Remember: Powell doesn’t retire until May

Outlook

Trump announced Kevin Warsh will be his nominee to replace Fed chair Powell. Having already served at the Fed, Senate confirmation is presumed to be a snap. Warsh is qualified but considered a Trump vassal. He will, of course, tell the Senate that he believes in Fed independence, just as the Supreme Court nominees swore they would abide by Roe—in other words, go on to find a way to break his word.

As both an economist and lawyer, tapdancing around that issue will be easy.

The obvious implication is that the Fed will be more dovish, but remember, Powell doesn’t retire until May. The CME FedWatch puts the probability of a June rate cut at 48.5%, not materially changed over the past few weeks, with another 16.9% expecting more. We shall see if this rises in the coming days.

As a general rule, the idea of a Fed on the rate-cutting trajectory “should” be equity-favorable and dollar-unfavorable. We are seeing only a little of that so far, perhaps because even the Fed chair has only one vote of the 12. But Warsh has some ideas about re-configuring Fed thinking and for all we know, that may be welcome.

Upcoming data will be useful. Today we get Dec PPI, forecast to 2.8% from 2.9% and core down from 3% to 2.8%. Remember, PPI feeds less into CPI than elsewhere Next week it’s JOLTs and Jan non-farm payrolls. So far nobody is forecasting a worsening of labor market conditions.

Japan

Either we got it wrong or Japan is putting on a brave face. Japan is positioning itself as not betrayed by TresaSec Bessent saying the US was not intervening in the dollar/yen. Technically, this is true—no one has actually spent a dime. Bessent did not deny he had ordered the NY Fed to “check prices,” an escape hatch for him. Japan can credibly go on projecting the US is with it if real intervention takes place.

This is the Reuters take: “Japan's top monetary officials are leveraging rare U.S. backing in their fight against the weak yen, using tactical silence and calibrated communication to drive the currency sharply higher without resorting to large-scale intervention.”

Top currency diplomat Mimura (vice finance minister for international affairs) is deliberately keeping traders guessing, as is the norm. He does it well and is admired in Japan. “"They've pushed dollar/yen down by roughly seven yen while preserving their firepower," said Shota Ryu, FX strategist at Mitsubishi UFJ Morgan Stanley Securities. "It's a remarkably efficient approach."

In Japan, the checking rates story is enough for the Japanese. “Its involvement, even at the level of rate checks, has strengthened the perception that the two governments are aligned in catching the yen's declines.”

Being silent is also communication, Mimura said. “Bank of Japan money market data shows no clear signs of Japan having conducted interventions since Friday's yen rally, at least not at the scale of operations in 2022 and 2024, when Japan spent 24.5 trillion yen ($160.19 billion) in total.”

Meanwhile, BoJ chief Ueda is doing the same thing—keeping mum about rate intentions. Besides, the two rate hikes forecast for later this year will not be market-moving. Then there is the Feb 8 election. Takaichi is turning out to be surprisingly popular.

So, wither the dollar/yen? If past is prelude, traders will test the supposed bond by taking it back towards 160, if skittishly and turning tail at various critical points. The 50% retracement of the downmove is 155.69 and the 62%, 1.5652. The B band lies at 157.41 and the old support/new resistance at 158.46.

Forecast

Sentiment is losing one of its top factors—relative interest rate decisions by central banks. The ECB is on hold, the US will be cutting and only the Reserve Bank of Australia is expected to hike. If these expectations are baked in, it will be other factors driving FX. That doesn’t mean inflation is off the table, the underbelly of central bank decisions, but something else will likely rise to the top of the list. In recent years it has been PMI’s, although they have lost some muscle as precursors for growth.

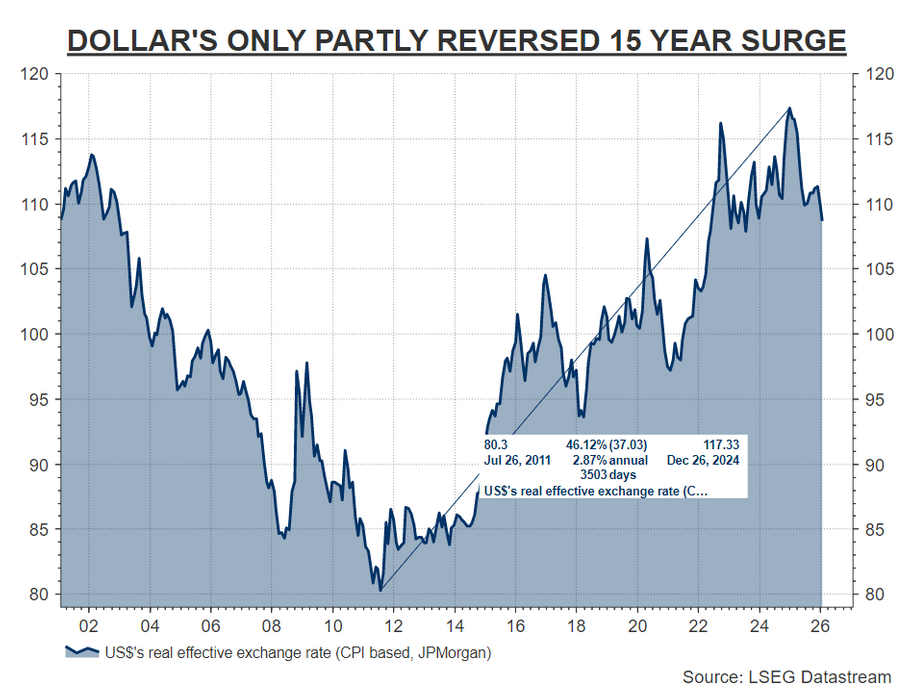

Charts matter and may matter more in the coming months. After all, the Dollar gained some 50% over the last decade and has given back only about 10% of it. We had endless (annoying) stories about king dollar. Now that the US has shown itself to be untrustworthy under Trump, it has a long way down to go. That’s the general picture. Unfortunately, it will be punctuated by upswings that will be due more to big player positioning than to economic data.

US politics

The liberals go on and on about Trump in full retreat over the conduct of the Feds in Minneapolis, with his border czar claiming repeatedly it is withdrawal of officers but Trump saying the opposite. A government shutdown was avoided by Congress agreeing to a new spending bill that excludes big increases for ICE. Trump and minions continue on lawlessly.

Food for thought

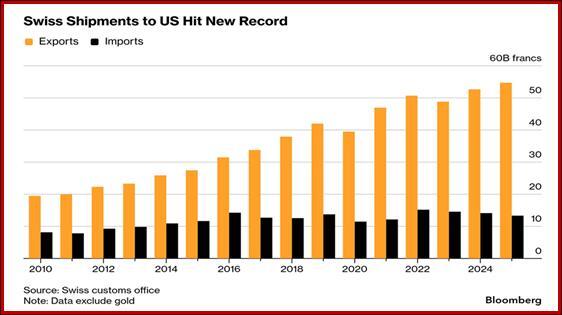

Maybe tariffs don’t matter. Exporters to the US can find other buyers or have the wherewithal to eat the tariffs. Yesterday Bloomberg had a dandy story on Switzerland overcoming tariffs and doing just fine, thank you. See the chart.

Between Aug and November, Trump imposed a 39% tariff on Swiss exports to the US because the Swiss leader, a lady, “rubbed me the wrong way.” (To be fair, a Swiss person will tell you Switzerland is the best country in the world within the first 15 minutes of meeting. It’s off-putting at first until you get used to it, like the guy who always mentions he went to Harvard B School within the first 15 minutes.)

In the Swiss case, the new tariff deal, still pending, will be 15% in exchange for “$200 billion in investment pledges by Swiss companies, easier market access for American fish, seafood and nuts, as well as duty-free quotas for certain meats.”

Bloomberg goes on to point out the US takes 20% of Swiss exports, making it the top buyer. Watches suffered during the higher tariff period, but pharma and chemicals are bigger. “Swiss watch exports to the US soared by more than 19% in December as brands rushed to send inventory to America.”

But trade isn’t all. There’s also those investment promises extorted from trade partners—Taiwan, S. Korea, Europe, Japan. We haven’t added up the billions but it’s huge. Here’s the rub—the timeframe for delivery of the actual plans and the money extends out several years. This is a practical necessity, but it should be obvious that the countries are counting on the next president to pardon them from any such obligation. Meanwhile, the companies that are supposed to make these investments have a great bargaining chip with their governments that put them on the spot. Lower taxes, probably.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)