It's all lies part 2b: The money supply metrics have become obsolete

In Part 2a I spoke about how fiscal spending works and how misleading the money supply can be. You can also find Part 1 here if you haven’t read about how QE actually works– which is not money printing. Okay, time to fully pull back the curtain. The money supply metrics (M's) are not only misleading but have become obsolete. The reason being is that the M’s do not track the markets where the most dollars exist– repo and eurodollar markets – which is the non-M’s money I referred to in Part 2a. First, what are these markets? The repo market is the inter-bank wholesale funding market. This is the market that banks borrow and lend to each other on a day-to-day basis. Repo is short for repurchase agreement. In the repo market there are cash borrowers and cash lenders. If a bank (or any financial entity) is looking for funding, it can go into the repo market and post collateral (often a US Treasury) and another entity will lend them cash. If the borrower defaults, the lender can sell that collateral to recoup its losses. It is a repurchase agreement because when the borrower posts collateral, it is agreeing to ‘repurchase’ that collateral back at a later date (often the next day) plus interest. The interest charged on a repo loan is the repo rate, also known as the general collateral or GC rate. A repo transaction is seen from the perspective of the borrower. From the perspective of the cash lender, this transaction is called a reverse repo (RRP). Repo and reverse repo are simply two sides of the same transaction. Despite RRP being a hot topic recently because of the Fed’s engagement, we won’t get into it here because it does not fit the context.

The euro dollar market is a cashless, virtual dollar market that is the funding mechanism for the global banking system, and it governs our global monetary system. In simpler terms, the euro dollar market is an offshore, US dollar market. There are two dollar markets: onshore (US) and offshore (outside the US). Eurodollars simply refer to any US dollar that exists outside of the US. Prior to the euro currency, euro simply meant a currency held outside of the domestic economy. For instance, a euroyen are Japanese yen outside of Japan, euroyuan are Chinese yuan outside of China, etc. Just wanted to clear that up because those not familiar with eurodollars often think I mean the EUR/USD exchange rate, which has nothing to do with this. The euro dollar system is an unregulated market that the banking system completely controls (there is no Fed or US government authority in this market). The banks make the rules and create the dollars in whichever manner they see fit. These eurodollars are created through various and often complex balance sheet constructions, which often never show up on a transaction sheet or accounting balance sheet, and because of this, it is very difficult (near impossible) to keep track of (hence the reason it is called “shadow banking”). Assuming there is balance sheet capacity, global banks swap assets and liabilities (like we talked about in Part 1), creating eurodollars. I talked more about the eurodollar market and its importance in my article a few months back titled, The US Dollar Is Alive And Well.

Repo and eurodollars are what the M3 metric (mentioned in Part 2a) attempted to capture, however, the Fed no longer uses M3 and we’ll get into why in a moment. Both repo and eurodollars are ways that banks borrow and lend to each other. Aside from the eurodollar market being a strictly offshore dollar market, the biggest difference between it and repo, is that a repo loan is a secured loan (backed by collateral), whereas a eurodollar loan is an unsecured loan (not backed by collateral). In the repo market, you have two main types of transactions: tri-party repo and bilateral repo. In a tri-party repo transaction, there is a third party, known as a clearing bank that facilitates the settlement of the said transaction. They are an intermediary between the two parties in the repo transaction. Those third party clearing banks (often JP Morgan and Bank of New York Mellon) are required by the Fed to submit to them all the transactions that take place among them in the tri-party repo market. So, the Fed has a way of tracking some of the repo markets. However, most transactions are bilateral repo transactions – both collateral providers and cash lenders directly exchange with one another, no third party is needed. In a bilateral repo, there is no third party, and thus much harder to track. The eurodollar market is even less traceable because it is not only bank-to-bank transactions, but there is absolutely no government or central bank authority involved, and thus, no reporting of these transactions is required. Most of these eurodollar transactions happen “off” balance sheets, meaning they are never actually reported. But, how big are these markets? On average there is over $1T in repo transactions that take place every single day. Of course, this figure is likely a conservative estimate as most of the transactions in repo are never reported. The eurodollar market is estimated (depending on the study) to be $30T, $40T, or even $50T. In other words, it’s massive. I personally think the eurodollar market is even bigger than any estimate that’s out there. The truth is, no one really knows how big it is, we just know that it is extremely vast.

Now that there is a basic understanding of repo/eurodollars, let’s move on to perhaps what’s even more important than the M’s being misleading– how they became obsolete. In order to do that, we must go back in time. Before the eurodollar market came about in the 1950s, the money supply was much more straightforward. There were no eurodollars, repo had a very small role compared to today, there was no “shadow banking”, no derivatives being used (which we’ll touch on later), etc. And when the Fed needed to slow down an overheating economy or stimulate a slow economy, it manipulated the money supply and was able to do so more directly because of the gold standard. Rather, it created in-elasticity and elasticity. The former, could also be defined as scarcity or discipline– if the economy is overheating, make money more scarce, that is, make money tighter to slow down the economy. With the latter, it was about making money lose, by allowing for credit expansion in order to stimulate the economy. The Fed could sell gold or lower interest rates which could cause outflows of gold from the country. Less gold means tighter money conditions. On the other side, the Fed could look to attract inflows of gold, and one of the ways to do that was to raise interest rates. More gold means looser money conditions. Today, the Fed attempts to do this by adjusting the Federal Funds Rate, which has proven to be quite ineffective. Do they really think raising or lowering the overnight rate by 25 bps here and there is going to achieve desired results? Slow down a hot economy or boost a stagnant one? Mainstream economics (Keynesian’s) certainly believe that to be the case. The reason the raising or lowering of interest rates does not influence the money supply like it could under a gold standard is that the Fed is no longer in control of the money supply and does not know how to even define the money supply anymore, and they haven’t been able to for over 40 years.

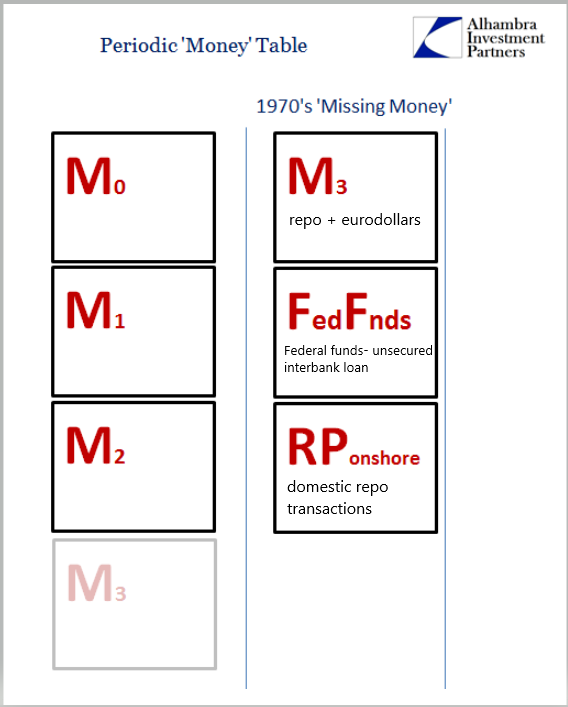

After WWII, the global economy was booming, which led to a global dollar shortage. It wasn’t so much that there wasn’t enough gold (although not distributed proportionately well), but rather the Fed was not able to create enough elasticity (credit expansion) to keep up with the booming economy. So, global banks that needed dollars found their own way to obtain them which did not include the Fed or US government – enter eurodollars. This was the purpose of eurodollars, to fill the void of the global dollar shortage that was being experienced. Unfortunately for the Fed, once this system got going, it never looked back. Jeff Snider of Alhambra Investments summarized what Charles Coombs (who at the time was the System Manager for the Open Market Account with the Fed) said in a 1974 FOMC transcript: “the volume of funds which might be shifted back and forth between that of the monetary statistics arose in connection with Euro-dollars; [Coombs] suspected that at least some part of the Euro-dollar-based money supply should be included in the U.S. money supply. More generally, he thought M1 was becoming increasingly obsolete as a monetary indicator. The Committee should be focusing more on M2, and it should be moving toward some new version of M3—especially because of the participation of nonbank thrift institutions in money transfer activities should be included in the U.S. money supply”. In other words, the progression of global banks’ usage of eurodollars in their transactions was happening so frequently that the Fed could no longer track or connect the money supply with what was happening in the real economy and should really be putting more focus on the eurodollar market. Let’s take a look at what money was beginning to look like up until that point. Courtesy of Alhambra Investments, below in the first picture is what money looked like prior to eurodollars and repo and the second picture is what money began to look like after eurodollars and repo. On the right hand side of the second picture is what the M’s are failing to capture, the “missing money”.

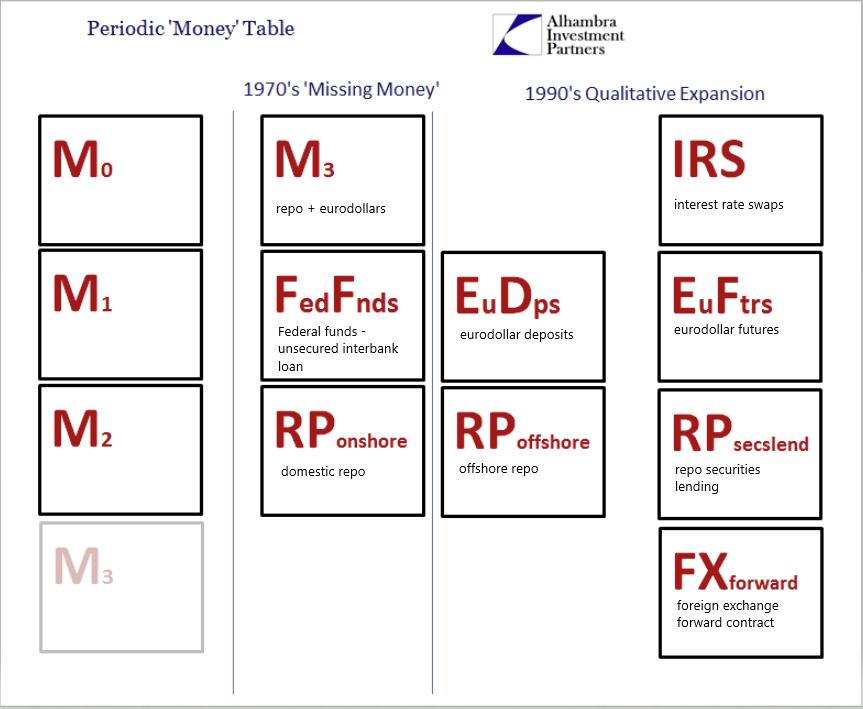

The Fed started to lose control of the money supply back in the 1970s, we’re talking almost 50 years ago. It did not get any better either (from the Fed’s perspective), in fact, it got worse, much worse. Fast forward to the 1990s and the products that were being used as money had grown significantly. Look at the chart below to see the expansion that had taken place which now includes derivatives. Had the Fed took the eurodollar market more seriously right off the bat, they might have been able to create a tool of measuring it. But they didn’t and the consequence was losing control of the money supply. Those that are only familiar with what the Fed’s mandate is now, might not see this as a big deal. Today, the Fed has a dual mandate: “The monetary policy goals of the Federal Reserve are to foster economic conditions that achieve both stable prices and maximum sustainable employment.” Price stability and maximum sustainable employment. Neither have anything to do with the money supply. But, they used to. The Fed’s mandate used to be about influencing the money supply, that is, up until the point in time that they realized they lost control of it. Now, the Fed has never openly admitted this or even announced that they were no longer going to target the money supply in their monetary policy. But, at some point in the 1980’s the Fed stopped targeting the money supply and started targeting the Federal Funds Rate instead. Now, like repo, Fed Funds is a wholesale inter-bank funding market, but it is not used anywhere near as much as repo is and yet, this is the Fed’s target. So, when you hear about the Fed lowering or raising interest rates, they are talking about Fed Funds, which has little influence on the overall money supply, especially when compared with repo and eurodollars.

However, in 2000, the Fed finally admitted (not directly of course) that they had lost control of the money supply. The following was said by then-Fed Chairman, Alan Greenspan in the June 2000 FOMC transcript: “The problem is that we cannot extract from our statistical database what is true money conceptually, either in the transactions mode or the store-of-value mode. One of the reasons, obviously, is that the proliferation of products has been so extraordinary that the true underlying mix of money in our money and near money data is continuously changing. As a consequence, while of necessity it must be the case at the end of the day that inflation has to be a monetary phenomenon, a decision to base policy on measures of money presupposes that we can locate money. And that has become an increasingly dubious proposition.” Basically, Greenspan is saying that the expansion of dollar products that exist outside of our money supply metrics had become so great that they had no idea how to track or even define what money was anymore. And, a decision for monetary policy to be based on money no longer worked because of it. At this point, not only was the Fed’s M1 and M2 completely useless in determining what money was, M3 hadn’t done much better. By 2006, the Fed discontinued its use of the M3 metric.

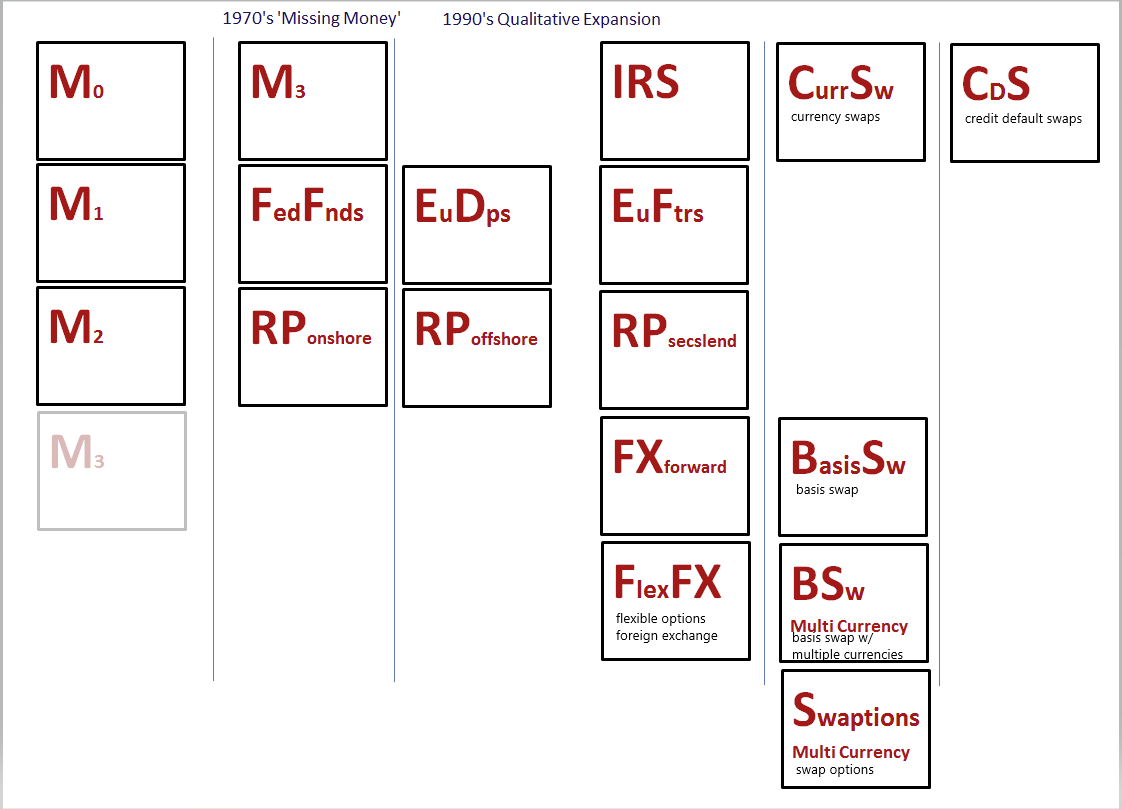

By the 2000s the “proliferation of products” had become even greater. The chart below depicts a further expansion of derivative products used in the repo and the offshore market to create eurodollars. I think at this point, it has become clear how obsolete the M’s have become because they fail to capture so many avenues where dollars are created and destroyed. To further prove this point, let’s take a look below at the M2 money metric alongside the CPI because Many academics like to say the definition of inflation is an increase in the money supply. Let’s start from about 1990 when the expansion of products became more rapid. The first half of the 1990s the M2 and CPI were mostly flat. Then from 1995 – 2000, the M2 grew, while the CPI mostly stayed flat, despite having bigger swings. From 2002 – 2008 the M2 declined, while the CPI rose and this was during the creation of the housing bubble! How could the money supply be declining during a time of economic expansion and housing market hysteria?! It doesn’t add up. Up until the GFC, money was loose and expanding but you would never know it by looking at the money supply metrics because money did not find its way into those limited avenues which they capture. The point I am trying to make is how are we supposed to predict the direction of inflation or growth based on the money supply if the money supply captures only a fraction of the money in existence? We can’t, and yet, it has become very popular since last year to use the M’s as proof that the Fed is printing money and that inflation is here to stay. By now, you should see the flaws in that argument. You can throw up the CPI and M’s on a chart and they may or may not line up. Like throwing darts at aboard. The eurodollar market is the largest dollar market in the world – more dollars are created and destroyed in this market than anywhere else. Add repo (a fraction of which the Fed tracks) on top of it, and it’s no wonder the Fed’s monetary policy no longer targets the money supply. If you want to know what is happening with money, you need to start looking in the shadows, not looking at the misleading, obsolete M’s, because they stopped tracking money many decades ago.

Now, after ripping the M’s apart in these past two articles, I do want to point out their usefulness. The M’s can serve a purpose, just not in determining the money supply, money creation, and money destruction. The M’s do track when money flows in and out of consumer bank accounts. We saw the M’s rise rapidly in 2020 as fiscal policy sent money directly into the checking accounts (captured by M1 and M2) of consumers and businesses. So, the M’s, when combined with things such as the velocity of money, can be useful in measuring where that money has flowed– whether it is spent in the real economy, used to purchase stocks, used to pay down debt, etc. This can give us a major clue into how successful fiscal policy has been and if consumer spending will help drive an economic recovery. I am not going to get into that here, nor will it be part of the ‘It’s All Lies’ series, but I will write about it in the near future.

Author

Ryan Miller

Ryan Miller Trading Economics

Ryan Miller received a Bachelors Degree in History from William Paterson University. Through his studies of U.S. history, he developed an interest in the implications the financial markets have on the economy.