Michigan Consumer Sentiment Index Preview: The tale of the shutdown

- First post-shutdown consumer confidence, current conditions and expectations readings

- Modest rebound expected from January's two year low

- Jobs, wages, GDP should support sentiment and expectations

The University of Michigan will release its preliminary Consumer Sentiment Index for February on Friday February 15th at 10:00 am EST, 15:00 GMT.

Forecast

The University of Michigan consumer sentiment index is predicted to rise to 93.0 from 91.2 in January. The current conditions index is expected move up to 112.1 in February from 108.8. The expectations measure will climb to 84.5 from 79.9 in January.

The government shutdown and the economy

The partial closure of the US Federal bureaucracy from December 22nd until January 25th had little effect on the labor market. Job creation jumped to 304,000 in January from 222,000 the previous month, private and manufacturing payrolls were abundant and annual wage gains stayed within a 0.1% of their decade high.

Initial jobless claims did rise to 253,000 in the last week of January as government workers reported. This was more than 30,000 over the 4-week moving average but they declined to 234,000 the following week and are expected to be 225,000 in the week of February 8th, which would be back at trend.

Statistics from other areas are still pending. Retail sales for December is due on Thursday and while the monthly expansion is predicted to be 0.2% and 0.4% for the GDP destined control group, sales numbers are notably volatile. Industrial production for January covering the shutdown month from the Federal Reserve is scheduled for Friday February 15th. While the anticipated increase of 0.1% would be down from December's 0.3% growth and Novembers 0.6% gain it would equal the rise in October. The reason for the drop would more likely be the severe cold weather in two-thirds of the country in January than any cutbacks by firms due to shutdown fears.

The US government shutdown and consumer sentiment

One area in which the partial government closure did appear to have a substantial impact was consumer sentiment.

The University of Michigan Consumer Sentiment Survey saw a post-recession peak of 102.00 in March 2018 and a subsequent top of 100.8 in September. After a modest and gradual decline to 99.0 in October, 98.3 in November and 97.5 in December, the gauge plunged to 91.2 (initially 90.7) in January, the survey coinciding with the first two full weeks of the partial shutdown. The initial 6.3 point drop was the largest one month decline in six years. This brought sentiment back to the level of late 2016 just before the US presidential election.

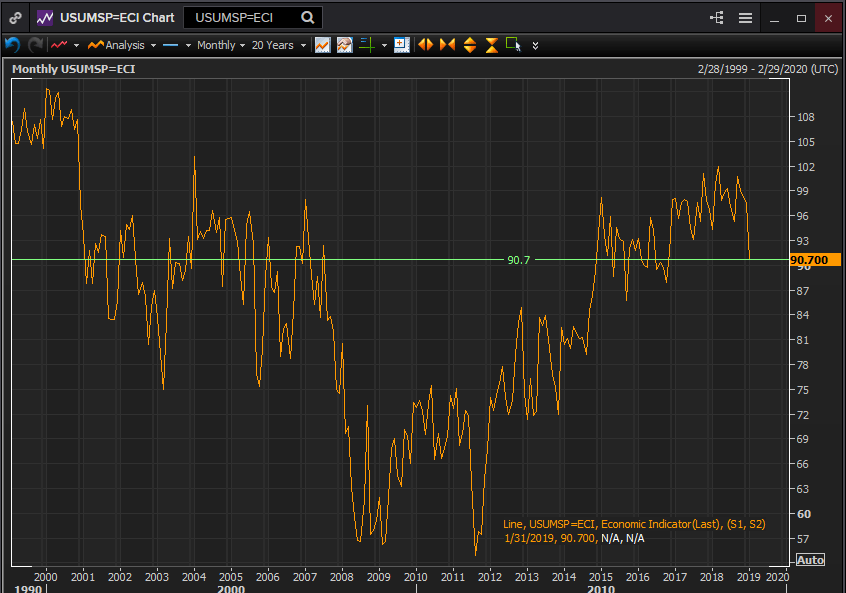

University of Michigan Consumer Sentiment

Reuters

The current conditions index evinced a similar though more volatile pattern. It hit a19 year high in March last year at 122.80, fell to 107.80 in August, rebounded to 115.20 by December and then dropped to 108.80 (initially 110.00) in January. The 6.4 point drop into January was smaller than the decline from March to April last year and the two month decline from June to August.

University of Michigan Current Conditions

Reuters

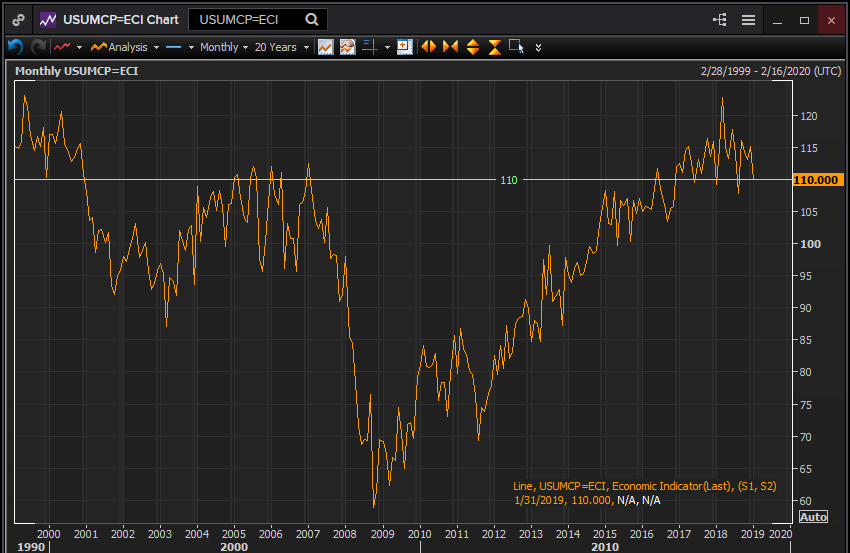

Consumer expectations sank in January along with its companion surveys losing 6.2 points from 86.1 to 79.9 (initially 78.3). Here also the comparison is to November 2016, and the post-election ascent.

University of Michigan Consumer Expectations

Reuters

Consumer Sentiment and the re-opened government

The February sentiment survey will be the first indicator that will test consumers' potential disillusionment with Washington. Each of the Michigan surveys dropped sharply in January, returning to the level of late 2016 before the two year surge of optimism brought about by the victory of Donald Trump.

Has the prolonged and often bitter political warfare in the capital begun to affect the attitudes of the American consumer? This is not an idle political question. Consumer spending comprises about 70% of US economic activity. With the labor market humming and wages and employment still rising there is reason to expect, but no certainty that households will resume their economy supporting outlook.

The next two months of sentiment data, February and March, will give an indication of if and how deeply DC politics may be damaging the economy.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.