Labor market healthy enough for the Fed to hike rates

AFTER THE RELEASE

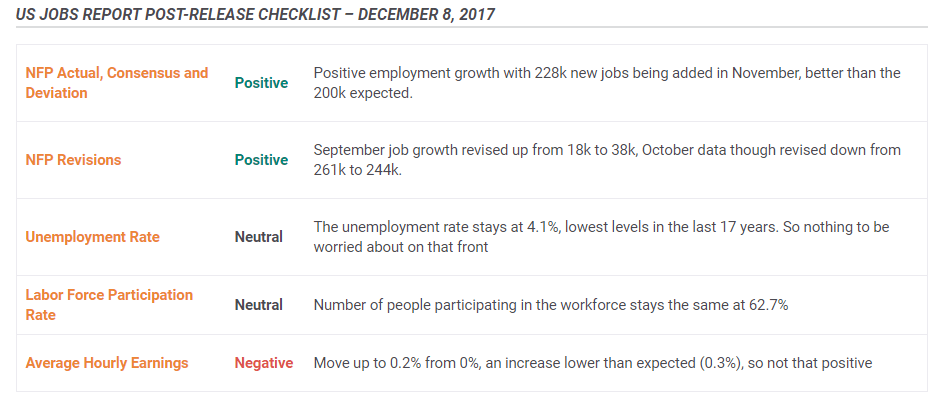

"...the headline number surprised positively, as the markets expected only 190,000 job gains in the previous month. Thus, the report is positive news for the U.S. labor market and negative for the gold market. Moreover, employment gains in September and October combined were 3,000 higher than previously reported. It means that job gains in the last three months have averaged 170,000, more than what is needed to keep up with the growth of population.

[...] Other labor market indicators were mixed. The unemployment rate was unchanged at 4.1 percent. Similarly, the labor force participation rate remained at 62.7. Meanwhile, the employment-population rate declined from 60.2 percent to 60.1 percent. It means that the U.S. economy added jobs, but neither unemployment rate, nor the labor force participation rate changed. It’s a bit strange. On the other hand, the average hourly earnings for all employees on private nonfarm payrolls rose by 5 cents. It means that the annual wage inflation was 2.5 percent. Historically speaking, the wage inflation is still subdued." by Arkadiusz Sieron

"At 228K job growth and 0.2% wage growth, the labor market is healthy enough for the central bank to move forward with 2017's last round of tightening. Although NFPs was one of this week's most anticipated economic releases, it had less of an impact on currencies than the Bank of Canada's rate decision and the Brexit deal." by Kathy Lien

"The EUR/USD price slightly rebounded after the important labor market report in the US. The unemployment rate remained at 4.1%, but the non-farm payrolls increased by 228,000 in November against the 198,000 forecasted and 244,000 in the previous month. Investors were disappointed by weaker than expected growth of the average hourly earnings by only 0.2% which is 0.1% less than anticipated." by OctaFx Analyst Team

"When compared to last year, the average monthly employment growth has reached 174K for eleven months of this year while averaging 187K in 2016. In terms of the labor market, a key element of the monetary policy, the year 2017 looks as good as 2016, justifying the expectations of three interest rate hikes going into the year 2018. " by Mario Blascak, PhD

"Now all the speculation centres on how this data may influence the Federal Reserve’s FOMC at next week’s meeting. It’s pretty much an odds-on certainty that the Fed will proceed with a 25 basis point rate hike on Wednesday." by David Morrison

BEFORE THE RELEASE

"Amid the NFPs’ release, we will also carefully consider the hourly wages growth which will likely provide any hints of inflationary pressures. Expectations are of an increase to 2.7 y/y from 2.4. This is also why we maintain our view that inflation is coming back up in the US and even though the Fed will raise rates next week, markets are still unsure about what will be the Fed monetary policy for 2018. Three rate hikes a year seem like difficult to achieve as pressures on all asset classes will not be sustainable. This may be one opportunity to buy back the euro against the dollar on the dip this afternoon." by Yann Quelenn

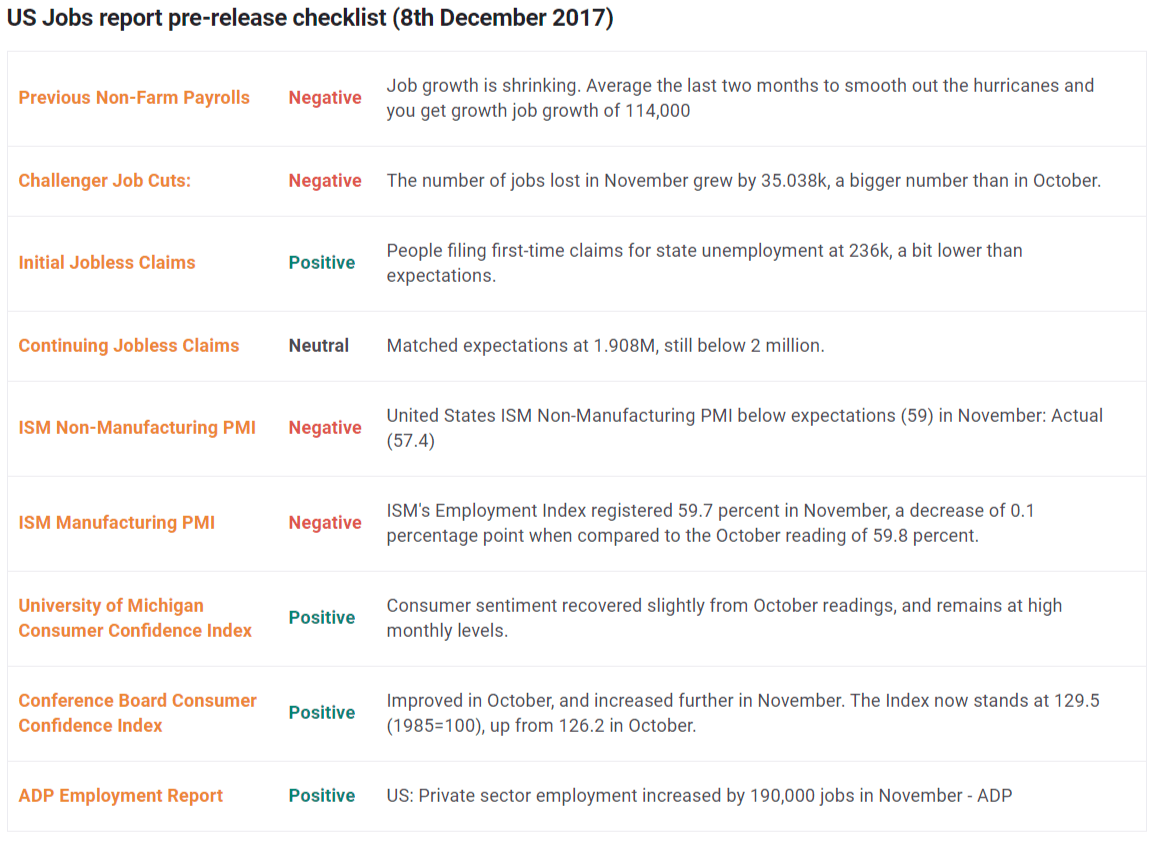

"Today’s NFP release has greater significance than usual as it comes less than a week before a key monetary policy meeting from the Federal Reserve. Next Wednesday the Fed is expected to raise rates by an additional 25 basis points to take its headline fed funds rate up to a band between 1.25 and 1.50%. If it does, then it take the fed funds rate to its highest level in over nine years.

[...]

The market assigns a 90% probability of the Fed hiking next week. Consequently, it’s unlikely that a poor payroll number would throw the central bank off track. However, a disappointing jobs report together with lower-than-expected Average Hourly Earnings (which would weigh on inflation) could see the Fed row back from its forecasts for a further three 25 basis point rate hikes throughout 2018.

[...] The consensus expectation is for November Non-Farm Payrolls to rise 198,000. This would represent a significant fall from the prior month’s reading of 261,000 which was itself well below the consensus forecast of a 312,000 increase. However, last month there were upward revisions to previous releases totalling 90,000 as the data counts were complicated by disruptions caused by summer hurricanes. Nevertheless, payrolls of 200,000 or thereabouts (revisions excepted) would keep the 6-month rolling average around 180,000 and should prove positive for equities and the dollar. Conversely, if payrolls come in below 180,00 and there’s no offsetting revision to prior data then we should expect the dollar to sell off – at least short-term." by David Morrison

"For the month of November, most economists forecast that around 210K non-farm jobs were created, so economists think that jobs growth was still relatively solid but slower compared October. In any case, just remember that a better-than-expected reading for non-farm payrolls triggers a quick Greenback rally as a knee-jerk reaction.Then the market could turn into profit-taking mode." by Kiana Danial, CFP

"From a technical standpoint, the Dollar Index has broken above 93.80 which could encourage a further appreciation towards 94.00. A solid NFP report has the ability to instil Dollar bulls with enough inspiration to challenge the 94.00 resistance, with the next level of interest at 94.20. Alternatively, a November NFP disappointment with subdued wage growth may open a path back to 93.50." by Lukman Otunuga

"While Friday’s jobs data outcome is unlikely to make very much of an impact, if any, on next week’s Fed decision (unless there is an exceptionally negative deviation from expectations), the current and ongoing employment landscape will be critical to the Fed’s policy path going forward into 2018, and will therefore impact the US dollar. Likewise, this impact on the dollar will also affect gold prices, which have dropped sharply in the run-up to the non-farm payrolls data, as the dollar has strengthened, anticipation of higher interest rates has increased, and demand for safe-haven assets like gold has generally remained subdued.

[...]

Wednesday’s ADP data came out essentially as expected at a very solid 190,000 private jobs added in November. Although the ADP report is not necessarily a very accurate pre-indicator of the official NFP jobs data from the US Labor Department – and sometimes even misses the mark dramatically – it does help provide a useful guideline when used in conjunction with other employment-related data.

One of the most important of these other indicators is the ISM non-manufacturing (services) PMI employment component, which showed expanding job growth in the critical services sector at 55.3 in November, albeit slower than October’s 57.5 reading. For the manufacturing sector, the ISM manufacturing PMI employment component also showed expanding job growth at 59.7 in November, which was little-changed from October’s 59.8 reading.Finally, November’s weekly jobless claims have all come out relatively close to expectations, and have mostly remained exceptionally low overall from a historic perspective." by James Chen

"The U.S. non-farm payrolls report is one of the most important pieces of data scheduled for release this week and it will play a major role in shaping expectations for Wednesday's Federal Reserve meeting. While the U.S. dollar traded higher against most of the major currencies today, its cautious rally over the past week particularly against the Japanese Yen is a sign of the market's lack of confidence in tomorrow's report. The Fed is widely expected to raise interest rates and the real question is where they go from there. Will Janet Yellen keep the Fed on a tightening track, hinting of further moves to come or will she take a step back and leave Powell with a clean slate? That's what investors will be thinking about after they see Friday's jobs report. Strong job growth accompanied by a solid increase in wages could go a long way in boosting expectations for 2018 tightening. Modest job growth accompanied by a subdued wage gains will keep investors skeptical of Yellen's intentions." by Kathy Lien

"The key, as usual, will be wages: average hourly earnings are forecast to rise 0.3% in the month, while compared to a year earlier, growth in hourly earnings is expected to accelerate to 2.7% in November from 2.4% the previous month. That won't be a shockingly positive reading, but surely an improvement from October's numbers." by Valeria Bednarik

"The previous NFP missed with 261k jobs added in October against expectations for more than 310k. This was the best month of jobs gains since July and the unemployment rate actually fell to 4.1% and the revisions to the prior two months means there is nothing in this to stop the Fed from hiking in December.

Nonfarm payrolls for employment for August was revised up from +169k to +208k, and the change for September was revised up from -33k to +18k , meaning employment was 90k higher than previously reported.

Of concern for the Fed is that wage growth has stalled and this raises doubts about the pace of inflation growth. Average hourly earnings rose 2.4% year on year, well down on the 2.9% reported last month and short of expectations for 2.7%." by Neil Wilson

"I’m expecting another buy rumors and sell fact effect with Average Hourly Earnings m/m below 0.3%. The sell-off of USD will be lasting until the FOMC meeting next Wednesday. On the contrary, we might have a huge rally in USD if the number beats expectation and USD will be bought continuously until next Wednesday as well." by Enho Kuo

Author

FXStreet Team

FXStreet