RBA leaves rate unchanged, global equity rally continues

Market Brief

After a very volatile session on Monday, crude oil prices stabilized during the Asian session as Saudi Arabia and Russia said they would not commit to an output freeze but pledged to pull in the same direction to stabilize crude oil markets. After surging 8.20% since last Thursday, the West Texas Intermediate eased slightly to $45.30 barrel. The international gauge, the Brent crude, moved in a similar fashion, as it eased to $48 a barrel after hitting $49.35 yesterday in London. The market is now awaiting the International Energy Forum (IEF) in Algiers on September 26-28 as OPEC members are expected to hold informal talks. However, investors do not expected much of these talks as anyone among OPEC and non-OPEC members seemed ready to limit its own production.

In Switzerland, the GDP grew 2%y/y in the second quarter, beating wildly median forecast of 0.8%, while previous reading was upwardly revised to 1.1%. The upward surprise was mostly due to a sharp increase in government spending (+1.8%q/q versus +0.4% in the first quarter) and a boost in foreign trade with exports rising 6.5%q/q and imports falling 2%. CHF crosses did not react to the release with EUR/CHF trading sideways at around 1.0930 and USD/CHF holding ground at around 0.98.

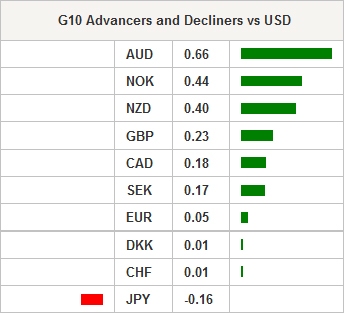

Overnight, the Australian dollar was the best performer amongst the G10 complex as it 0.63% against the USD, 0.89% against the EUR and 0.44% against the pound sterling as the chase for yields continues and the central bank decided to leave rate unchanged after a cut in early August. AUD/USD hit 0.7637 in Sydney, rising 1.95% over the last week, as expectations for a September tightening move from the Federal Reserve fade away.

Asian regional market were trading in positive territory across the board with the exception of Australian shares which fell 0.30%. In Japan, the Nikkei and Topix indices were up 0.26% and 0.65% respectively. In mainland China, the Shanghai and Shenzhen Composites rose 0.42% and 1.18% respectively, while offshore Hong Kong’s Hang Seng surged 0.39%. Finally, in Europe, equity futures followed the positive lead from Asia and extended gains in pre-session, pointing to a higher open.

Today traders will be watching CPI from Switzerland; retail PMIs from the euro zone and Germany; GDP from the euro zone; COPOM monetary policy minutes from Brazil; ISM non-manufacturing from the US.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 17081.98 | 0.26 |

| Hang Seng Index | 23742.77 | 0.39 |

| Shanghai Index | 3085.135 | 0.42 |

| FTSE futures | 6893.5 | 0.12 |

| DAX futures | 10709.5 | 0.29 |

| SMI Futures | 8323 | 0.18 |

| S&P future | 2180.1 | 0.1 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1327.25 | -0.02 |

| Silver | 19.54 | 0.14 |

| VIX | 11.98 | -11.13 |

| Crude wti | 45.38 | 2.12 |

| USD Index | 95.74 | -0.11 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| SZ Aug CPI MoM | -0,10% | -0,40% | CHF/07:15 |

| SZ Aug CPI YoY | -0,10% | -0,20% | CHF/07:15 |

| SZ Aug CPI EU Harmonized MoM | -0,10% | -0,10% | CHF/07:15 |

| SZ Aug CPI EU Harmonized YoY | 0,00% | -0,50% | CHF/07:15 |

| GE Aug Markit Germany Construction PMI | - | 51,6 | EUR/07:30 |

| GE Aug Markit Germany Retail PMI | - | 52 | EUR/08:10 |

| EC Aug Markit Eurozone Retail PMI | - | 48,9 | EUR/08:10 |

| FR Aug Markit France Retail PMI | - | 51,6 | EUR/08:10 |

| IT Aug Markit Italy Retail PMI | - | 40,3 | EUR/08:10 |

| EC 2Q F GDP SA QoQ | 0,30% | 0,30% | EUR/09:00 |

| EC 2Q F GDP SA YoY | 1,60% | 1,60% | EUR/09:00 |

| EC 2Q Gross Fix Cap QoQ | -0,10% | 0,80% | EUR/09:00 |

| EC 2Q Govt Expend QoQ | 0,20% | 0,40% | EUR/09:00 |

| EC 2Q Household Cons QoQ | 0,30% | 0,60% | EUR/09:00 |

| SA 2Q GDP Annualized QoQ | 2,60% | -1,20% | ZAR/09:30 |

| SA 2Q GDP YoY | 0,60% | -0,20% | ZAR/09:30 |

| UK BOE Indexed Long-Term Repo Operation Results | - | - | GBP/09:40 |

| BZ COPOM Monetary Policy Meeting Minutes | - | - | BRL/11:30 |

| TU Aug Effective Exchange Rate | - | 101,1 | TRY/11:30 |

| RU Bank of Russia Governor Nabiullina at Council Federation | - | - | RUB/12:00 |

| UK Bank of England Bond-Buying Operation Results | - | - | GBP/13:50 |

| CA sept..02 Bloomberg Nanos Confidence | - | 59,3 | CAD/14:00 |

| US Aug Labor Market Conditions Index Change | - | 1 | USD/14:00 |

| US Aug ISM Non-Manf. Composite | 55 | 55,5 | USD/14:00 |

| US Sep IBD/TIPP Economic Optimism | 48,1 | 48,4 | USD/14:00 |

| BZ Aug Vehicle Production Anfavea | - | 189907 | BRL/14:20 |

| BZ Aug Vehicle Sales Anfavea | - | 181408 | BRL/14:20 |

| BZ Aug Vehicle Exports Anfavea | - | 45552 | BRL/14:20 |

| SZ Swiss National Bank President Jordan Speaks in Lucerne | - | - | CHF/16:15 |

| BZ Jul Federal Debt Total | - | 2959b | BRL/22:00 |

Currency Tech

EURUSD

R 2: 1.1616

R 1: 1.1428

CURRENT: 1.1155

S 1: 1.1046

S 2: 1.0913

GBPUSD

R 2: 1.3534

R 1: 1.3372

CURRENT: 1.3341

S 1: 1.2851

S 2: 1.2798

USDJPY

R 2: 107.90

R 1: 105.63

CURRENT: 103.45

S 1: 99.02

S 2: 96.57

USDCHF

R 2: 1.0328

R 1: 0.9956

CURRENT: 0.9793

S 1: 0.9522

S 2: 0.9444

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

Author

Arnaud Masset

Swissquote Bank Ltd

Arnaud Masset is a Market Analyst at Swissquote Bank. He has a strong technical background and also works in the development of quantitative trading strategies.