Australian Dollar Price Forecast: Tiptoeing into uncharted territory

- AUD/USD remains weak, breaking below the 0.6900 support.

- The US Dollar continues its correction, revisiting multi-day lows.

- Next on tap in Oz will be the release of the RBA Minutes of the June event.

The Aussie Dollar continues to lose momentum, remaining unable to not only find a catalyst that prevents the currency from falling further but also reverse course and at least start trimming its recent weakness Meanwhile, developments in the US Dollar and geopolitics appear to have weighed on the Aussie, leading to a correction in AUD/USD to below 0.6900 and raising the possibility of a test of the critical 200-day SMA.

The Australian Dollar (AUD) has practically faded the rally seen from late March to mid-May, motivating AUD/USD to clinch its seventh day in a row of losses and breach below the 0.6900 support level, hitting multi-week troughs and paving the way for a probable visit to its critical 200-day SMA around 0.6850 sooner rather than later.

Another dreadful day for the risk complex sees the US Dollar (USD) gather extra steam and advance to levels last seen in May 2025 well north of the 101.00 barrier when gauged by the US Dollar Index (DXY), always in response to steady bets that the Federal Reserve (Fed) might eventually hike its interest rates in the second half of the year.

In addition, the persistent scepticism surrounding the recently clinched US-Iran deal appears to have removed, albeit for now, the geopolitical premium from global markets.

Domestic economy still holds up

The Australian economy does look healthy and stable altogether and, honestly, in much better shape than many of its G10 peers.

This performance appears underpinned by a solid domestic demand and pretty decent figures when it comes to economic growth. The spectre of sticky inflation seems to justify the cautious and data-dependent stance from the Reserve Bank of Australia (RBA), particularly following the latest meeting, where it raised rates to 4.35%, broadly in line with market expectations.

Supporting the above, the preliminary data from the June Purchasing Managers’ Index (PMI) showed Manufacturing at 51.2 (from 50.7) and Services at 49.9 (from 48.7).

Adding some colour to the domestic fundamentals, the latest trade balance figures showed a A$1.791 billion surplus in April, reversing March’s A$1.024 billion deficit. The latest Gross Domestic Product (GDP) data, meanwhile, kind of disappointed expectations: the economy expanded by 0.3% QoQ in Q1 2026 (from 0.9%) and 2.5% YoY (from 2.5%), both prints missing consensus.

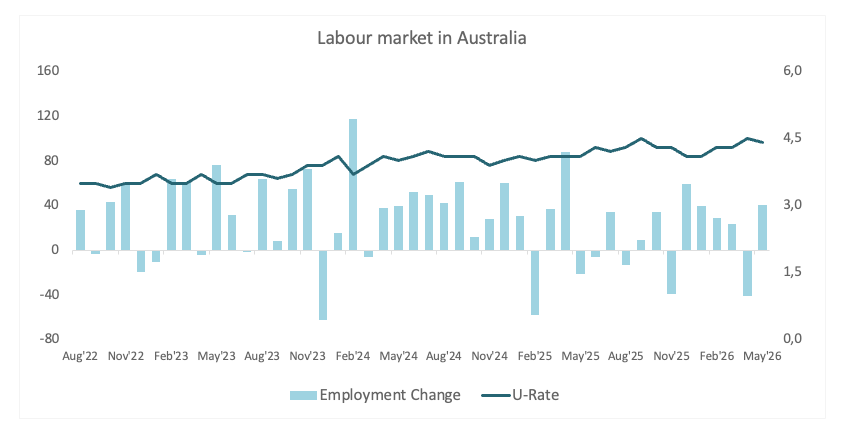

Still on the bright side, the labour market remains healthy. Indeed, the Unemployment Rate ticked lower to 4.4% in May (from 4.5%), and the Employment Change increased by 40.6K individuals (from the revised 40.7K drop seen in the previous month).

Regarding inflation, May data was far from telling after the Consumer Price Index (CPI) ticked lower to 4.0% from a year earlier (from 4.2%), while the Trimmed Mean and the Weighted Median rose to 3.6% over the last twelve months (from 3.4%). The pace of disinflation remains weak, although the direction is still broadly correct. Somehow reinforcing that view, the latest Melbourne Institute’s Consumer Inflation Expectations eased to 5.5% in May (from 5.6%).

For the RBA, that means the job is still incomplete, as policymakers continue to signal that inflation may only return to target around mid-2028, keeping the focus firmly on patience rather than any imminent pivot.

Looking ahead, investors expect the central bank to maintain its current stance at its August meeting, while they now anticipate just around 10 basis points of tightening by year-end.

China offers stability, not lift

China now looks more like a stabilising force than the tailwind it usually provides to the Australian economy.

Let’s see some numbers: the economy expanded by 5.0% YoY in Q1, while Retail Sales unexpectedly contracted by 0.6% in the year to May but expanded by 1.41% since January. In addition, Industrial Production exceeded expectations last month after expanding by 4.5% from a year earlier.

Of note is the strong recovery of the trade balance, with May’s surplus widening to $105.43 billion from around $84.8 billion in the previous month and both imports and exports expanding markedly.

However, business activity seems to be regaining traction after the National Bureau of Statistics (NBS) reported Manufacturing PMI at 50 in May (from 50.3), while Services returned to the expansion territory at 50.1 (from 49.4). At the same time, private gauges such as RatingDog still point to expansion, with Manufacturing coming in at 51.8 and Services improving to 54.4.

The disinflationary trend in China seems to have re-emerged after the CPI disappointed expectations and rose by 1.2% in the year to May, matching the previous reading. On a monthly basis, prices dropped by 0.1%, while Producer Prices gained 3.9% over the last twelve months, also holding steady from April’s prints.

In the meantime, and matching the broad consensus, the People’s Bank of China (PBoC) kept its Loan Prime Rates (LPR) unchanged at 3.00% for the one-year tenor and 3.50% for the five-year tenor at its event earlier on Monday.

In summary, China is no longer pushing growth higher, but it is not dragging it down aggressively either. It is simply keeping things steady.

The RBA keeps its powder dry

As broadly awaited by market participants, the RBA left its Official Cash Rate (OCR) unchanged at 4.35% at its event early on Tuesday.

The Reserve Bank of Australia adopted a hawkish stance at its June meeting, reiterating that inflation remains too high and cautioning that more rate rises may yet be necessary if price pressures persist. Policymakers also noted continuing concerns from increased energy costs and underlined their commitment to preventing inflation from becoming entrenched.

That said, Governor Michele Bullock was a little more measured in tone at her press conference. She kept the option of additional tightening open but said the incoming data had generally progressed as expected and showed the Board did not need to tighten at this meeting. The economy is not entering a recession, and the employment market is still reasonably tight, she said.

The message in general was one of cautious tolerance. Inflation is still the bank's biggest worry, but officials seem more satisfied with the progress made so far and prepared to let past rate rises have more time to work through the economy. Further tightening is feasible, but the bar for another rate rise appears higher than the phrase alone may lead one to expect.

AUD/USD: Upside intact, conviction fading

Base case

While above its key 200-day SMA around 0.6850, the pair’s outlook is expected to remain tilted to further advances. However, for such a scenario to materialise, it needs a strong catalyst to emerge and feels heavily dependent on the broader backdrop: without a sustained improvement in risk sentiment or continued US Dollar weakness, the probability of extra gains could start to lose momentum.

Bull case

Further conviction is needed. If risk appetite picks up serious pace, spot should meet the initial hurdle at the psychological 0.7000 barrier, ahead of the 0.7200 yardstick before reaching the 2026 peak near 0.7280, just ahead of the minor 0.7300 barrier. Further up, the 2022 ceiling at 0.7593 awaits. Speculative positioning seems to be leaning toward this scenario for now.

Bear case

In the current volatile context, we should not rule out the loss of further momentum. If sentiment deteriorates, the Greenback gains extra momentum, or Chinese data continue to disappoint, spot could recede further and initially challenge its critical 200-day SMA near 0.6860.

The eventual recovery appears more distant in the current context, and it seems market participants are taking notes of these developments.

Positioning unwind gathers pace

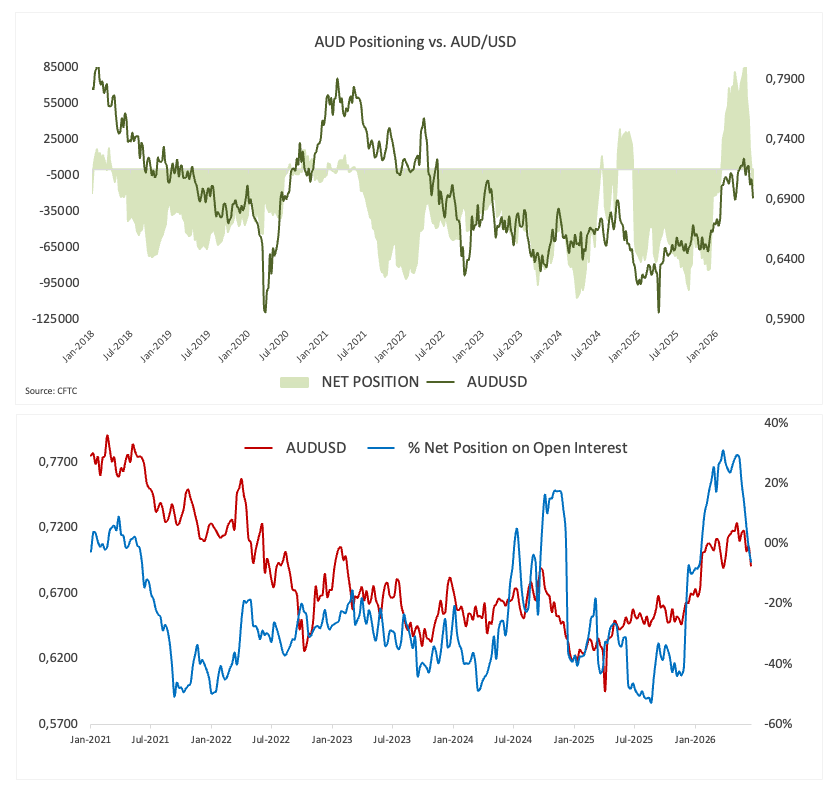

Speculative traders continued to unwind their positioning in the Australian Dollar in the week to June 23, with net positioning dropping to -13.0K contracts from -4.1K a week earlier. The move marks a second consecutive week in net short territory and extends the sharp reversal that has unfolded since speculative longs peaked earlier this year.

The latest Commodity Futures Trading Commission (CFTC) figures suggest the dominant theme remains the steady erosion of bullish conviction rather than the emergence of an aggressive bearish consensus. Net positioning declined by another 8.9K contracts on the week, while the 4-week change now stands at -73.2K contracts, underlining the speed with which investors have reduced their exposure.

Open interest tells an equally important story: outstanding contracts fell sharply to 214.3K from 295.5K, pointing to investors leaving the market instead of adding fresh short positions. That combination of weaker positioning and declining participation continues to favour the interpretation of long liquidation rather than outright bearish positioning.

Viewed in isolation, the return to net short territory could be interpreted as a decisive shift in sentiment. However, historical positioning measures paint a more balanced picture. Indeed, despite the recent sell-off, the current net position still ranks in the 79th percentile of its 5-year range, while the speculative exposure remains in the 80th percentile.

That apparent contradiction reflects the exceptionally elevated starting point. Non-commercial accounts have unwound a substantial portion of their long exposure over the past month, but positioning has yet to move into historically depressed territory. In other words, the market has become considerably less optimistic on the Aussie, but it is not yet heavily positioned for further downside.

From a positioning perspective, this remains a market in transition. Momentum continues to deteriorate, but the adjustment appears to be driven more by investors abandoning previously crowded longs than by the conviction that the currency is entering a sustained bearish phase. Until historical positioning metrics move closer to the lower end of their 5-year range, the data suggest there is still scope for further repositioning should the macro backdrop remain unfavourable.

What could drive the next move?

In the near term, the US Dollar, global risk sentiment, and geopolitics remain the main focus. Those remain the key drivers of price action. Next on tap on the Australian docket is the publication of the RBA Minutes of the June 16 meeting.

Key risks include a sharper slowdown in China, a persistently cautious Fed, a change in investors' risk sentiment, or any shift in the RBA’s stance. Any of these could quickly destabilise the Australian currency in the near term.

Technical view

In the daily chart, AUD/USD trades at 0.6889, extending its slide below the 55-day and 100-day simple moving averages (SMAs) at 0.7118 and 0.7080, which now cap the topside and reinforce a bearish near-term bias. Price still holds marginally above the 200-day SMA at 0.6861, but the Relative Strength Index (14) around 27 signals oversold conditions, while the firm Average Directional Index (14) near 40 suggests the downtrend remains strong despite stretched momentum.

On the downside, initial support is seen at the 200-day SMA at 0.6861, followed by the horizontal level at 0.6833, ahead of more substantial cushions at 0.6660 and 0.6593, where sellers could slow the decline. On the topside, immediate resistance emerges at 0.7079 and the nearby 100-day SMA at 0.7080, with the 55-day SMA at 0.7118 adding to this supply zone, while higher up, 0.7278/0.7283 precede a more distant barrier at 0.7661.

(The technical analysis of this story was written with the help of an AI tool.)

All in all

The broader backdrop for the Australian Dollar remains constructive, albeit losing some momentum. In the meantime, the RBA’s cautious stance should continue to provide some degree of support on dips.

But the Australian Dollar is still a currency that trades heavily on sentiment. When confidence is strong, the Aussie performs well. When uncertainty creeps in, the Greenback tends to take over.

So while the medium-term story still leans constructive, the near-term outlook feels less certain. The move higher should be there, but conviction is not quite there…yet.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.