Macro Events & News

FX News Today

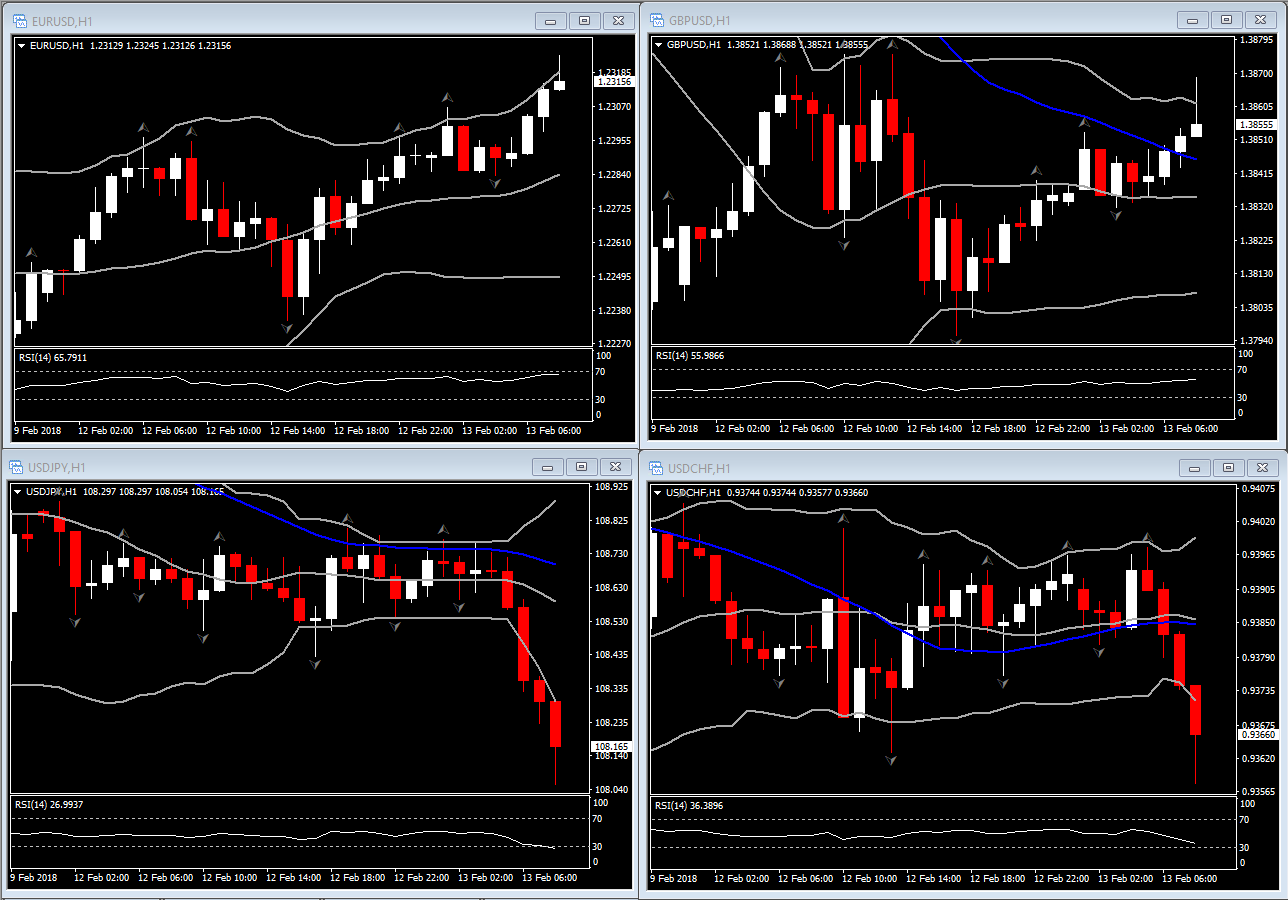

European Fixed Income Outlook: Asian stock markets mostly moved higher. Japanese markets returned from yesterday’s holiday’s in a good mood, but pared gains as the yen strengthened and Nikkei closed with a loss of -0.65%, the Topix was down -0.88%. In Europe, 10-year Bund yields are down -0.7 bp at 0.744% in opening trade, the 2-year is up 0.3 bp at -0.591%, leaving the curve flatter. 10-year Treasury yields are down -1.1 bp at 2.848% while JGBs underperformed in Asia and the 10-year nudged slightly higher despite a stronger yen. European stock futures are heading south, in tandem with U.S. futures setting up European equities for a correction from yesterday’s gains. Markets remain nervous as long yields continue to trend higher. The focus in Europe today will be on U.K. inflation data, with CPI expected to fall below 3% for the first time since August.

FX Update: The dollar traded mostly softer as the global equity rebound extended in Asia after Wall Street yesterday completed its biggest two-day rebound in just over two years. The U.S. currency has been correlating inversely with global stock market direction of late on the causation that risk-on phases have seen investors divest of dollars and dollar assets in favour of higher yielding opportunities, and vice versa. The narrow trade-weighted USD index has declined 0.3% to 89.94, earlier clocking a four-session low at 89.88. Cable and USDCAD have remained within their respective ranges from yesterday, while USDJPY and yen crosses have traded lower in Tokyo, where markets have reopened after a long weekend. Japan’s Nikkei 225 has bucked the global equity rebound, closing with a 0.8% loss, while U.S. equity index futures are also lower. AUDUSD saw a four-day high at 0.7874, aided by data showing Australian January business conditions rising to 19 from 13, with overall confidence lifting to a reading of 12, up from 11. The rand took a hit after the South African Congress ordered President Zuma to resign. News out of Japan today include remarks from Japan Economy Minister Motegi, who argued that Abe’s stance on monetary policy (i.e. ultra dovish) must be maintained. Japan January PPI came in at 0.3% m/m, as expected, after 2.7% y/y in the month prior.

Charts of the Day

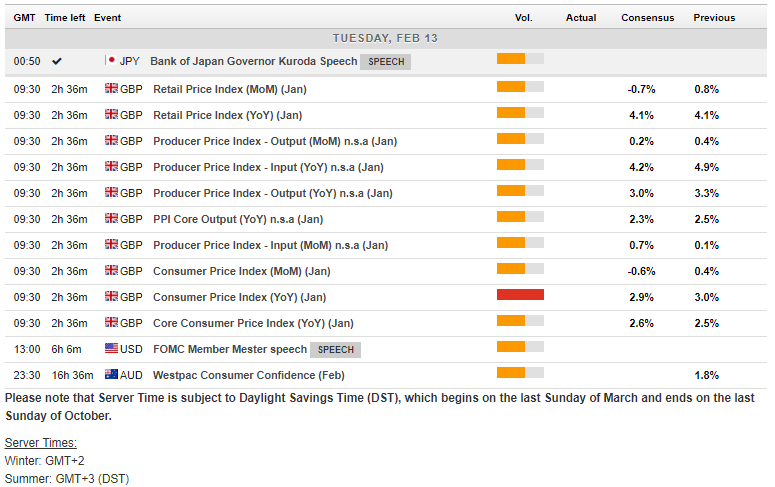

Main Macro Events Today

UK CPI – expected to dip to 2.9% y/y after 3.0% in December, which would continue a modest climb down from the 3.1% cycle peak that was seen in November. An as-expected outcome would comfortably fit BoE projections, with the central bank forecasting CPI to have retreated to 2.2% at the two-year forecasting horizon in Q1 2020.

UK PPI – PPI core Input expected to rise to 0.7% in January from 0.1% seen in December.

FOMC Member Mester Speech

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in