The Bank of Canada can taper because the Federal Reserve will not

- Bank of Canada leaves interest rate steady at 0.25%, raises economic outlook.

- Reduces weekly purchases of government bonds from C$4 billion to C$3 billion.

- Canadian bond yields rise,10-year gains 2 basis points to 1.525%.

- US 10-year Treasury return stays flat at 1.56%.

- USD/CAD falls more than a figure but holds within recent ranges.

- Dollar was mixed, US equities gained and Treasury yields were little moved.

Canada became the first government to begin withdrawing pandemic financial support when the central bank announced a 25% reduction in its weekly government bond purchases on Wednesday, despite leaving its base rate unchanged.

The Bank of Canada (BOC) sharply upgraded its economic outlook saying that it expects the pandemic will be ‘less detrimental” to the economy than previously estimated.

“Activity has proven more resilient than expected in the face of the COVID-19 pandemic,” noted the statement accompanying the decision.

The governors now expect that all of the slack from the pandemic will be made good in the second half of 2022.

“We remain committed to holding the policy interest rate at the effective lower bound until economic slack is absorbed.... Based on the Bank’s latest projection, this is now expected to happen some time in the second half of 2022,” said the statement.

The overnight rate was left at 0.25%, as universally expected, but the timetable for the first increase has moved up to next year.

Previously, the bank had predicted that the economic slack would not be overcome until 2023, delaying the first rate increase.

While a reduction in its bond purchases had been signalled by Bank Governor Tiff Macklem and member Toni Gravelle in recent speeches, the C$1 billion cut in weekly government bond purchases to C3 billion, is the first move by any central bank to pull back a portion of the extraordinary monetary and rate support of the last year.

In the US the Federal Reserve remains committed to its $120 billion a month purchases program.

Economic growth

Canadian economic growth is expected to be 6.5% in 2022, up from the BOC’s January forecast of 4%.

Some of that expansion is pulled forward from 2022 where GDP was lowered to 3.7% from 4.8%, as reported in the separate spring Monetary Policy Report issued the same time as the rate decision. The report expecteds US growth to be 7% this year.

The Federal Reserve’s own estimate for US GDP this year was 6.5% in its March Projection Materials, with an update due in two months at the June 15-16 FOMC meeting.

The Atlanta Fed’s GDPNow model for the first quarter is 8.3% (anualized).

Market response

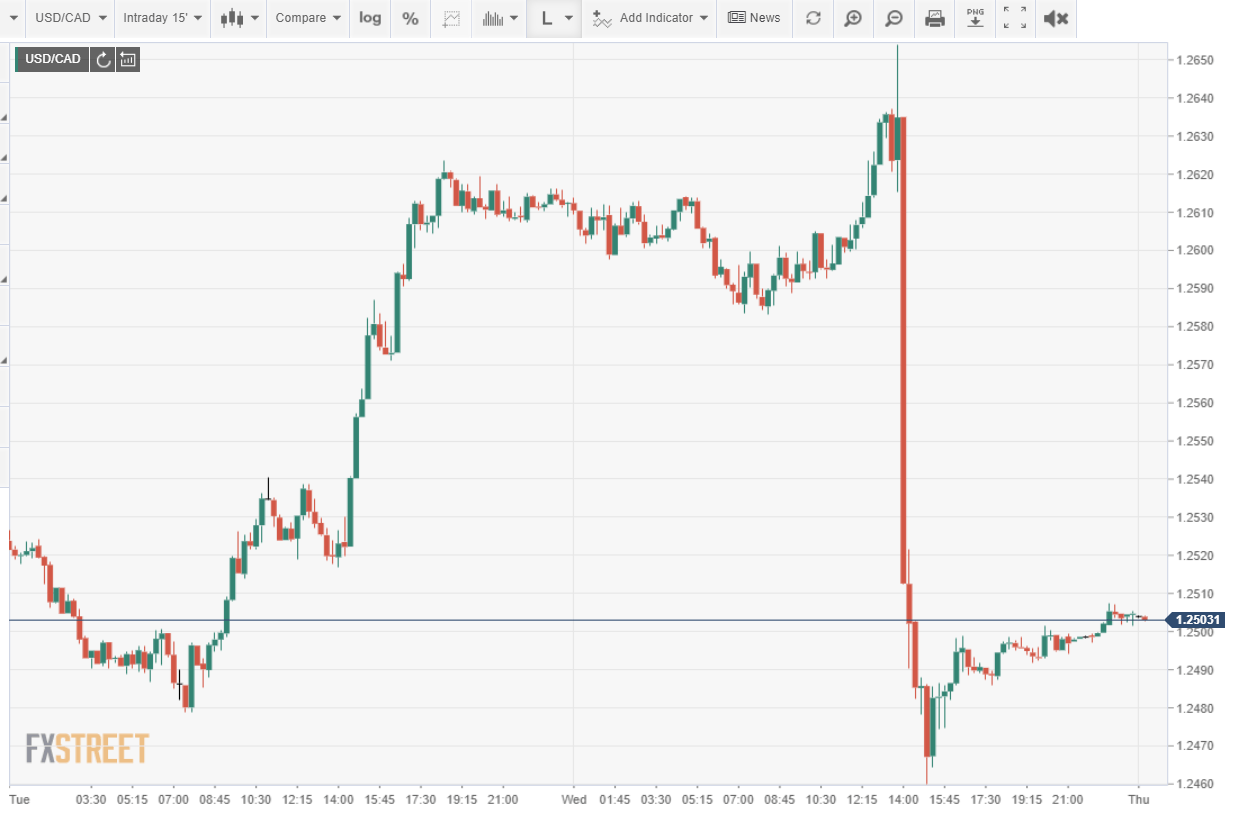

Despite the widespread expectation that the BOC would cut its bond purchases, the USD/CAD responded vigorously dropping from 1.2635 at the announcement to 1.2512 in the first thirty minutes and continuing to a low of 1.2460. The pair closed at 1.2498 in New York.

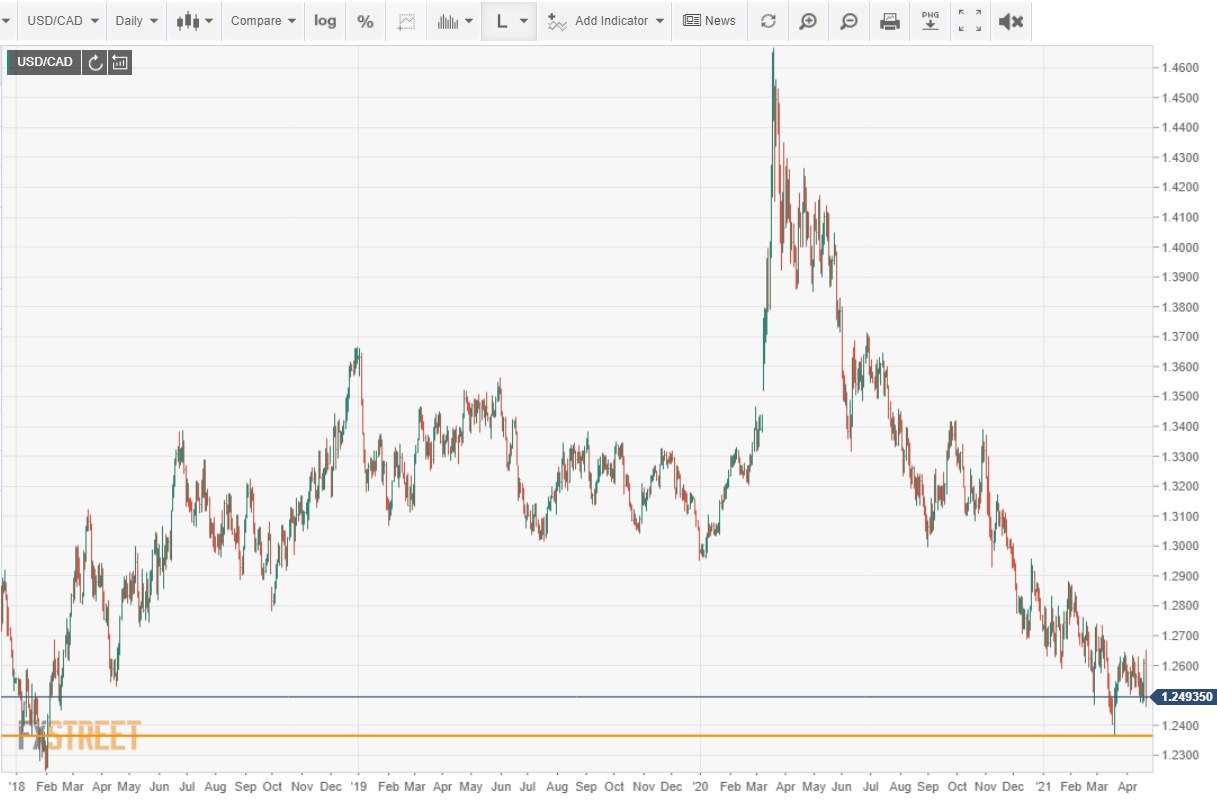

The USD/CAD closed at the bottom of its four-week range but it is still more than a figure above the three-year March 18 low of 1.2365.

American dollar weakness was limited to the Canadian pair. The EUR/USD barely moved, opening at 1.2038 and finishing at 1.2036. The USD/JPY traversed but five points from 108.18 to 108.13. The sterling lost 46 points against the greenback from 1.3986 to 1.3940 and the AUD/USD rose from 0.7726 to 0.7753.

Credit markets were also unimpressed.

The Canadian 10-year bond rose 2 basis points to 1.525%, and its US equivalent was unchanged at 1.559%. The pandemic high close for the Canadian bond was 1.607% on March 18 and for the US 1.746% on March 31.

Canada 10-year bond yield

CNBC

US 10-year Treasury yield

CNBC

Equities shrugged off the BOC implications for US rates. The Dow gained 316.01 points, 0.93% to 34,137.31. The S&P 500 added 0.93%, 38.48 points to 4,173.42 and the NASDAQ climbed 163.95 points, 1.19% to 13,950.22.

S&P 500

CNBC

Employment

One factor that facilitated the BOC action was Canada’s achievement in restoring employment.

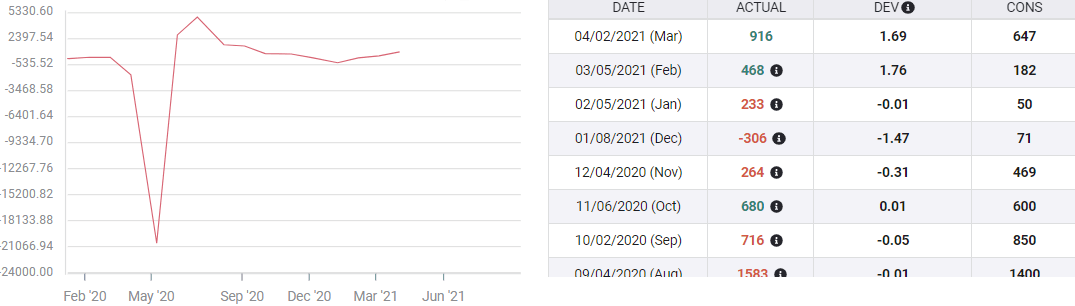

The US has rehired 64% of the 22.4 million Nonfarm Payrolls jobs lost in the March and April lockdowns, leaving about 8.4 million still out of work. At the first quarter job creation rate of 1.617 million, it would take about five-and-a-half months to put everyone back on the payroll.

Nonfarm Payrolls

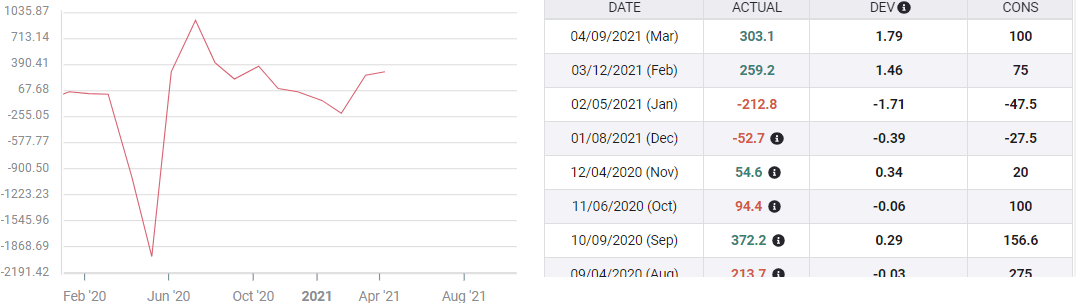

In contrast, Canada’s Net Employment Change list has recovered 90% of its losses with just 296,000 left unemployed.

Net Change in Employment

FXStreet

Conclusion

While Canada’s success in returning the vast majority of its workers to employment is a credit to its economic and fiscal policies, the slower job recovery in the US, with its vastly larger economy and global central bank, is providing an unexpected benefit.

Would the BOC be able to curtail its stimulus and rate repression if its Washington counterpart was not pumping $120 billion a month into the US Treasury market and economy?

The Federal Reserve has promised to maintain its economic support until the economy and employment are, in its words, “fully recovered.”

Washington has unleashed trillions of dollars in fiscal stimulus and the Federal Reserve's bond program has kept the short end of the yield curve pinnned near its historical low.

The US and Canadian economies are the most intertwined in the world. That flood of spending and liquidity will, in short order, have almost as much impact on the Canadian economy as on the US. To a large degree, Canada can reduce its economic support because the US is not.

Another facet of the market response is the recognition that the shift in the BOC bond program signals the same move, somewhat delayed, from the Fed.

As the US economy improves, Treasury rates will resume their ascent. Later, or perhaps sooner, the Fed will acknowledge the development and begin its own taper.

But by that time, the US Treasury yields will already have made the change manifest.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.