The AUD can’t get a break

Outlook:

We get the newest Atlanta Fed forecast of Q4 GDP tomorrow, but now that we have the virus outbreak that can turn into a global epidemic, it may have little value by the time we get the official "advance" Q4 GDP on Thursday. We will still want to see business investment and PCE, with personal income and spending on Friday. We get a ton of other data—see the calendar—with the same warning now attached. And oh yes, there is a Fed policy meeting this week. No change is expected.

Similarly, no change is what we should expect from the BoE policy meeting on Thursday, for several reasons. First up is that Brexit becomes official the next day, Jan 31. That may be only symbolic at this point, but a rate cut one day before the official date would sent a message of impending weakness due specifically to Brexit. Secondly, it's Carney's last meeting and he may think any change—and any change would be drama—belongs to the next guy. Third, data indicates that predictions of doom and gloom arising from Brexit were overdone. The prognosis is still for a certain amount of doom and gloom, but not as much as expected, including the inflationary effects of the massive devaluation.

Despite the enormous calendar this week—and note we get a ton of earnings reports, too—one thing not to lose sight of is the month-end. We can easily see re-positioning, including profit-taking, into Wednesday.

So far the currency effect of the Chinese virus is on the yuan itself, the Japanese yen—rising on risk aversion—and the Australian dollar. The AUD can't get a break. Drought and wildfires, and now this. Everyone is quoting the statistic that the SARS epidemic in 2003 cut 3% from Chinese GDP. Goldman says this epidemic can cut $3 off oil prices. CNBC reported that the SARS crisis cost the world economy a total of about $40 billion.

We are not there yet, but unless the new virus is defeated immediately, by which we mean this week, we have to expect a Chinese and global slowdown that will in turn trash German and Australian exports, again, as well as other measures, trade-related and not.

Oddly, in 2003 the US stock market recovered strongly. Conditions were different then—the US was coming out of a slump and the stock market had been wonky—but analysts expect US equities to shrug off this issue, too, despite the scary drop in equity index futures so far this morning.

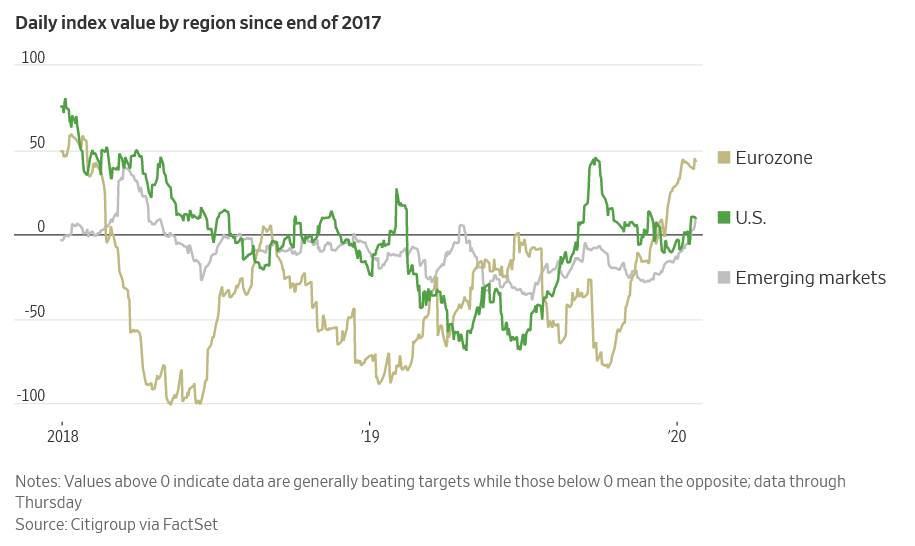

The stock market is not the economy but can usually be counted on to take its temperature. The WSJ today notes that momentum in US equities in particular remains strong, fueled by cheap money but also data coming in better than expected—see the Citibank surprise index chart—and also earnings on a rising trendline since the beginning of the year. We have no reason to suppose any of this is going to reverse and therefore cash keeps flooding into index-tracking funds. We have the usual small number of doomsters but so far their story is not convincing. Sometimes it's not even coherent.

Whenever we have an Event, and the coronavirus outbreak will probably qualify, we have to expect safe haven flows into Treasuries, into the yen and dollar, and into gold. The implied global slowdown hurts oil and other commodities, plus the currencies of those countries dependent on commodities (Mexico, Norway). Equities may be a different matter, with some falling (China, now on holiday and markets closed) and some others shrugging it off (US, UK ex-energy). This is a conventional deduction. The introduction of an additional Big Factor is not priced in. We don't even know what the Big Factor might be.

One well-known analyst (John Taylor, of the defunct FX Concepts) says "The Fed's next move will be a cut and possibly this week using Wuhan as an excuse. The next move will be another cut as well. We see a low in rates in May accompanied by an equity sell-off. If the situation is okay, the rate cuts will work but this is a very risky picture that we see as the dollar shortage outside the US is extremely large and its impact is unclear. Every dollar must flow through the US system and the numbers are 5 to 10 times larger than ever before (2008) and the liabilities are basically unknown. We believe the system is broken as the percentage of US based transactions has dropped and others (often Chinese) have exploded in volume since 2008."

We don't buy the rate cut idea, let alone blaming the Chinese virus outbreak for it—this is not how the Fed behaves. It sees things like disease pandemics and oil prices as beyond its wheelhouse. But what if inflation (PCE) looks soft later this week? A change in sentiment toward the Fed is about the only thing we can imagine that would be dollar-negative. Politics: The Trump defense appeared for only two hours (of its allotted 24) on Saturday in the sneak preview of what we will get next week. It's not very impressive so far. The defense complained about "cherry picking" one part of a conversation and not disclosing the whole thing. Yeah, it's called editing. We do it every day. A good editor doesn't lose context, especially when there is a mountain of similar/corroborating evidence.

The defense claimed the impeachment is to "cancel the 2016 election." This is an effort to arouse emotion among those who voted for Trump, who might feel dismissed or marginalized. But impeachment does not cancel the previous election. It tries to remove someone who has behaved wrongly after being elected and might behave badly again, in this case in the 2020 election. If the impeachment process "cancelled" the election, would we have to hold the same one all over again? Nobody wants to see Hillary again. Ever.

The defense tried the usual "hearsay" argument again and defended the White House refusing all efforts to get first-hand testimony and documents by saying the Committees did not have the authority from the full House vote to issue subpoenas. This is one of those "process" arguments and it's dead wrong. The House issues its rule for every session and the rules this time did allocate to the Committees the authority to issue subpoenas.

On another point, the defense said (again) the Republicans were excluded from secret hearings—clearly not true since they were photographed entering the secure room—modified to a charge of the president not being able to question witnesses in the House proceeding. But he was invited to attend and declined.

Then there was attacking the prosecution for extreme language, like Manager Schiff quoting a Trumper who said Trump is vengeful and would have a nay-sayer's "head on a pike." Just ask any of the "losers" Trump has fired, evidently forgetting he "has the best people." Schiff was reminding Senators that they are being intimidated—which is jury tampering—by threats implicit and explicit of Trump "primarying" them, as he did to Arizona Senator Flake. This entails personal and financial support to an opponent in a state Republican primary. Golly, the GOP is offended by Dem strong language but forgive Trump for his insults?

One former legislator opined on TV that Alaska Senator Murkowski would shrug off head-on-a-pike, despite her comment to the press that she didn't much like it. Murkowski is made of sterner stuff, having won her election as a write-in candidate after the local GOP threw her out. Maine Senator Collins said it's not true. Okay, Susan, prove it. Utah Senator Romney doesn't give a hoot. So, one to go to get witnesses and documents. Many analysts continue to say we may not get witnesses. The issue doesn't come up until Friday and we may not know even then. Never mind. All the facts are going to come out eventually. The Trump legacy is one of shame.

The only part of the preliminary defense that gives us pause is the assertion that Trump did indeed withhold/postpone foreign aid to others and not just Ukraine, harkening back to Chief of Staff's Mulvaney's "we do it all the time." Others treated this way include Lebanon, Pakistan and El Salvador. Ah, but in those cases Trump did not ask for a quid-pro-quo but rather compliance with previously agreed standards. The Trump defense points out he asked Ukraine to "do us a favor," not "do me a favor." This supposedly means Trump was referring to the whole US needing that favor. But the favor consisted of investigating Bidens, and Trump has a perfectly capable CIA/FBI and Justice Dept to do that.

We find the defense quite weak. That doesn't mean it won't influence voters. After all, they presumably believe or forgive at least some of those 15,000 lies Trump has told since taking office. Something new: press reports have it that a draft of the Bolton book is circulating around Washington and Bolton says the aid holdup was directly tied to one thing and one thing only—strong-arming Ukraine into announcing an investigation into the Bidens and the 2016 election. Period. No underlying concern about corruption. Today the WSJ has it as the top story with the front-page blurb "A draft of a book by former national security adviser John Bolton alleges that President Trump told him in August that he wanted to keep aid to Ukraine frozen until the country aided investigations into Democrats." Trump denies ever having any such conversation with or in the presence of Bolton, but Trump has told 15,000 lies since taking office.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports, including the Traders Advisories, send $3.95 to [email protected] using Paypal.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat