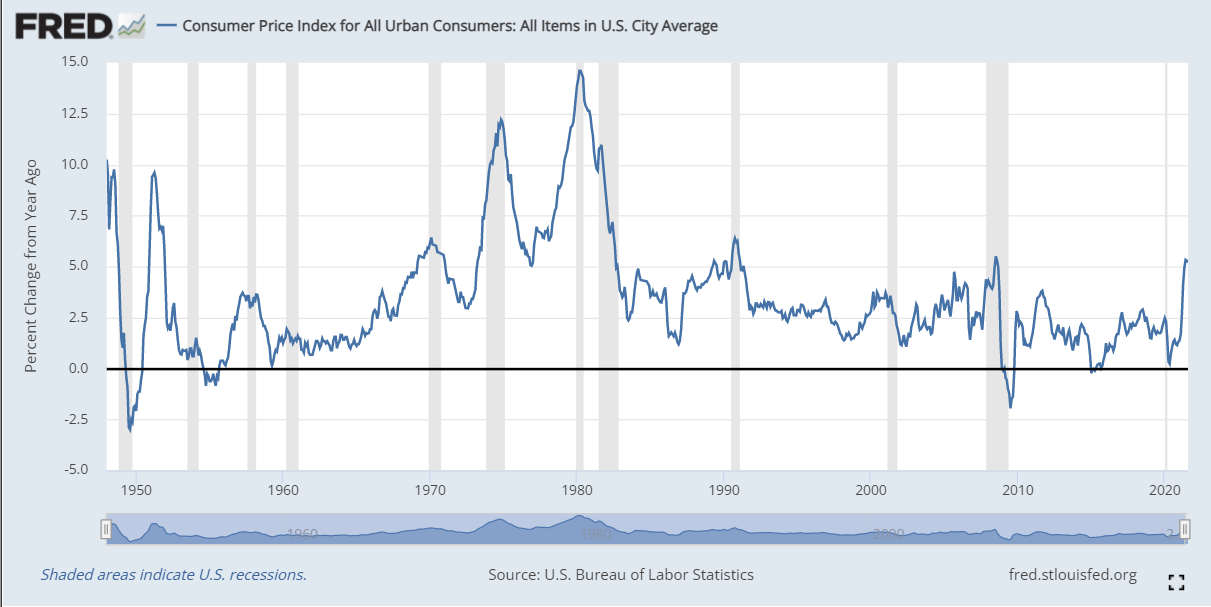

The origin of the inflation in the 1960s and 1970s lay in Washington’s unwillingness to fund the Vietnam War and the extensive expansion of social programs without commensurate tax increases. Consumer prices crossed the 2% line in February 1966 and did not return to that level until April 1986, more than two decades later. In April 1980 CPI reached 14.6%, still the US record.

Paul Volker was appointed to head the Federal Reserve by President Jimmy Carter in August 1979. His implementation of monetarist theory, and the ensuing regime of high interest rates which reached 20% in 1980, eventually squeezed inflation out of the US economy. Despite the two recessions precipitated by the Fed’s rate policies, President Ronald Reagan, who replaced Carter in 1980, backed Volker throughout and the US economy turned in its best post-war performance in his second term.

Central banks around the world imitated the success of the Fed in adopting strict inflation targets. When these rate policies were combined with the globalization of manufacturing that lowered prices and widened the competitive labor market beyond national borders, restraining wages, inflation commenced a long decline that saw it below 2% for most of the decade to 2020.

The question for analysts, government officials, business managers and consumers is which example of inflationary excess is the US economy likely to follow in 2022 and beyond.

Before we venture an opinion let’s look at the origins of inflation as standardized by economic analysis.

Inflation mechanics

Economists generally describe two paths of inflation causality: Cost-push inflation and demand-pull inflation.

Cost-push inflation occurs when retail prices rise due to increases in wages, raw materials and other manufacturing and production inputs. Companies raise consumer prices to cover their own increased costs.

The lockdowns and subsequent reluctance of workers to return to employment have forced employers to raise wages. The shortage of workers has curtailed the mining and production of raw material and components. Higher wages and shortage pricing have been incorporated into producer expenses and retail prices.

Another good example is the year-long surge in oil prices which began their climb in November 2020 in response to the US presidential election of Joseph Biden. Oil is the industrialized world’s basic commodity. In one form or another, as feedstock or energy, oil is part of the production of almost every consumer good. The 98% rise in West Texas Intermediate (WTI) in the last year has affected every aspect of manufacturing and is a direct contributor to CPI in energy prices.

Demand-pull inflation happens when the demand for a good or many goods outstrips the supply. It can occur when demand rises on a static supply or when supply falls. The reduction in production for many consumer goods due to labor and material shortages over the past year has made items scarce and more dear. At the same time, overall demand has risen as people first made up deferred consumption and second, with waning restrictions in many places, resumed normal purchasing. In the past decades the cheaper goods available from alternative usually overseas sources largely deprived retailers of pricing power. They could not increase their prices without risking a loss of market share. In the current global scarcity, that restraint has vanished.

Two other factors often abet the inflationary impulse in consumer prices: fiscal largess and monetary stimulus.

Governments at the federal and state level respond to economic hardship by sending money directly to the consumer. Whether extended unemployment benefits, direct subsidies for the pandemic, food stamps or the many other government programs, the purpose is to maintain consumption by giving consumers money.

Fiscal stimulus from the Federal Reserve is also a common response to economic problems. The current incarnation is near zero interest rates for almost two years and a massive bond-buying program. These efforts operate at the market level, propping up equity, bond and housing prices. They do not directly affect consumer inflation as stock and home prices are not considered in consumer indexes, though by providing a sense of wealth they contribute to a willingness to spend.

Current inflation

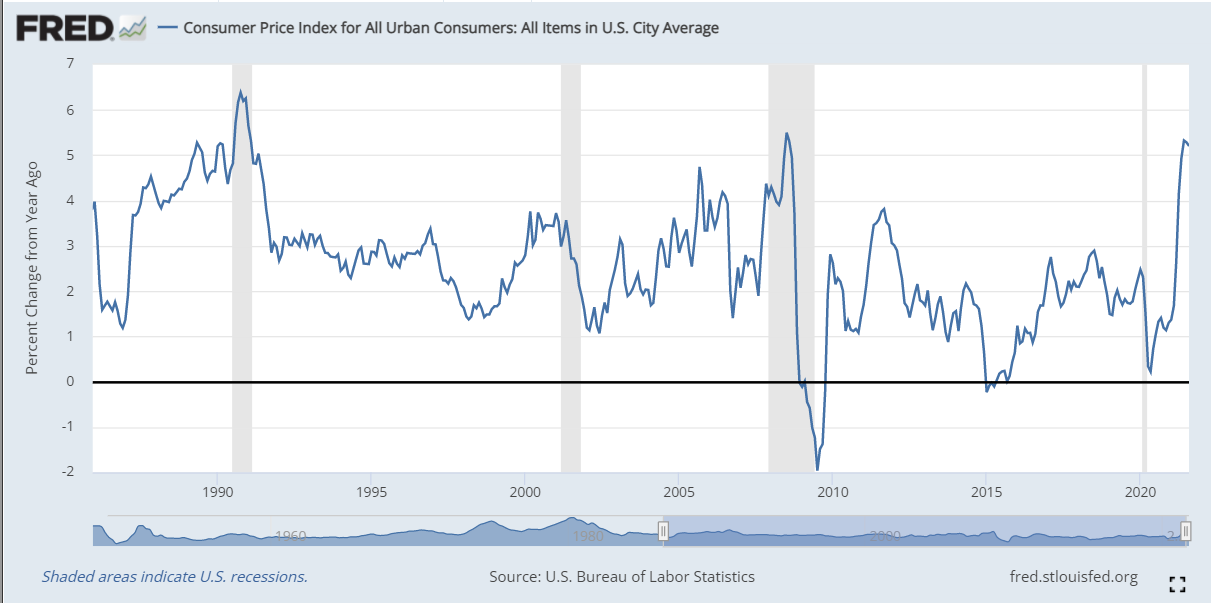

The speed and extent of this year's inflation is something the US has not seen in a generation.

The Consumer Price Index (YoY) was 6.2% in October and the six-month average was 5.5%. That is the highest monthly rate since 6.4% in October 1990. It is the fastest half-year of price gains since the six month beginning that October.

In the 12 months from November 2020 to October 2021, CPI rose 5%, from 1.2% to 6.2%. That is the quickest annual acceleration in inflation in 71 years. Even the great surges in CPI from 1973 to 1975 and 1978 to 1980 had 12-month increases of 4.1% and 4.7% respectively.

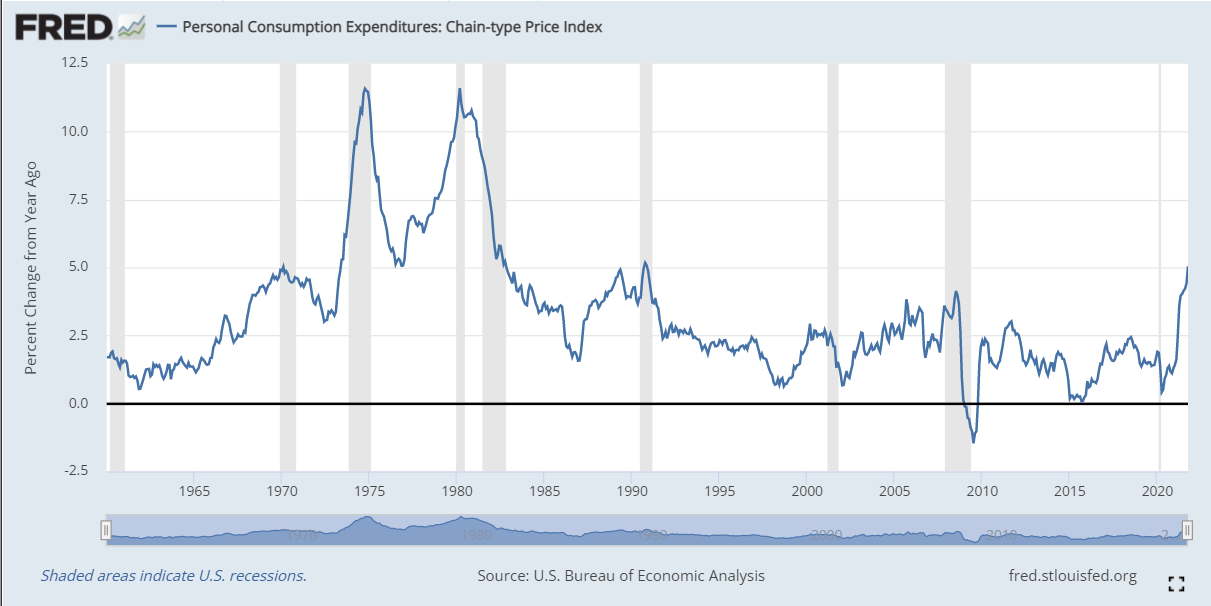

The Personal Consumption Expenditure Price Index (PCE for short), designed as it is to produce lower inflation numbers, has lagged CPI but at 5% in October is the highest rate in exactly the same 31 years since October 1990.

Producer Prices, harbingers of future consumer inflation, are also setting records. October ‘s Producer Price Index (PPI, YoY) was 8.6%, up an astonishing 7.8% since November 2020 and the highest rate in 13 years.

Headline vs core inflation

The Federal Reserve uses the Core PCE rate in its measurement of US inflation, believing that it is a better representation of long-term price trends.

Our concern is about the impact of inflation on consumer behavior and the US economy. For that, headline prices are more accurate for the simple reason they represent what consumers see and pay when they make their purchases.

Current inflation causes

Inflation’s sudden and virulent emergence this year was a product of price pressure from both sides of the supply and demand equation.

From the producer's cost side, the lockdowns and subsequent restrictions put many materials and components in short supply and raised prices dramatically. These increases took place against a background of soaring energy prices, a trend that predated the lockdowns, and whose origin had nothing to do with the pandemic. These price increases were passed on to retailers and consumers.

Supply-chain problems, initially a matter of business closures, are now primarily one of workers shortages. Businesses cannot find the workers to fill their orders. Producers ran down what stockpiles they possessed. Many components, particularly the ubiquitous computer chips, remain in short supply keeping prices high and rising.

The vulnerability of just-in-time production schedules to interrupted deliveries was an unpleasant surprise to businesses that have operated on that model for a generation.

In order to secure employees, businesses have been forced to offer higher wages and signing bonuses. As payroll expenses are normally a business’s largest line item, the additional cost to consumers is large.

Annual Average Hourly Earnings (AHE) have averaged 4.3% for the six months to November about double the increase for the decade from 2010 to 2020.

AHE

FXStreet

On the demand side consumption has remained surprisingly strong though most of the pandemic. First, after the lockdowns last year as deferred purchasing was resumed all at once, and lately as the restrictions have ended in most of the country and normal life returned.

From August to November this year, Retail Sales climbed 0.58% each month. In 2019 the average gain for the entire year was 0.45%.

Retail Sales

Personal Spending has increased 0.70% a month from August through November. In 2019, the last full year before the pandemic, this consumption measure averaged 0.36% monthly.

As the unconstrained consumer has come up against the limited availability of goods, price increases have blossomed everywhere.

For the first time since globalization became the order of the day, retailers and manufacturers have regained pricing power. In the past if a retailer or wholesaler wanted to raise prices, chances were that there was another outlet, often with an overseas source who was willing to undercut prices and gain sales. The name of the game was market share.

Now the product scarcity is worldwide. There is no alternative source for cars or computers or whatever is hard to find and companies can sell at their asking prices.

Fiscal and monetary stimulus

Washington has poured more than $4 trillion into the economy, mostly in the form of grants directly to businesses and consumers. Unemployment insurance, pandemic stipends, food-stamps and a dozen other programs have kept cash flowing to families and individuals and this largess has helped to keep consumer spending strong.

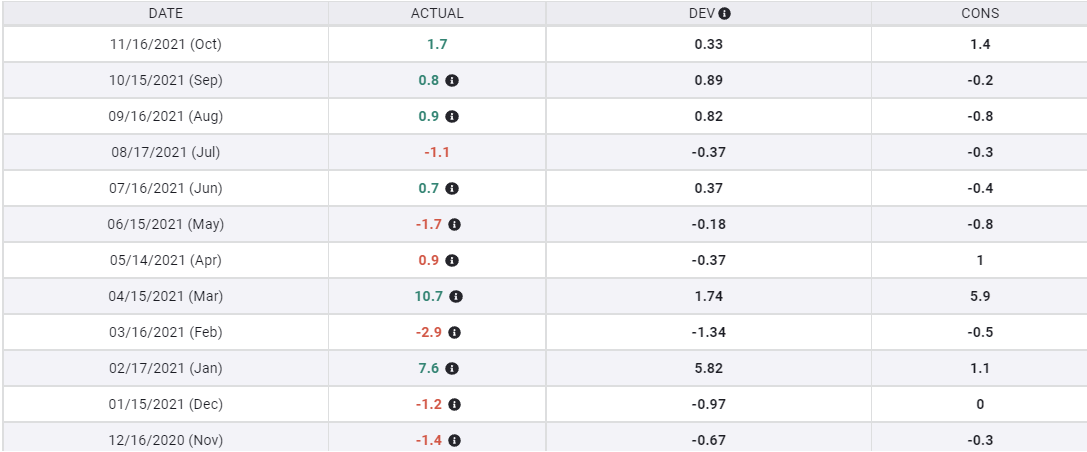

Retail Sales rose 7.6% in January and 10.7% in March, by far the largest gains this year. These were the months when the payments from government rescue bills reached consumers.

The Federal Reserve has kept the fed funds rate at a record low of 0.25% for nearly two years. Its $120 billion a month of Treasury and mortgage-backed securities purchases have served to keep commercial rates near all-time lows since March of last year, offering business cheap and nearly inexhaustible funding.

The Fed’s efforts have limited impact on consumers but are a large factor in asset markets and may have a minor wealth effect on consumption. Asset prices are not included in CPI or PCE measures and so their very evident inflation is not an official concern.

Fiscal stimulus has been the greatest government factor in inflation. By giving consumers recurrent grants, demand has boosted in an economy suffering from widespread supply restrictions.

Inflation in 2022: Supply and demand

The pandemic and the lockdowns that were instituted around the world in response have undone much of the old global order. The replacement is not yet at hand.

Supply chains will gradually unkink and the shortages, particularly of computer chips, that have inhibited automobile production and much else, will ease. Ports will gradually return to normal operation and the logistical delays that have inhibited production will end.

Supply will improve but the pandemic saw the high point of the globalized production and distribution chains. The problems exposed by the pandemic will incur permanent changes.

Nations and manufacturers are now acutely aware of the dangers of sourcing many products exclusively overseas. The vulnerability of foreign factories for key medical, defense and even consumer products to the dictates of governments for whom the international aspects of their decisions are far less important than the national ones, is now painfully evident.

The pandemic was global with most governments responding in a similar if not copycat fashion. When China shut factories and plants so did Europe and the United States in short order. Last year's lockdown was worldwide..

It would not, however, be hard to imagine a more local crisis, say for the US and China over Taiwan. Would Beijing attempt to use its dominance of, for example, rare earth metals, as a lever against American and Taiwanese political interests? The danger of outsourcing whole crucial industries to competitors cannot be ignored.

The coming redistribution of new plants away from political competitors and in some cases the repatriation of older institutions to the home country will keep supplies tight and costs higher for years.

The assumption of the past thirty years that globalization is an unmitigated good has been overthrown. It will take years for a new equilibrium to take shape. The costs associated with the new manufacturing world will necessarily be higher than the old

A similar effect has been wrought on the labor market.

Workers, to the puzzlement of many analysts, not the least at the Fed, have shown no rush to return to their old jobs. The labor shortage, like the supply crunch, is worldwide.

As we observed a year ago, (The Homeworking Revolution: Change accelerates for businesses, real estate and stock market ), the pandemic has instituted changes, and fortified trends in employment and home work that were already taking place.

The old world is not returning. There is no greater evidence of that than the more than 10 million jobs on offer in the US for more than six months. Workers are not going back because it's not necessary. The electronic world has created many other opportunities for professional and home life, and workers are flocking to the new paradigms.

This does not mean that the old jobs will disappear. Some will be automated but the others, the welders, factory workers, machinists, and dozens of other skilled trades and physically demanding jobs will require higher pay. The pandemic has fostered an immense dislocation in the US labor market. It will take time and money to sort it out.

Inflation in 2022: Government spending

The US economy is, according to the Atlanta Fed, growing at an 8.6% annualized pace in the fourth quarter. Even if the economists are off by a factor of half, the US economy does not need trillions of dollars of deficit spending to recover from the pandemic.

The $2 trillion infrastructure bill recently passed by Congress may help repair the nation’s bridges and tunnels, or whatever portion is actually headed to its stated purpose, but the resulting spending, which will inject real competitive dollars into an economy already suffering from scarcity induced price increases, must make inflation worse.

The inflation criticism applies even more so to the several trillions of additional spending being contemplated by Congress, which seems oblivious to the real inflation danger.

Inflation in 2022: Federal Reserve policy

Advancing the end of the Fed’s bond program from June to perhaps March, with two fed funds 0.25% hikes in the second half of the year will do little to restrain inflation. That particular genie is out of the bottle. Rates projections for 2023 and beyond are interesting but of little real consequence.

Treasury rates have been unusually restrained despite the Fed’s clear intention to return to the inflation fight. That will change as the Fed’s seriousness becomes evident but interest rates start toward normalization from such a low level that any inflation impact is a year or more away.

Inflation in 2022: Markets

Equities will not be deterred by inflation or by rising interest rates as long as the US and global economies continue to grow strongly. Treasury yields and the credit markets in general will follow the Fed once its policy is proven by action and not just commentary.

The dollar’s direction is determined by the forward rate policy of the Fed and the US economy's resurgent growth, both point to a stronger greenback in 2022.

Inflation in 2022 and beyond

The Fed’s initial inflation predictions of a quickly terminating base effect assumed that the economic world would quickly resume its original shape once the pandemic ended.

Instead the pandemic has reshaped the world in unpredicted ways.

The changes in the global supply chain, in manufacturing and distribution, have only begun and the revisions and relocations will take time and money. The price pressures that began with shortages will continue and abate only slowly as the system reforms. Labor markets are evolving away from their industrial and office models and that change will add to employee costs.

Even if Washington passes no additional pandemic spending bills, there is more than enough money in the hopper waiting to be distributed to insure that too many dollars will be chasing too few goods for the next several quarters.

At the beginning we asked if the brief 1950 or the prolonged 1970s inflation was the better example for this year and next. Early indications are that the global economy is in the opening stages of a profound shift in the manufacturing sector and that the labor market is rapidly adopting an internet distributed model. These adaptations will take years to complete and will prolong the current product, material, component and labor shortages. Inflation will follow the rule of scarcity in goods and labor exacerbated by the endemic responses of governments and central banks, whose single policy is to throw money at every crisis.

The rise of globalized manufacturing and labor markets over the past generation that have been the chief conqueror of inflation are giving way to a far more nationalized enterprise. The higher costs of converting to and maintaining this structure will be with us for several years. Inflation for the rest of the decade is likely to resemble, in its persistence if not its excess, the structural changes of the 1970s rather than the brief recession induced example of 1950.

.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.