Just like Fed, is BoJ’s independence under threat?

When talking about central bank independence, most of the focus has been on Donald Trump’s pressure on the Federal Reserve. But a similar story, a quieter one for now, seems to be happening on the other side of the Pacific: Japan’s government may be testing the Bank of Japan’s independence just as the country tries to leave decades of ultra-loose monetary policy behind.

Welcome to another chapter of politics meddling in central bank decisions.

Donald Trump and the Fed, the most recent precedent

Since the return of Donald Trump to the White House in January 2025, one man he has criticized and has threatened to lay off several times is the former Federal Reserve (Fed) Chairman Jerome Powell. All these reprimands were for a simple reason: not lowering interest rates quickly, as Trump desired.

To increase his control over Federal Open Market Committee (FOMC) voting, US President Trump also appointed one of his top economic advisors, Stephen Miran, to fill the remaining time in former Fed Governor Adriana Kugler’s term, who stepped down after she was accused of violating the central bank’s ethics rules. During his term, Miran always went against the grain and voted for large interest rate cuts, while others called for caution due to Trump’s tariff policies.

Meanwhile, the nomination of current Fed Chair Kevin Warsh by US President Trump, who was confirmed in May this year, was also made on the expectation that he would pursue his economic agenda – lowering interest rates.

US President Trump also faced criticism from several global and central bank leaders for publicly criticizing former Fed Chair Powell and attacking the Fed's autonomy, calling it damage to the central bank’s independence. This also raised concerns over the credibility of the US Dollar (USD), Treasury Yields, and other US assets.

Takaichi pushes central bank to align with government

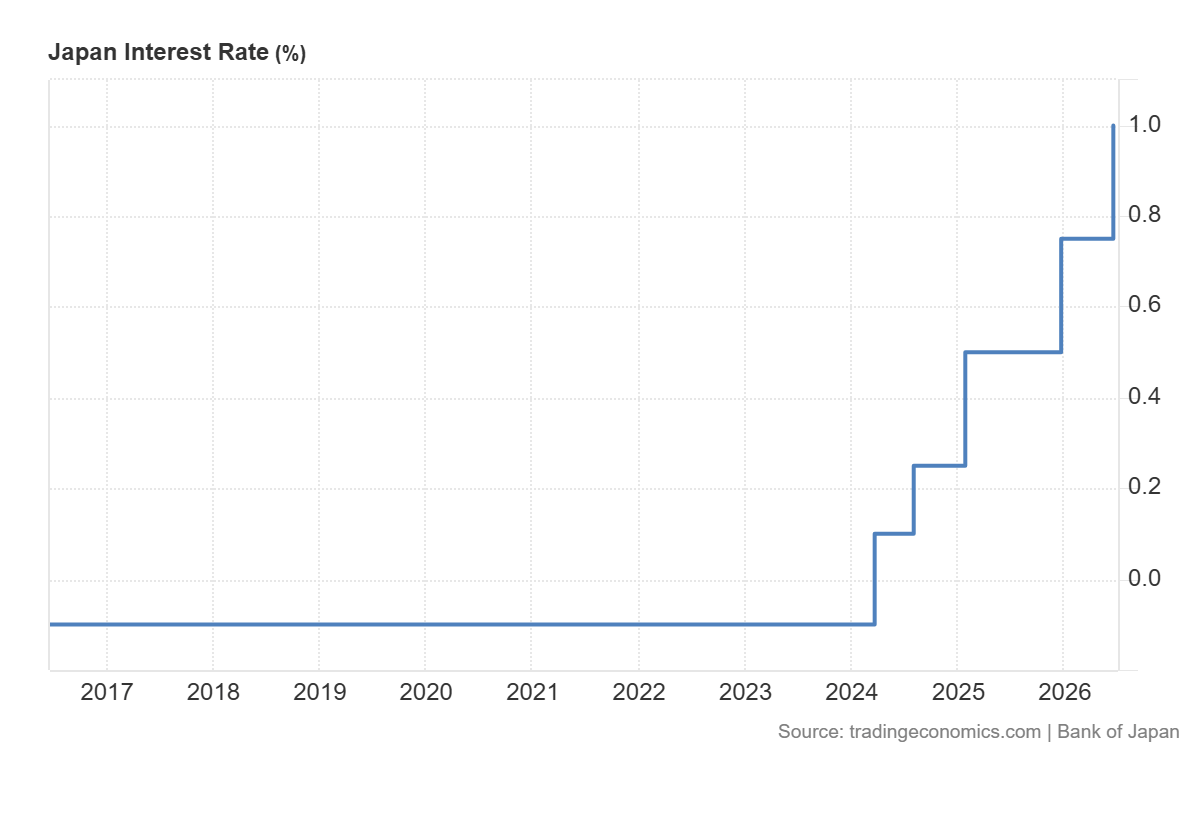

In the last Bank of Japan (BoJ) June policy meeting, the majority of officials decided to raise interest rates by 25 basis points (bps) to 1%, as markets expected, bringing the rate to its highest level in 31 years.

However, the Summary of Opinions (SoP) of the meeting showed that the decision wasn’t unanimous: Prime Minister Sanae Takaichi’s newly appointed board member, Toichiro Asada, was the only one voting against the interest-rate hike, citing risks to output and jobs from the Middle East conflict.

"The downside risks to production and employment may disrupt the virtuous cycle between wages and prices. In the worst-case scenario, this could potentially push Japan back to deflation," one member was quoted as saying in the summary, while the view is widely seen as that of Asada, Reuters reported. This leaves little doubt about his commitment to Takaichi’s desires to stick with an ultra-loose monetary policy.

While disagreements among central bank officials are notorious and normal, the dissent vote by Asada – the appointee of a prime minister who very explicitly has vowed to abandon austerity in favor of aggressive fiscal expansion – has raised eyebrows.

Market experts view the BoJ Asada’s dissenting vote as political pressure from Tokyo, which has been seen as supporting loose fiscal conditions.

“The dovish dissenting vote by Asada and the BoJ’s decision this month to halt bond tapering next fiscal year may reflect the influence of political pressure to some extent,” analysts at JP Morgan said.

After a landslide victory in general elections last year, PM Takaichi said in a policy speech in the Parliament that the new government will break “excessive fiscal austerity” and won’t hesitate in increasing spending in areas like artificial intelligence (AI), chips and shipbuilding to lift Japan's potential growth, Reuters reported.

Takaichi’s leadership campaign also included a mission to revive former Japanese PM Shinzo Abe’s economic vision of cheap borrowing and high public spending, also known as “Abenomics”.

Hours before the June rate hike by the Bank of Japan, economic policy minister Minoru Kiuchi said he “strongly” expected the central bank to “coordinate closely” with the government, the Japan Times reports.

The Yen doesn’t like doves in the BoJ

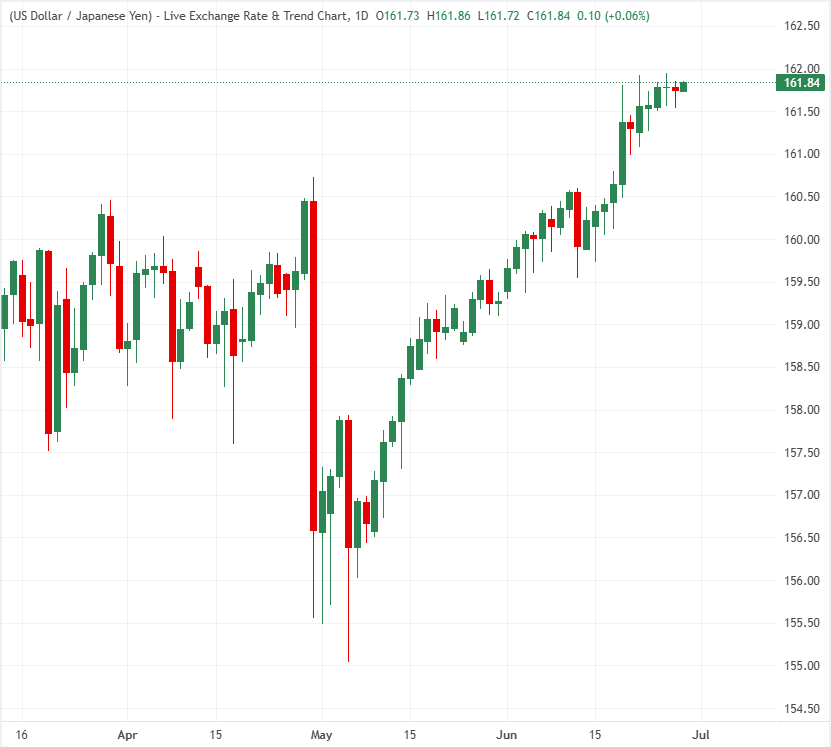

Asada could be the first of many doves to land in the Bank of Japan. Knowing the fact that PM Takaichi is set to fill one more member to the BoJ’s board as a replacement for Junko Nakagawa – whose tenure will be completed in a few days – and two more by the year-end, this scenario could prove to be even worse for the Japanese Yen (JPY), which is already close to 162.00 against the US Dollar, the lowest level seen in over 40 years.

In this context, market experts believe that the BoJ could fasten the monetary tightening pace before the arrival of more doves at the helm.

“The BOJ may not have much time left to continue raising rates toward the neutral rate,” analysts at Mitsubishi UFJ Morgan Stanley Securities said. “It may therefore try to reduce the degree of monetary accommodation as much as possible by next summer.”

Meanwhile, the BoJ SoP of the June policy meeting also showed that one board member said Japan's policy rate must be brought “closer to the estimated neutral rate of around 2% at a pace of once every few months.

The more the BoJ looks constrained by politics, the harder it will be to keep confidence in the Yen. Japan’s exit from ultra-loose policy was never going to be smooth, but if central bank independence becomes the next casualty, the turbulence for the Yen seen so far may only be a little taste of what’s to come.

Bank of Japan FAQs

The Bank of Japan (BoJ) is the Japanese central bank, which sets monetary policy in the country. Its mandate is to issue banknotes and carry out currency and monetary control to ensure price stability, which means an inflation target of around 2%.

The Bank of Japan embarked in an ultra-loose monetary policy in 2013 in order to stimulate the economy and fuel inflation amid a low-inflationary environment. The bank’s policy is based on Quantitative and Qualitative Easing (QQE), or printing notes to buy assets such as government or corporate bonds to provide liquidity. In 2016, the bank doubled down on its strategy and further loosened policy by first introducing negative interest rates and then directly controlling the yield of its 10-year government bonds. In March 2024, the BoJ lifted interest rates, effectively retreating from the ultra-loose monetary policy stance.

The Bank’s massive stimulus caused the Yen to depreciate against its main currency peers. This process exacerbated in 2022 and 2023 due to an increasing policy divergence between the Bank of Japan and other main central banks, which opted to increase interest rates sharply to fight decades-high levels of inflation. The BoJ’s policy led to a widening differential with other currencies, dragging down the value of the Yen. This trend partly reversed in 2024, when the BoJ decided to abandon its ultra-loose policy stance.

A weaker Yen and the spike in global energy prices led to an increase in Japanese inflation, which exceeded the BoJ’s 2% target. The prospect of rising salaries in the country – a key element fuelling inflation – also contributed to the move.

Author

Sagar Dua

FXStreet

Sagar Dua is associated with the financial markets from his college days. Along with pursuing post-graduation in Commerce in 2014, he started his markets training with chart analysis.