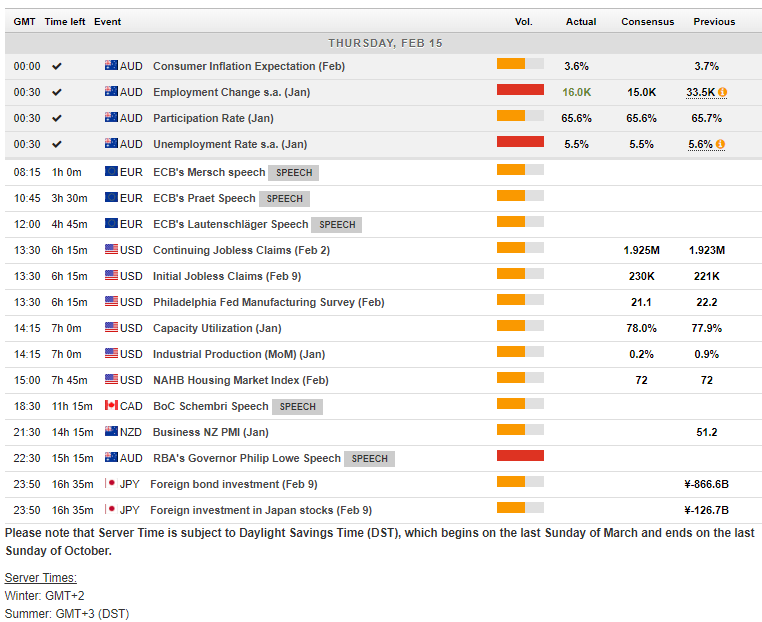

Macro Events & News

FX News Today

European Fixed Income Outlook: Asian stock markets moved broadly higher, after a strong close on Wall Street yesterday. Investors seem to get slowly used to the idea of further U.S. tightening and a trend higher in global yields, but set backs on the way are still likely. The Nikkei closed with a gain of 1.47%, despite a stronger yen. The ASX 200 gained 1.16% and Hang Seng and CSI 300 are up 1.97% and 0.80% respectively. Bund yields continue to rise in opening trade, peripherals are outperforming as risk appetite continues to improve and European stock futures move higher in tandem with U.S. futures, after a strong session in Asia and following on from yesterday’s gains. US and UK100 futures are moving up, suggesting that the recovery in stocks continues and oil prices are higher with the front end WTI future trading at USD 61.83 per barrel. Today’s European calendar is unlikely to shake things up significantly with Eurozone trade numbers for December the main highlight.

FX Update: The dollar has declined for a fourth-straight session versus the euro and other currencies. The narrow trade-weighted USD index (DXY) is presently at a two-week low of 88.80, showing a 0.3% decline on the day and now racking up a 1.8% loss on the week so far. EURUSD lifted to a two-week peak of 1.2487, and AUDUSD also posted a two-week high, while Cable logged a one-week high. USDJPY continued to lead the dollar lower, with the pair showing over a 0.6% loss on the day as the London interbank community take to their desks. This is despite the 10-year U.S. Treasury yield rising to four-year highs during the Asia session, which extended the move seen since yesterday’s hotter than expected U.S. CPI data. The revived risk appetite evident in global markets has been putting U.S. held assets out of favour as investors seek out higher yields, which is weighing on the greenback. With regard to USDJPY specifically, also in the mix were remarks by Japan’s finance minister, Aso, who said that recent yen strength was not sufficient to “require intervention.”

Charts of the Day

Main Macro Events Today

ECB’s Mersch, Praet and Lautenschlager Speech

US PPI – PPI is forecast to rise 0.3% in January, while core may increase 0.2%, though core y/y at 2.0% would be below 2.3% previously.

US Unemployment Claims – Initial jobless claims may rebound 9k to 230k for the week ended February 10.

US Philly Fed Manufacturing Index – may ease slightly to 20.0 in February vs 22.2 and the Empire State index is set to tick up to 18.0 in February vs 17.7.

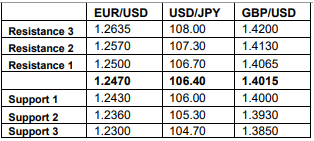

Support and Resistance levels

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in