The Bank of Korea stands pat, highlighting its neutral stance

As widely expected, the Bank of Korea kept its policy rate at 2.5%. Upward revisions to 2026 growth and inflation forecasts suggest there's little justification for maintaining an easing stance. We expect the BoK to hold rates steady throughout 2026. The odds of a hike in the fourth quarter will increase if growth and prices accelerate more than expected.

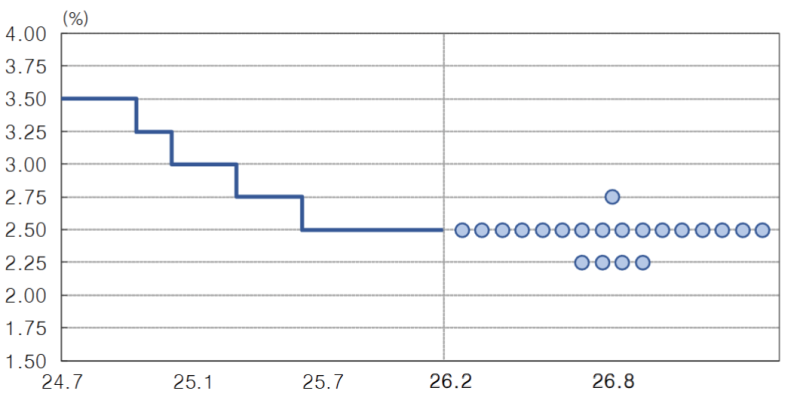

The Bank of Korea ended its easing cycle, highlighting a neutral stance

Today's signals from the Bank of Korea remain quite balanced. It stood pat and clearly closed the door for additional easing. There were no hints of a rate hike on the horizon. The BoK announced its first 6-month dotplot framework, similar to the US Federal Reserve. It shows the median rate outlook stays at 2.5%. The dotplots suggest the risks are skewed to easing with four dots at 2.25%. Yet this leaning is not meaningfully strong. Also, in the three-month guidance, no member considered a rate hike.

Bank of Korea's dotplot suggests a 2.5% policy rate in six months

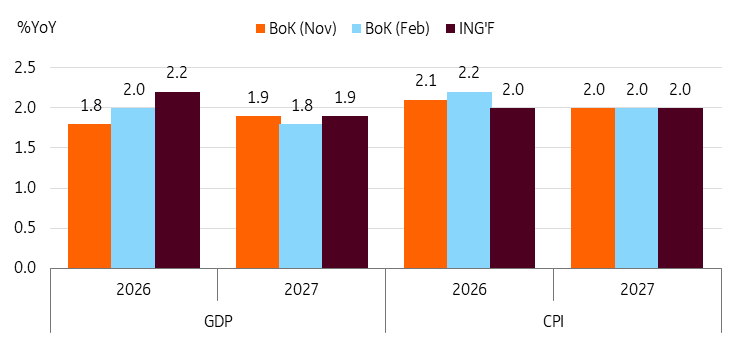

The Bank of Korea revised up GDP and CPI outlook for 2026

The BoK revised upward 2026 GDP from 1.8% year-on-year to 2.0% and CPI from 2.1% to 2.2%. A stronger-than-expected semiconductor cycle is likely to boost exports and investment. Meanwhile, the recent surge in DRAM prices is likely to put additional pressure on inflation. The BoK expects negative GDP gap to narrow but persist this year. It’s expected to turn positive in the second half of 2027. Regarding inflation, the recent surge in DRAM prices has already started to push up producer prices. This is likely to be reflected in consumer prices with time lags. How much of the cost increase will be passed on to consumers is still in question, but a rise is inevitable. In addition, the recent strong performance of the equity market is likely to boost wealth effects, which may build up demand-side inflationary pressures. We have revised up CPI forecasts to 2.0% from the previous 1.9%, but risks are open to the upside.

Bank of Korea revised up its GDP and CPI outlook for 2026

BoK watch

We expect BoK to resume its rate hikes in 2027. Macroeconomic conditions -- such as growth above potential and firm inflation -- could justify hikes even earlier, perhaps in the fourth quarter. As we expect GDP to grow 2.2% in 2026, stronger than the BoK's own estimation, the negative output gap may close as early as end of 2026. However, a K-shaped recovery is expected to continue, as the imbalance between the IT and non-IT sectors widens. This should limit the risk of earlier-than-expected BoK hikes.

In addition, it is also important to consider financial stability. The government tightened housing rules, which are expected to stabilise housing prices in Seoul. The data will be confirmed around June/July.

Another key variable to watch is the possible change in board membership. Three members are set to retire in 2026: Governor Rhee Chang Yong in April, Deputy Governor You Sang Dae in August, and Shin Sung Whan in May. Once the reshuffle happens, the direction of monetary policy will likely become clearer.

At this time, our base case assumes no changes in rates throughout 2026.

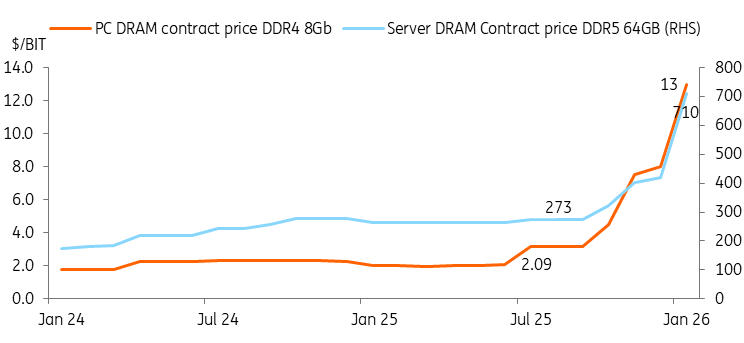

DRAM price surge likely to trigger 'chipflation"

KRW trends toward appreciation

As we argued in our FX monthly, the KRW is on an appreciation path after the unusual weakness we saw in 2025.

The KRW appreciated significantly in February. While global dollar weakness played a role, several factors specific to Korea also supported the won. The strong performance of Korean chipmakers attracted both domestic and international investors, leading to increased capital inflow. The government’s various FX stabilisation measures helped control FX flows. Today’s news on possible dollar bond issuance by the National Pension System (NPS), if materialised, should help ease dollar demand pressures. Additionally, the upcoming WGBI inclusion beginning in April is expected to further benefit the KRW. The USDKRW broke 1,420 at the time of writing, and the pace of appreciation has been faster than expected. Nvidia's positive outlook on AI should boost the KRW appreciation further today. We anticipate the USDKRW will stabilise around 1,435 in the near term and then strengthen to 1,375 by the third quarter of 2026. We expect investment commitments to the US to be implemented during the second half, contributing to a more balanced supply-and-demand environment, thus setting the 1,400 level by year end.

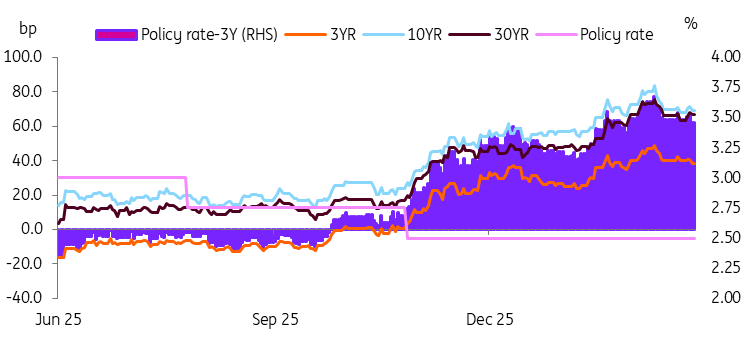

KTB: Overreaction is expected to normalize

Korean treasury bond (KTB) yields had been shooting upward since November until very recently. We recognise that market volatility is normal when the direction of the central bank's policy changes. However, in our view, the recent market pricing was somewhat overdone. Governor Rhee also mentioned that the current interest rate level is excessive and that the new six-month dot-plot guidance is likely to provide the market with more long-term guidance. We expect KTB yields to decline as market concerns over an immediate rate hike subside. The inclusion in the WGBI in April is expected to bring in additional capital. Also, even if the government drafts a supplementary budget later in 2H26, we would not expect additional debt issuance, given that government revenue is stronger than expected. We expect 10YKTB to move toward 3.25% in 1H26.

Spreads are expected to narrow on the back of neutral policy stance

Read the original analysis: The Bank of Korea stands pat, highlighting its neutral stance

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.