One more hike from RBA in June?

Australia: Wage price index supports further RBA tightening

While Australian wage growth remains moderate by international standards, the latest print is still high enough for the Reserve Bank of Australia (RBA) to justify further tightening.

3.7% yoy wage price index

Higher than expected.

Wage growth is very lagging, but the RBA think it is important

The recent statements by Philip Lowe, the Governor of the Reserve Bank of Australia (RBA), have emphasized the significance of increasing wage rates and unit labour costs. Although I don't agree that these factors are alarming – as they tend to be lagging indicators of economic performance or residuals of slowed growth – it's evident that such data will likely influence the RBA's interest rate decisions in the upcoming months.

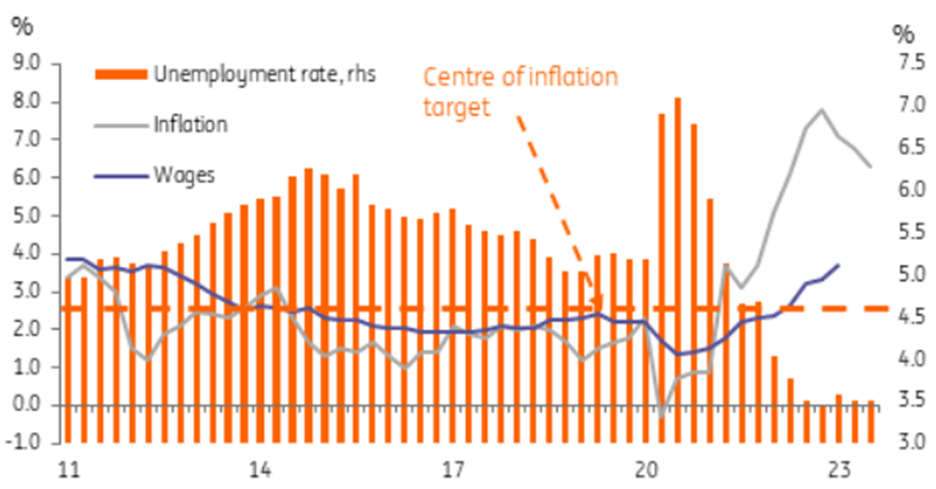

Australia's wage growth currently stands at 3.7%, which is relatively low compared to international standards. In the United States, hourly wages have grown by 4.4% YoY, and in the UK, weekly earnings (excluding bonuses) have risen by 6.8% YoY. This moderate wage growth in Australia does not appear particularly worrisome. Additionally, the quarterly increase has remained steady at 0.8% QoQ, showing no change from the previous quarter. However, from a purely mechanical standpoint, 3.7% is too high to align with the RBA's target inflation range of 2-3% (unless it undergoes moderation, which is likely to occur).

Australian wages, inflation, and unemployment

Source: CEIC, ING

Wage arithmetic

The basic calculation can be summarized as follows:

Assuming firms pass on wage growth in prices to maintain their profit margins and with an estimated 1% annual increase in productivity, they should be able to handle wage growth of up to 4% while keeping price increases below the upper limit of the 3% inflation target.

If we aim for the centre of the target range (2.5%), then the highest sustainable annual wage growth rate in the long run would be 3.5%. Therefore, the current wage price index growth rate of 3.7% YoY suggests a need for further tightening by the RBA.

However, there are several important considerations to keep in mind. One major factor is the assumption regarding how much of the wage growth can be absorbed by productivity. Governor Lowe often highlights low productivity growth, but productivity is influenced by economic growth, which is slowing, as well as the labour market, which has yet to show significant signs of softening but is likely to do so in time. Consequently, productivity is bound to experience cyclical declines during such periods, without any inflationary consequences.

Even prior to the current economic slowdown, Australia's trend productivity growth did not appear particularly impressive, with OECD estimates hovering near zero in the years just before the pandemic. If that is indeed the non-cyclical trend figure to consider, even modest wage growth, well below current levels, could start to squeeze profit margins and exert upward pressure on prices.

The truth is, we cannot be certain about these trends, and neither can the RBA. Trend rates only become evident long after the period of concern. What we do know is that regardless of productivity and wage growth, inflation is already decreasing. While the April figures may not show a significant decline, the following two months are expected to witness a more substantial drop in headline inflation.

Additional data on unemployment rates and employment growth will likely shape the RBA's decisions on interest rates soon. The unemployment rate remains exceptionally low, but the RBA is also cautious about the impacts of previous tightening measures. While today's data is important, the RBA does not appear to react impulsively on a month-to-month basis, making it challenging to assess their response pattern.

My current assessment suggests a probable 25 basis point rate hike in the cash rate target to 4.1%. This hike could potentially occur in June, although there is also an argument for the RBA to take their time and allow lagging data to reflect the effects of earlier tightening. Therefore, the timing of the rate hike remains uncertain.

While some market participants support the idea of two more rate hikes before reaching the peak, I believe that the resumption of the decline in inflation evident from May onwards will likely limit it to just one hike. However, the difference between these two perspectives is not significant.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

Author

ACY Securities Team

ACY Securities

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis. The key pi