Tech bounces back, but earnings must now carry the AI boom

- New York’s tech rebound hands Korea a favourable opening, giving its AI buildout and foundry ambitions fresh oxygen.

- Korea remains a higher-beta version of the global AI trade, with memory, industrial ambition and domestic positioning all magnifying the US move.

- Earnings season is now the real checkpoint, with AI infrastructure expected to drive nearly 60% of S&P 500 EPS growth.

- Hormuz remains a live risk, but physical crude supply still offers enough cushion to limit sustained oil upside unless disruption becomes materially worse.

Tech bounces back

US stocks closed higher into quarter-end, ahead of the structurally important July 1 retirement-contribution reset*, with mega-cap technology back at the front of the parade after spending last week being dragged behind it.

The Magnificent Seven bounced meaningfully into the New York close, with Nasdaq again doing the heavy lifting. After last week’s record selling in big tech, buyers returned to the same names they were throwing overboard only days earlier. That does not mean the AI trade has suddenly been cured. It means the patient stopped bleeding long enough for the surgeons to begin bidding the stock back up.

For Asia, and especially Korea and Japan, that is the handoff.

A firm New York technology close gives Seoul’s increasingly ambitious AI buildout a much cleaner opening. Korea is no longer merely pitching itself as a supplier of memory chips to somebody else’s boom. It is trying to build a larger industrial claim on the whole AI stack: memory, foundry capacity, power, data infrastructure, domestic capital and the strategic ambition to become an AI production hub in its own right.

That makes Korea one of the purest regional expressions of the global AI trade. When New York’s mega-cap complex catches a bid, Seoul does not just follow the move. It tends to amplify it. The KOSPI has become the echo chamber of the AI boom: US capex optimism goes in at one end, memory names, leveraged products and domestic retail enthusiasm come out louder at the other.

That is the appeal. It is also why the market can turn so quickly.

Last week’s tech rout was a reminder that Korea’s AI trade is not simply an earnings story. It is an earnings story wrapped in retail-based hyper-positioning, leverage, and a now-national industrial aspiration. The buildout is real, but so is the sensitivity. If the global AI machine keeps spending, Korea sits close to the engine room. If investors begin questioning the return on all that spending, the same market can behave like a rubber band pulled too far.

Still, the broader US market looked healthier than the weakness in mega-cap tech suggested. The equal-weighted S&P 500 is outperforming the cap-weighted index year to date. Eight of the eleven major sectors rose last week even as the broader S&P 500 fell. The generals were being hit, but the rest of the army did not break formation.

That matters because the AI debate has been reduced to a crude binary. Either hyperscalers keep spending at breakneck speed and equities keep climbing, or capex slows and the market discovers it has been living in a penthouse held up by a very narrow elevator shaft.

Reality is usually messier than the cleanest bear case or the cleanest bull case.

AI spending can remain strong. Earnings can continue rising. Volatility can stay elevated. And the market can still rotate beneath the surface as investors separate the companies selling the picks and shovels from the companies digging the holes, financing the holes and eventually needing to prove there was gold at the bottom.

Nothing in last week’s selling provided hard evidence that AI investment is decelerating. But markets do not wait for the quarterly filing to tell them the music has stopped. When valuations are elevated, they start listening for a change in tempo. They look at every capex forecast, every margin guide and every demand assumption, asking whether the orchestra is still playing or whether the sound is coming from a recording.

That is why the market is moving from macro volatility back toward micro volatility. Oil, geopolitics and inflation had been the thunderstorm outside. Now investors are walking indoors, into earnings season, where every company will be placed under the bright, unforgiving lights of the operating theatre.

Second-quarter earnings season is the next real test.

The S&P 500’s roughly 21% gain over the past twelve months has been driven entirely by earnings rather than valuation expansion. That gives the rally real muscle. But it also means earnings are now the engine, the gearbox and the spare tyre. There is very little room for the machine to cough.

AI infrastructure is expected to contribute nearly 60% of S&P 500 EPS growth this quarter. Micron and NVIDIA alone are expected to account for more than 40% of that contribution. Consensus expects the median S&P 500 company to grow earnings by roughly 9%, while relatively conservative revenue assumptions leave room for upside if demand, pricing and operating leverage prove more resilient than feared.

That is the bullish case. The runway remains open, the engines are still running and the passenger list is full.

But the market is beginning to ask a different question. It no longer wants applause for the size of the investment. It wants a receipt.

Hyperscaler capex still matters, but the more important conversation is shifting toward how much everyone else is spending on AI, how quickly those investments become productive, and whether the return arrives before investor patience runs out. Corporate America has spent heavily building the racetrack. Earnings season will show whether there are enough cars on it.

For Korea, the answer matters more than almost anywhere else. Its AI foundry aspiration cannot survive on the idea of semiconductor scarcity alone. The investment has to become orders, the orders have to become earnings, and the earnings have to justify both the capital expenditure and the excitement now being built around it.

Monday’s rebound had the familiar feel of a crowded unwind reversing. Big-tech dip buyers filled their boots after last week’s selling. Nasdaq led. 0DTE flows reportedly faded the initial move before being squeezed into cover as equities pushed higher. Bonds and the dollar barely moved. Oil rose on fresh tit-for-tat strikes and the absence of meaningful talks. Bitcoin traded higher but choppy. Gold slipped.

It was one of those sessions where the market says everything is fine, then quietly checks the nearest fire exit.

For now, investors appear willing to treat the weekend’s geopolitical escalation as another flare rather than a structural break. Iran remains determined to challenge transit through Hormuz, but the physical crude market is still better supplied in the near term than the headlines suggest.

That explains why equities could rise even as crude firmed. The market is not pricing peace. It is pricing less uncertainty than feared.

The calendar adds one final wrinkle. This was quarter-end, half-year-end and the opening act of a shortened US holiday week. Institutional rebalancing can create sharp bursts of volatility, especially after such a powerful quarter for risk assets.

That leaves the market walking a narrow ridge.

The rally has survived war, oil shocks and inflation scares. The AI trade has survived another violent clearing event. New York has reopened the door for the AI complex. Korea will now test just how much of that optimism it can turn into an industrial and market story of its own.

For FX traders eyeing the scary yen headlines in Bloomberg Yen hits 40-year low in historic slide that’s rattled Japan, a little perspective is required.

Yes, USD/JPY edged to its highest level since 1986, with the dollar nearing ¥162. But the move itself was barely more than 20 pips in overnight trading terms. That is enough to print a dramatic headline at these levels, but not enough on its own to declare that a fresh dollar breakout is under way.

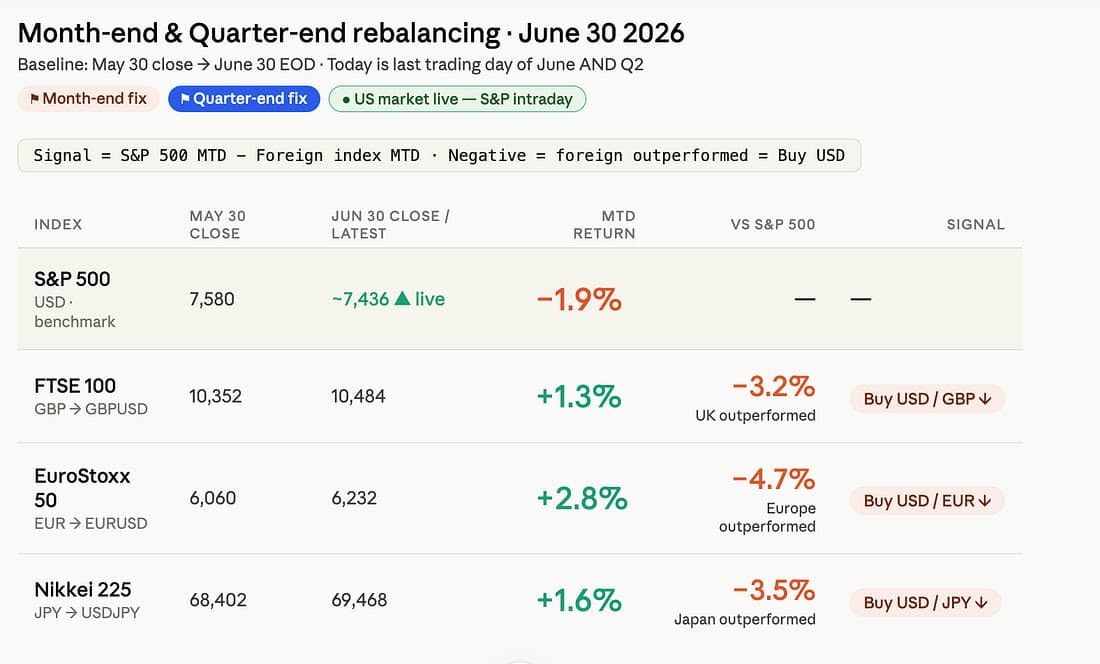

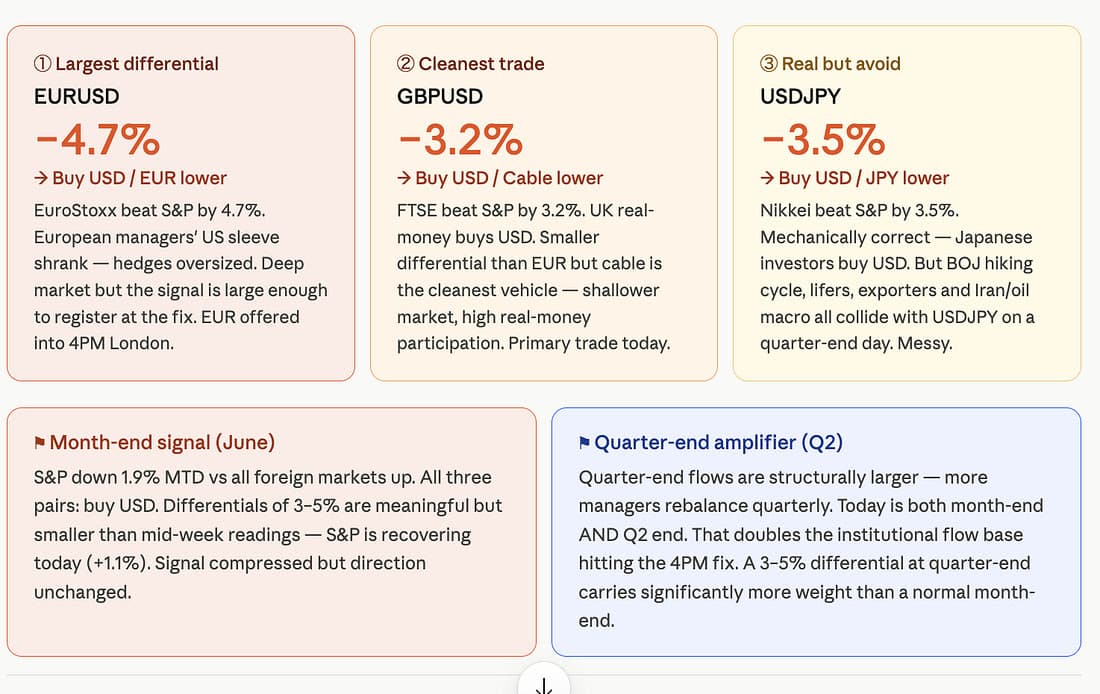

The timing matters. This was quarter-end, and much of the late move appeared to be tied to benchmark-related demand that might trigger like a gangbuster today at the WMR 4:00 p.m. London fix. Month- and quarter-end portfolio rebalancing can push sizeable currency flows through a narrow window, particularly when global equity performance and hedging ratios have shifted sharply. The fix is a benchmark execution point, not a central-bank signal.

That does not make the yen story harmless. Trading at a forty-year low keeps Tokyo’s intervention risk firmly on the screen, and traders should never pick nickels in front of intervention. But it does mean the first question is not whether USD/JPY touched a scary number. It is whether the market can hold above it once the quarter-end machinery is switched off against the now likley intervention backdrop, the higher we trade + ¥162

Here is my month-end signal, which doesn’t always work but is worth keeping an eye on. It’s relevant when equity market differentials are steep enough. My primary signal is triggered when the US market needs to rebalance, based on a pure -2.5% drop. This setup is only for the short window around the WMR fix and should never be taken as gospel. It should be used by most as a positioning enhancer, not a pure PnL generator, even if I trade heavily around it.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.