Macro Events & News

FX News Today

European Fixed Income Outlook: German 10-year Bund yields jumped higher from the off and as of 06:19 GMT are up 1.8 bp at 0.326%, underperforming Treasuries and JGBs, which showed rates rising 1.6 bp and 1.0 bp respectively. Stronger than expected growth numbers at the start of the session added to pressure on Bunds, after core yields already started to back up again as stock markets stabilized and Turkey jitters receded somewhat. Japanese markets bounced back overnight and European stock futures are moving higher alongside US futures. Bundesbank’s Wuermeling suggested one should not “over dramatize” the risk of Turkey contagion, adding that ECB didn’t see the need for a risk meeting so far. Until there is a further dramatic escalation, the turbulence is not expected to derail ECB’s course towards a phasing out of QE. Already released German July HICP was confirmed at 2.1% y/y. Still to come are German ZEW confidence, the 2nd reading of Q2 Eurozone GDP and UK labour market data.

FX Update: Safe haven positioning were unwound some today, which saw the Dollar and Yen traded softer against most other currencies after Ankara managed to halt the rout of the Lira, which in turn brought a reprieve in still-fragile global markets. Most stock markets found a footing in Asia, and USA500 futures are showing a 0.3% gain, reversing most of yesterday’s regular-session’s losses, though Chinese market were an exception, declining after a batch of economic data showed the economy to have hit a rough patch, while investment growth was shown to have reached a record low. EURUSD settled around the 1.1400 mark, above yesterday’s 13-month low at 1.1365. USDJPY recouped back toward the 111.0 level after posting a seven-week low at 110.11 yesterday. PBoC set the reference rate for USDCNY at 6.8695, versus 6.8629 yesterday. China’s statistics bureau said that the weaker Yuan, which has declined the most against the Dollar since April on record (in the era of the prevailing regime), and perhaps aiming to counter the wrath of President Trump, was a reflection of the Fed’s tightening cycle. AUDUSD firmed above 0.7770, finding a footing after 3 consecutive days of declines. Australia data showing business confidence rising provided the Aussie a supporting influence.

Charts of the Day

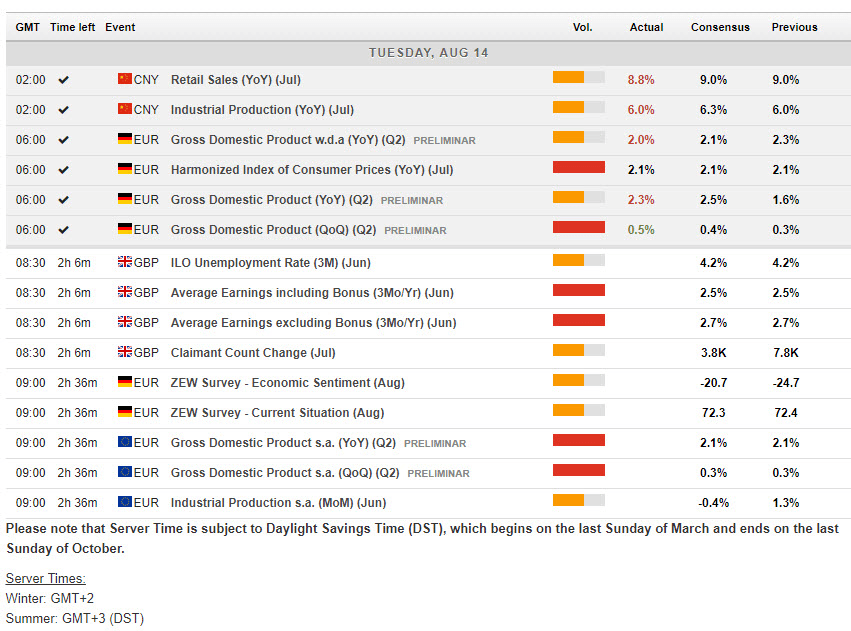

Main Macro Events Today

UK Average Earnings Index – Expectations – Average Household Earnings expected to come in with 2.5% y/y and 2.7% y/y growth in both the including- and ex-bonus figures, which would match the respective growth rates that were seen in the month prior.

UK Unemployment Rate – Expectations – The labour report expected to show unemployment holding unchanged at 4.2% in June.

Eurozone GDP – Expectations – Eurozone Q2 GDP is likely to be confirmed at 0.3% q/q.

German ZEW Economic Sentiment – Expectations – A slight improvement is anticipated in the headline number to -24.0, from -24.7 in the previous month.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in