The dollar can rally like crazy

Outlook:

We are really surprised that the Fed has capitulated to market fear, whether in the form of inverting yield curves or the stock market rout, saying these market events are a risk to the economic fundamentals. In other words, if enough people believe a recession is coming because yield curves are inverting, it's the Fed's job to de-invert them and fend off a self-fulfilling recession. We never heard of such a thing. See the chart from CNBC. Yeah, we know, but it's the prettiest chart out there.

That doesn't mean it's the wrong statement. Plenty of analysts think it was the right thing to do, including loudmouth Jim Cramer, who says it may put the Trump rally back on track (in person, Cramer is a doll). El-Erian (above) seems to approve, too. Other analyst say we are counting the days to the first cut, not the next hike.

A firm principle of technical analysis is that if enough traders jump on a bandwagon, the bandwagon will keep rolling, even if there is a brick wall around the next corner and the traders know it. In this case, the brick wall would be inflation, and we are all pretty sure by now that it's not around the next corner. In a very real way, a postponement of hikes, aka normalization, is beneficial to those still stuck in QE, mainly the ECB and BoJ. It slows down the divergence process. This is something the ECB can really use, since it faces different problems than the Fed in terms of ending purchases of some risky assets, particularly Italy's but not excluding other of the PIGs. (When France gets added to the PIG list, how will we incorporate the F?)

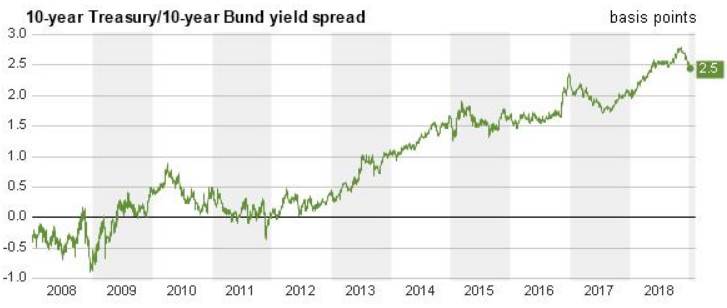

In other words, Powell was inaccurate in naming China as the reason for caution in 2016. It was the yield spread between the US and Europe and Japan. We still have it, and it's still a hugely disruptive factor in international finance. In fact, it's bigger than it was in 2016. See the chart (Thompson Reuters). You have to wonder if the Fed chiefs are in cahoots. At the Atlanta Fed shindig on Friday, former Fed Chairman Bernanke said (WSJ) "the current volatility wasn't unusual. More surprising, he said, was ‘how benign markets were for such a long time despite the risks of trade wars and other things that were going on.'" So there's a second mention of China. This could well be a deliberate misdirection away from our pal and ally, Mr. Drahgi.

If the analysis is correct, we are in for a period lasting at least two quarters of the Fed sitting on its hands. By July, we will either have a hike (JP Morgan's forecast) or a cut. What does this mean for the dollar? Maybe very little, with the China trade war taking center stage until end-March and then whatever Trump serves up next. Uncertainty and risk aversion can still favor the dollar even if one risk-event is removed from the table. The euro's action just this morning is decidedly perverse. German manufacturing orders fell hard from other eurozone members, if up domestically and other international. This might have been a euro-negative but instead the market chose to focus on quite good German retail sales. This probably shows an anti-dollar bias as much as a pro-euro sentiment, but is not really supported by the data.

The point is likely to emerge that the Fed leads the world and sets the tone. If what Trump wanted was a stock market recovery (for a while), he is probably going to get it. We see normalization in oil and gold, too. We can't neglect that Powell said he sees the US economy moving with momentum, and postponing rate hikes is a good way to keep that momentum going. If we start getting hard data that shows momentum, sentiment toward the dollar can shift back to positive, maybe as soon as tomorrow (turnaround Tuesday). The ISM report today is likely to show a drop, but never mind. The mood is shifting. We imagine the FX market will accept and cheer Mr. Powell and we will see it in a rising dollar, unless Trump throws another temper tantrum about the China trade talks. And if the negotiators report progress tomorrow or Wednesday, the dollar can rally like crazy.

Fun Tidbit: The Economist features "The Trump Show, Season Two" on the cover and repeats all the derogatory words of the past two years to describe the Wrecker-in-Chief. Instead of toppling the self-serving Washington elite, "...the president's bullying, lying and sleaze have filled the swamp faster..." The Economist writes "If the federal government really were a business, the turnover of senior jobs in the White House would have investors dumping the stock." Trump is "self-absorbed, distracted and ill-informed" according to his own (now-departed) staffers.

Another New Yorker article is ostensibly about Mark Burnett, the producer of the "Apprentice" TV show starring Trump, but really about Trump and how Trump was universally despised by all the production teams. Nobody associated with the show voted for him. Jimmy Kimmel said the TV shows was what make Trumps' candidacy even remotely possible, because everyone knew Trump was a tacky con artist, blatantly pushy of his brands--and not actually rich. (He was declaring bankruptcy during the show's run.) Fran Liebowitz said "Trump us a poor person's idea of what a rich person is." The show was supposed to be camp, but the masses failed to see the humor and took it seriously, to all the producers' surprise. The show rented a floor in Trump Tower and found nobody would provide services because Trump had stiffed them all. Trump couldn't keep to a script and shows were edited from the ending back to a beginning that never happened to accommodate Trump's impulsive changes.

None of this is new. We get two points from the very fact that magazines are still writing about Trump. First, Trump is so awful that—like the proverbial train wreck—we keep watching. It's his very awfulness that demands attention. That means we will be watching even after he is gone from office. We can hardly expect him to fade decently and with dignity into the background like the Bushes and Obama. Secondly, it's going to get worse. The need to feed the narcissistic ego can only grow larger.

Interestingly, it stops short of Trump starting a war. He may not be the "stable genius" he claims, but he's not totally stupid, either. He's a bully, and bullies back down when the fur flies. He also knows that he who starts a war without an unquestionable provocation will go down in the history books as a failure, even if he wins the war. The majority of us know Trump is going down in the history books as the very worst president ever, but Trump seems not be know that. He thinks he has a chance (remember when he said he was the equal of Lincoln?).

Unless we put on our tinfoil hats and imagine Trump is goading the N. Koreans to attack first—shades of Pearl Harbor—we are likely safe from this worst outcome of the Trump presidency. We feel confident he is not goading the N. Koreans to war because Trump doesn't have a Plan of any sort on any subject. He may goad one day but be best friends forever with Kim the next day, as we have already seen. He may also fear the military will rise up and disobey the Commander-in-Chief, calling him incompetent to make the war decision and resigning en masse or something equally embarrassing. Trump feels inadequate and the one thing a narcissist fears the most is looking foolish in public. He is, of course, right that he is inadequate.

Note: The table showing the percentage of oil imports as a percentage of the trade deficit has not been updated since July 2018. This is probably due to the Trump administration preferring to invent data than to collect and report it. We have a space on the page. Suggestions welcome.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat