Stuck in the mud but no hard landing yet

The global macroeconomic backdrop has weakened significantly since we published "The Big Picture – Renewed trade dispute casts shadow over global economy" on 11 June, following the escalation of the trade war between China and the US. In this document, we present our updated economic outlook for the US, China, the eurozone, Germany, Japan and several emerging markets.

We see further downside for the global economy in coming months, followed by a stabilisation and modest rebound on the back of monetary and fiscal stimulus.

Our new base case of no solution to the trade war between China and the US ahead of the 2020 US presidential election has led us to downgrade our growth trajectory for

both advanced and emerging markets.

The risk of a more pronounced downturn has increased (we assume 30% probability of a recession in the next two years). However, in our view, there is also possible upside

from a sudden breakthrough in US-China trade negotiations, more aggressive central bank easing and still strong consumer confidence.

Overview

This document updates our global economic outlook and discusses the downside and upside scenarios from our baseline. The global macroeconomic and political backdrop has weakened significantly since we published The Big Picture – Renewed trade dispute casts shadow over global economy on 11 June. Some of the downside risks that we flagged have materialised, most notably the decision by Donald Trump’s administration in late July to escalate the trade war with China, further after signalling an intention to hit the remaining USD300bn of imports from China with 10% tariffs. On the back of the announcement in late July, global risk sentiment dived further and global bond yields fell to new lows.

In light of the escalation of the trade war and the severe negative impact it has had on the relations between the two countries, we no longer expect a deal between the two sides ahead of the 2020 US presidential elections in our baseline (we assume 60% probability of no deal). However, we do not preclude the two sides from delivering a sudden breakthrough, seeing a 40% probability of a trade deal (for more discussion on the scenarios, see US-China Trade – Three trade war scenarios – 'no-deal' now our baseline, 8 August).

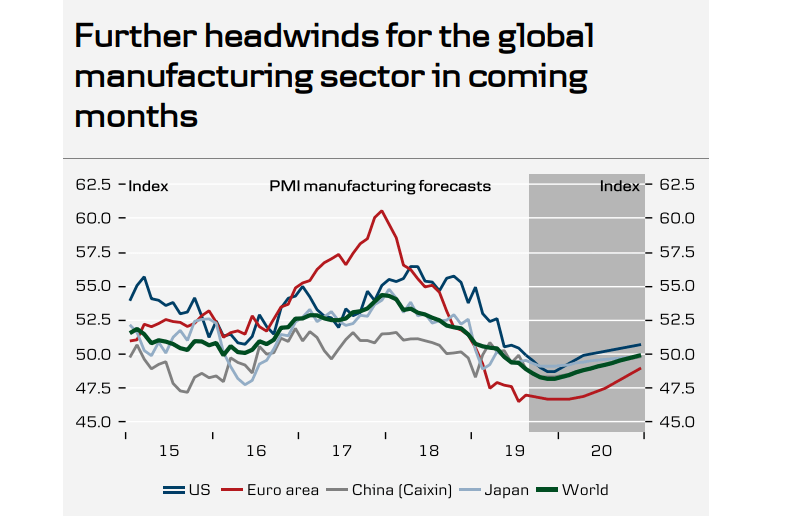

The absence of a trade agreement between the two sides in the near future and a cautious easing policy by the central banks are set to weaken the momentum in the global economy near term. The biggest impact of the trade war is the uncertainty about global value chains and the future state of the global economy, which is hurting investment demand, global trade and manufacturing activity. As a result, we see further downside for the global manufacturing sector in coming quarters; in other words, we believe the global economy is stuck in the mud for the time being. However, the service sector has held up well.

In response to the weakened outlook for the global economy and sharp falls in inflation expectations, we expect the Fed, in particular, and other central banks to ease monetary policy quite vigilantly. The Fed already cut its policy rate in July and the ECB has opened the door to easing at the next meeting in September. We now expect the Fed to cut its policy rate a total of five additional times (see FOMC Research – New Fed call: five more from Fed, 15 August), while we think the ECB will cut

rates by 20bp (see ECB Research - New ECB call - rate cut and restart of QE, 18 June), restart QE and introduce a tiering system (see ECB – Mitigating side effects – gauging the tiering premium, 16 August). Many emerging markets’ central banks, including the Brazilian, Russian, Indian and Indonesian central banks, have already followed suit with monetary easing. We believe the monetary policy easing in both advanced and emerging markets will support domestic demand in their economies.

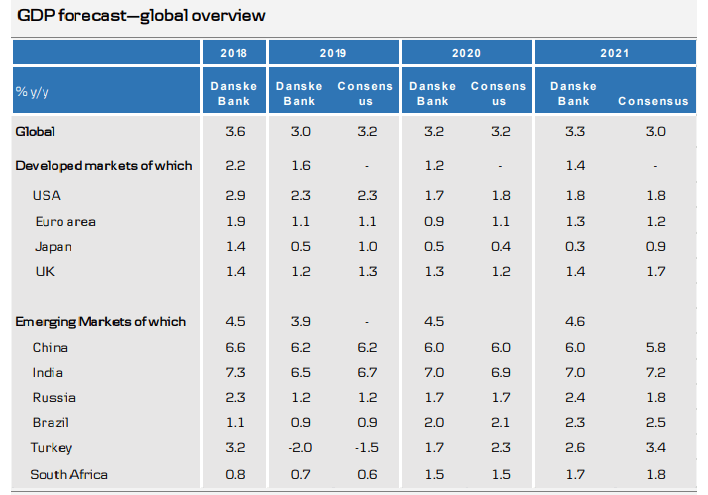

On aggregate, we downgrade the outlook for the global economy in coming years. We lower our growth outlook, expecting global growth to be 3% in 2019, followed by a slight pickup to 3.2% in 2020 and 3.3% in 2021 (versus 3.2% in 2019 and 3.4% in both 2020 and 2021 in The Big Picture – Renewed trade dispute casts shadow over global economy on 11 June). Following weakness in coming months, we expect the global economy to stabilise early in 2020 and witness a modest recovery onwards, as the stimulus measures from the global central bank and fiscal easing in China start to kick in.

While our baseline assumes modest growth in the global economy, the risk of a more pronounced downturn is increasing. Among the key downside risks are further escalation of the trade war between US and China, possible US car tariffs versus Europe, a hard Brexit this autumn or too slow and small stimulus by the global central banks. Furthermore, another key risk is a negative spiral in confidence and actual spending in the global economy set forth by the current negative headlines. In our view, the risk of the downturn resulting in a global recession is around 30% over the next 18 months.

While there are currently many negative headlines, there are also upside risks (see positive scenario). The US and China could find an agreement in the trade dispute, which would underpin market sentiment by removing uncertainty and supporting a pickup in investment and global trade. Consumer sentiment remains strong. There are few noticeable imbalances in the biggest economies, which normally precedes a recession. Inflation pressures are still modest allowing central banks to extend stimulus rather than stepping on the brakes, keeping easy financial conditions with the potential to support global demand.

In our view, three factors are critical to the economic outlook for the global economy over the next three to six months: (1) monetary and fiscal stimulus in advanced and

emerging markets, (2) trade discussions between China and the US and (3) Brexit negotiations. In the table below, we outline some of the key dates for each risk factor for

which to watch out.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.