Nonfarm Payroll preview: volatility coming, but no lasting effect expected

- The US is expected to have added 178K new jobs in May, unemployment rate seen steady at 3.9%.

- Wages' growth seen within latest levels, not enough to deviate the Fed from its gradual path.

Dollar's in correction mode ahead of the Nonfarm Payroll report but pulling back from multi-month highs against most of its major rivals. The previous sharp rally and the ongoing correction, have little to do with currencies' strength or weakness, but more to do with sentiment, and geopolitical jitters here and there.

The relevance of employment figures is tithed to upcoming central banks' decisions, not only in America. The other leg, is, of course, inflation. With that in mind, one should wonder how much influence the outcome of the report could have on Fed's future decisions. Of course, a result which diverges from market's expectations would trigger some immediate action across the FX board, but as it has been long since the NFP had has the ability to change a previous trend.

Ahead of the report, the ADP survey showed that the private sector added 178K new jobs in May, below market's expectations of 190K, but more relevant, April's figure was revised to 163K from a previous estimate of 204K which could result in a downward revision of the previous NFP headline of 164K.

According to analysts forecasts, the US is expected to have added 188K in the month, while the unemployment rate is seen steady at 3.9%. The lately more relevant wages' growth figures are expected to post modest upticks expected to have risen by 0.2% monthly basis, up from 0.1% previously, while the year-on-year number is forecasted at 2.7% from 2.6% in April. These numbers will fall short of being a shocker for the Federal Reserve, not good enough to increase chances of more rate hikes, neither too soft to make them step back.

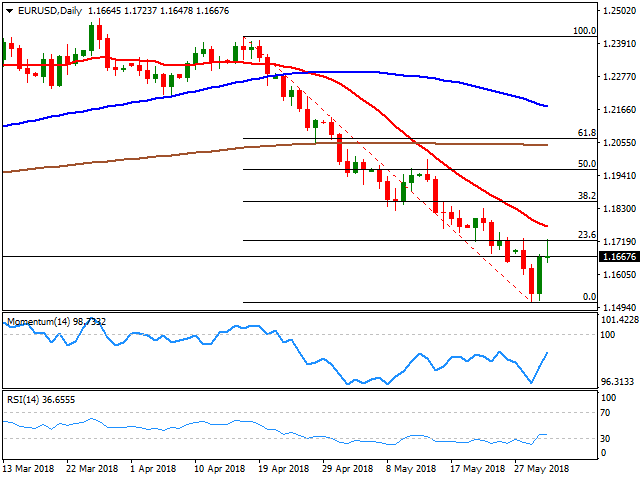

EUR/USD levels to watch

Ahead of the release, the EUR/USD pair reached 1.1720 but after failing to surpass its weekly high, came under renewed selling pressure, now around 1.1660. The daily chart shows that today's high coincides with the 23.6% retracement of the latest daily slump and that the overall bearish trend remains firmly in place, given that the 20 DMA continues heading lower above the current level and after crossing the larger ones, while the 100 DMA gains downward traction. Technical indicators in the mentioned chart have corrected extreme oversold conditions, but the RSI has turned flat, now around 36, indicating that the corrective movement may be over. The 1.1720/30 area is the key resistance for this Friday, as a discouraging report that boosts the pair through it, should anticipate further gains ahead extending into early next week. The 38.2% retracement of the same decline comes at 1.1850 but seems too far away to be a possible target for Friday. The 1.1600 figure is the main support, with a break below it exposing the recent yearly low at 1.1509.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.