It's all lies part 1: The Fed isn't printing money

Quantitative Easing (QE) has been used by the Fed (and other central banks) since the end of 2008, except for the Bank of Japan (BOJ) who has been using it since 2001. Yes, twenty years now. The Fed has many years of catch-up, which is exactly what they are doing with their rapid balance sheet expansion in the past year (see below). Unfortunately, this is not the way forward if economic growth is the ultimate goal. Japan, who is seven years ahead of the US in the QE department has been stuck in a vicious deflationary cycle. One which the US is headed towards. In other words, QE does not work. It has never worked and is never going to work. But, Ryan, “the money printer go brrrr!”. That is the most overused, inaccurate statement to describe what the Fed is doing. There is no printer. There is no money creation. But the Fed wants you to believe that there is. Let me explain. But before I do that, let’s first take a look at what QE actually does, or attempts to do.

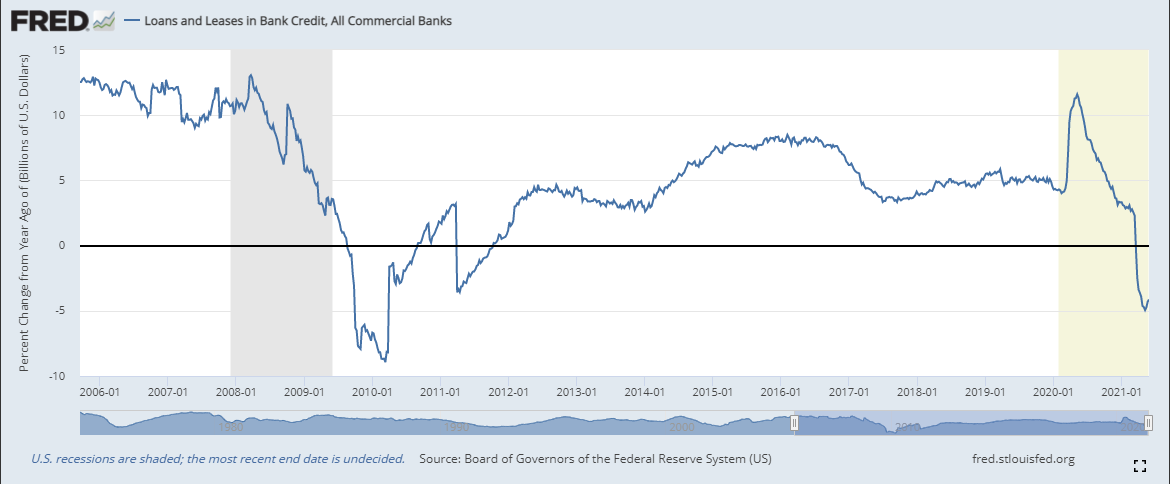

QE attempts to work through three channels: portfolio effects, signaling, and lowering interest rates. First, let’s look at portfolio effects. QE works by the Fed creating bank reserves and swapping them for US Treasuries with the Primary Dealers (big banks – more on this later). So, the Fed is removing a safe, liquid asset (US Treasuries) from bank balance sheets in hopes that the banks replace that asset with a riskier one – loans to consumers. That is the purpose of the asset swap (reserves for Treasuries), remove the safe asset to free up space for banks to then lend. When commercial banks loan money into existence, they increase the money supply (more detail on this later). The more money being created, the more likely it’s going to be spent into the real economy, boosting economic growth and inflation. This is the idea. Unfortunately, banks are unwilling to lend because they behave on a risk-adjusted basis and the current environment does not warrant risk-taking. If you look (below) I have a chart that show loans and leases of commercial banks since QE started back in 2008. Notice the big spike in lending just after March 2020 was due to the government guaranteed loans. The only reason banks were willing to lend was because the loans were guaranteed by the government, so it removed the default risk from the equation. Since, loans and leases have consistently contracted on a month-over-month basis. More bluntly, the portfolio effects channel has not been a success for the Fed, because not only are banks not replacing Treasuries with riskier assets (not lending), they are going out and buying more Treasuries. Just in the past year, commercial banks alone have added about $375B in Treasuries to their balance sheets.

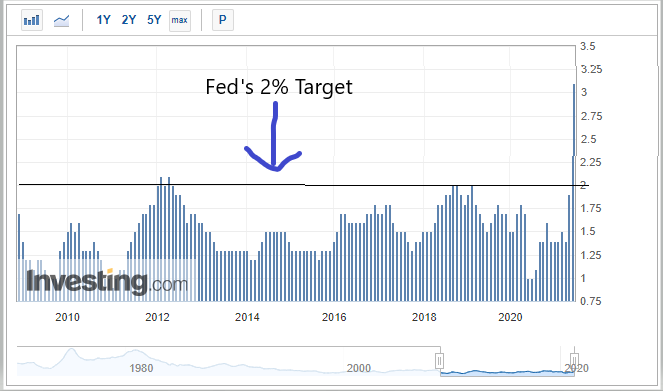

The next channel QE works through is signaling – attempting to control the behavior of consumers through what QE is believed to be, which is “money printing”. If consumers, businesses, etc. believe that the Fed is printing actual money and injecting it into the economy (which from a mainstream economic perspective should produce inflation), then they will behave in an inflationary way. They will start spending and investing – businesses will start spending and hiring etc. to front-run the inflation that is coming. If enough people behave this way, it can create inflation on its own, making it a self-fulfilling prophecy. This is the idea from the perspective of the Fed, set expectations and hope consumers and businesses act on them. This has probably been the most successful channel for the Fed, well, kind of. Now, this signaling never makes its way into the real economy. It has done a good job boosting financial assets (just look at the stock market since 2008), but it never translates into spending in the real economy (where it is most needed). Years 2009-2019 were the weakest growth period in history. On top of that, From January 2009 until April 2021, the Fed has failed to meet their PCE (personal consumption expenditure) inflation target of 2%, 138 out of 147 months (see below). Yes, they met their goal just 9 months during this time period. We can chalk this up as another failure.

The last channel is the lowering of interest rates. The mainstream and most people I come across believe that interest rates are low because the Fed has been buying bonds (QE) on and off since the end of 2008. It makes sense, because bond prices and yields have an inverse relationship. So, if the Fed is engaging in an LSAP (large scale asset purchases) by buying bonds, bond prices should rise and yields should fall. Since we know that interest rates are structured based on bond yields, they fall too. The purpose of lowering interest rates is to stimulate the economy because it lowers debt servicing costs and enables cheaper borrowing. On paper it all makes sense. The Fed buys bonds, pushing up bond prices and lowering yields (interest rates). Low interest rates are accommodative because it makes borrowing cheaper, which encourages consumer borrowing and spending in the real economy. It’s that simple. End of discussion. Except in practice, in the real world, it does not work anything like that. Low rates are not accommodative. Low rates are NOT a sign that money is loose and flowing. Low rates tell us that money is tight. Low rates cannot be stimulus if it means money is tight. This is the interest rate fallacy, famously brought to the mainstream’s attention by Milton Friedman back in the 1960s, yet economists continue to ignore this reality.

Okay, but the Fed is the reason the interest rates are low, right? They would certainly like you to think so, but there is little evidence to support this popularly held belief. This is a quote from a research paper conducted by the IMF (International Monetary Fund) in 2012: “Research on the effectiveness of earlier quantitative easing has yielded mixed results, with most pointing to limited effects on economic activity. While most papers found evidence that quantitative easing helped reduce yields, its effect on economic activity and inflation was found to be small. The reasons cited included a dysfunctional banking sector, which impaired the credit channel…”. So, according to this study, QE has at best, “helped reduce yields”. If it has only helped reduce yields, that means the market is the other party responsible for sending yields lower. But, who is more responsible for falling yields, the Fed or the market? “The evidence shows LSAP proved effective in providing much needed support, lowering long-term interest rates and exchange rates, and underpinning economic growth and inflation. Studies found the government bond purchases worth 10 percent of GDP have, on average, lowered 10-year government bond yields by around 50 basis points.” This is straight from the RBNZ’s (Royal Bank of New Zealand) website, which is one of the many central banks engaging in QE. Let’s think about the above quote for a moment and try to let it sink in...It takes bond purchases worth 10 percent of GDP to lower yields by a whopping 50bs?! Hold the phone! Think about that! US GDP is roughly $20 Trillion. That means the Fed would have to buy $2 Trillion worth of bonds just to reduce yields by a measly 50bps. Hang on a moment while I laugh myself off of this chair...

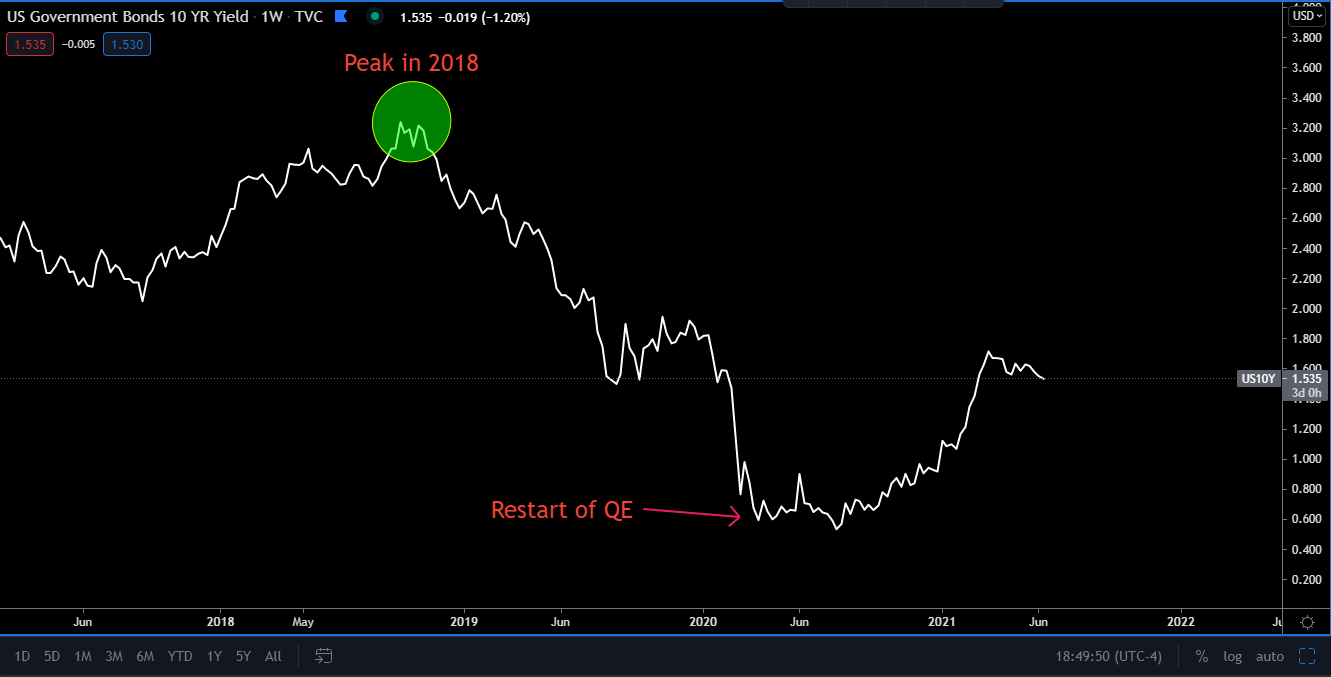

The last reflationary period ended towards the end of 2018. Let’s look below at the 10-year yield. It peaked in October of 2018 at about 3.25% (while the Fed was hiking rates). The Fed was NOT doing QE at this time. Yields then proceeded to drop to 1.42% in August 2019. In September 2019 the repo rate (inter-bank funding rate) spiked, signaling tight financial conditions, initiated the Fed to engage in their “not QE” program. It was dubbed “not QE” because normally during QE the Fed buys longer-dated maturity bonds. But, in Sept 2019 they began buying T-bills, which have a maturity of less than a year. The 10-y continued its grind lower until it descended sharply lower the end of Feb 2020, a couple of weeks before the Covid pandemic struck. The 10-y yield bottomed on March 9, 2020 at about 0.54%. At this point, the Fed had not officially restarted their QE program, meaning they were NOT purchasing the 10-y bond (or other longer-dated bonds). So, from October 2018 until March 2020, the 10-y yield fell from 3.25% down to 0.54% - 271bps. Yes, the market took the 10-y 290bps lower before the Fed stepped in with their QE program, after the brief selloff in risk assets in March 2020. But, wait, after the Fed restarted QE towards the end of March 2020, the 10-y yield eventually fell further. On August 4th, 2020, the 10-y yield dropped down to a whopping 0.52%. By that point there had been trillions of dollars worth of bond purchases and the 10-y yield fell 2bps lower than it’s low of 0.54% that the market created a few months earlier. Hats off to Jay Powell and the Fed for a job well done! Since then, the 10-y yield has risen to a high of 1.77% and it sits today at roughly 1.50%. So, the market took yields lower all on its own, without help from the Fed and since the Fed has started purchasing bonds via QE, yields have risen, with the 10-y rising 137bps at one point, which is in line with the current reflationary period we are in. If this isn’t a complete and utter fail, I don’t know what is. Every time the Fed starts their QE programs, yields were already falling. In other words, the Fed starts buying securities (Treasuries) that the market is already buying! If I haven’t been clear enough, from the perspective of lowering rates, QE is absolutely worthless. The Fed buys bonds to try to lower rates just a tad more (maybe 50bps) after the market has already taken rates lower for different reasons (low growth and inflation expectations). How is this stimulus? I have said this many times and I will say it again, the bond market tells the Fed what to do, NOT the other way around. Yields move independent of what the Fed is doing, contrary to popular belief.

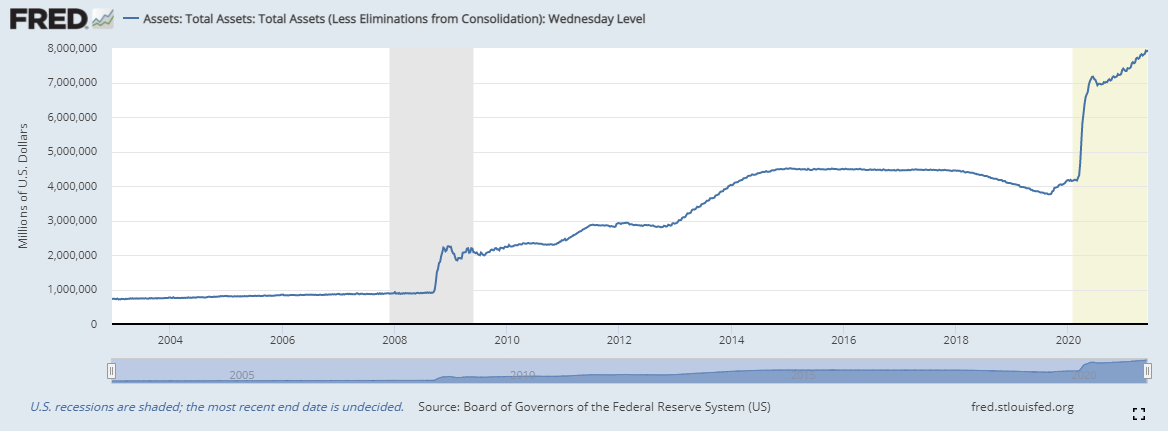

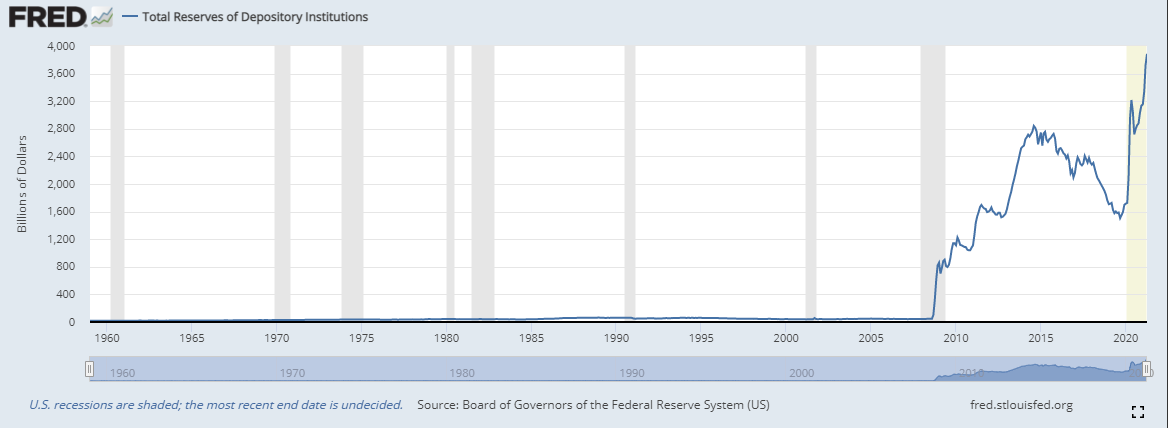

Now, notice the three channels that QE attempts to work through do NOT include “money printing”. This is because the Fed cannot print money, they can only create bank reserves. Reserves are not legal tender – they cannot be spent in the real economy (more on this later). Most believe the Fed is buying bonds and literally injecting cash into the system, which could not be further from the truth. It works like this… First, there is a Treasury Auction in which the US Treasury auctions off a specific maturity bond: 1-year, 2-year, 7-year, etc. The Fed does not participate in these auctions. Rather, Primary Dealers (big banks like Goldman Sachs, JP Morgan, Bank of America) purchase these Treasuries at auction with their own cash (bank deposits or financed through repo). The Fed interacts with Primary Dealers (PD’s) as a transmission mechanism of their monetary policy – the Fed adjusts its holdings of securities in an attempt to influence the money supply through Open Market Operations (OMO) with the PD’s. So, PD’s purchase Treasuries with their own cash. The Treasury gets the cash which the US government can then use to fund liabilities like military, social security, unemployment benefits, etc. After the auction, the PD’s are left with the Treasuries and the Treasury has the cash. This is where it normally ends, but now via QE the Fed decides to step in. The Fed, through OMO, swaps reserves (which it creates from nothing – see next paragraph) with the PD’s for the Treasuries. The Treasuries then show up on the asset side of the Fed’s balance sheet with the newly created reserves as its liability. On the bank balance sheet, under assets was Treasuries but is now reserves because of the asset swap. All that is really happening is the Fed is swapping reserves for Treasuries – one safe asset for another. Reserves show up on the liability side of the Fed’s balance sheet (see below), expanding the balance sheet, making it look like money was printed when it clearly was not. Notice how reserves were nearly non-existent prior to 2008 and yet, the market found a way to purchase Treasuries. Again, all that is happening is the Fed is swapping reserves for Treasuries. When you look at QE from the perspective of the Fed it looks like money printing because of the expansion of both sides of their balance sheet (more on this later). Assets increase because the Fed is adding Treasuries to its balance sheet and their liabilities also increase because they create offsetting reserves which are a liability for the Fed and an asset for the banks – one’s asset is another’s liability and vice versa. But, when you look at QE from the perspective of the banking system, all that is really happening is the Fed is removing one safe asset off the bank’s balance sheet (Treasuries) and replacing it with another safe asset (reserves). That cash that initially went to the Treasury came from the market – in this case, primary dealers. There was never any need for the Fed. All reserves really tell us is what the Fed is doing. They tell us nothing about what is happening in the real economy because reserves never make their way into the real economy.

What is a reserve you ask? Jeff Snider, Head of Global Research for Alhambra Investments says, “it is a byproduct of an accounting input” – an offsetting liability to the increase on the asset side of the Fed’s balance sheet. When the Fed “buys” bonds they are really just swiping them off the hands of the PD’s. The bonds show up on the asset side of the Fed’s balance sheet. To offset this, the Fed also expands the liability side of their balance sheet, by creating reserves which they give to the PD’s. This is what is meant by a “byproduct of an accounting input”. This will become clearer in a moment when we take a basic look at a balance sheet. To quote Jeff Snider again, “bank reserves are not money, but a legally authorized substitute to satisfy reserve requirements”. At the end of the day, reserves are used to make it appear that the Fed is printing money (this is the signaling channel), and at best, they satisfy regulatory requirements. To repeat what I said earlier, reserves are NOT legal tender – they cannot be spent in the real economy, therefore they are not money. Reserves cannot leave the banking system. Among banks, reserves can act as money because reserves can be used to settle transactions between participating banks (banks that have an account with the Fed). However, they cannot do much else. Reserves are very limited, whereas the money you and I are familiar with whether it be physical or electronic, is quite dynamic. For a closer look at the balance sheet accounting with illustrations, I recommend Jeff Snider’s article titled, “OK, Bank Reserves; Let’s Do This One More Time”.

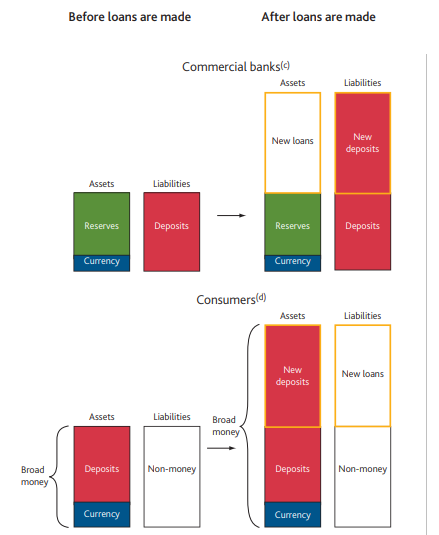

Okay, if the Fed can’t print money, who can? The banking system. Nearly all money creation nowadays happens in the banking system. Now, banks aren’t literally creating dollars that we carry in our wallets (only the Treasury can create those), but what they can do is expand and contract the supply of credit. We have a credit based monetary system and the money supply expands and contracts through the creation and destruction of credit. Let’s say you deposit $100 into your bank. You are giving the bank your $100 in exchange for a bank deposit, which is an IOU that the bank owes you. Now, everyone, from banks to businesses, to households all have balance sheets. Assets fall on the left side and liabilities on the right side of the balance sheet. Money is created by commercial banks expanding both sides of their balance sheet (I will explain in a moment). It’s important to remember that one’s asset is another’s liability and vice versa. So, the $100 deposit shows up on the liability side of the bank’s balance sheet (because they will owe this money back to you) and cash (reserves) you gave them shows up on the asset side of their balance sheet.

Let’s take a look at the illustration below (courtesy of the Bank of England from the paper titled ‘Money Creation In The Modern Economy’) to gain a clearer understanding. Just note, this is oversimplified just to gain an understanding... As you can see, on the commercial bank side, before loans are made, you have reserves and currency as bank assets and deposits as liabilities. Deposits are liabilities for banks because after you deposit money with your bank, you can withdraw it at anytime. Remember, you give the bank cash, and they give you a bank deposit, which is an IOU that the bank must pay to you when you go to them for a withdrawal. If you look to the right side of the illustration, after loans are made, you can see that money was created by an expansion of both sides of the bank’s balance sheet. They created new deposits which are a liability (owed to the borrower) and received a new loan (borrower’s debt) as an asset. The new loan is an asset for the bank because the borrower must pay back that loan plus interest. Money (credit) was created by the bank expanding the liability side of their balance sheet – creating a new deposit which shows up in the borrowers account. This liability is offset because the new loan that was created is also an asset for the bank. If you look at the consumers balance sheet, before the loan is made they have deposits and currency as their assets and currently for simplicity sake, nothing as a liability. But, after the loan is made, the consumer gets a new deposit (credit from the loan), which expands the asset side of their balance sheet and an offsetting liability, the new loan (debt). The new loan is a liability for the consumer because it is debt, and it must be paid back. Notice on the consumer balance sheet— broad money (currency + deposits) have expanded after the loan was made due to the new deposit created by the bank. So, from an accounting perspective, money creation by commercial banks is simply an expansion on both sides of the balance sheet. Now, once the principal portion of that loan is paid back, that credit is destroyed and the credit (money) supply contracts by an equal amount. The only money that stays in the system is the principal portion of the loan, assuming it too is paid.

This differs from the fractional reserve system that most believe is how banks create money. In a fractional reserve system, new deposits are needed in order for banks to lend. But as you can see from above, that is not what happens. Commercial banks do not need new deposits in order to lend, rather they create new deposits by lending money into existence. Unlike the fractional reserve system, which is limited by bank deposits, in the system just described, theoretically banks have no limits on how much money they can create. The constraints on commercial bank’s ability to lend are things such as: risk versus reward, balance sheet constraints, regulatory requirements, business and household’s appetite to borrow (which depends on many factors like interest rates), competition among the banking system and other financial entities that can lend, and monetary policy which influences interest rates. We won’t get into any of this today, however.

So, just to clarify all of this...both the commercial banks and the Fed can expand both sides of their balance sheet, except only the banks are creating money in doing so. When the banks expand the liability side of their balance sheet by creating new bank deposits in the form of new loans, they are creating new money. You and I can take that money (credit) and spend it directly into the real economy. Whereas, when the Fed takes Treasuries off of the primary dealer’s balance sheets and creates an offsetting liability in the form of reserves — well, reserves cannot leave the banking system, thus, never making it into the real economy. Bank liabilities are money whereas the Fed’s liabilities are not. For all of those touting about hyperinflation (there are many), we will get it overnight if and when congress rewrites the Federal Reserve Act and makes the Fed’s liabilities legal tender— money that can be spent in the real economy. This is extreme, but a legitimate possibility if we get another deflationary shock similar to March 2020. Until then, reserves are nothing more than some fancy accounting work.

Some have argued that it doesn’t matter if banks are lending to consumers or to the government (by buying Treasuries), lending is lending. Banks may not be lending to consumers directly, but if they are lending to the government and the government hands that money to the public, then what’s the difference? This will be inflationary, goes the argument. Now, this can be inflationary if the money finds itself in the right hands and is spent in the right places (the real economy). But, like we have seen over the past year with a large portion of stimulus checks being used to pay down debt (deflationary) and buy financial assets, this often isn’t the outcome. However, the big difference lies in the credit supply. There are two types of debt: bank debt and collateralized debt. Our example above with the bank’s loaning money into existence is considered bank debt – bank extends new credit by creating new customer deposits. Collateralized debt happens when a bank (or investor) purchases a government bond with their own cash. The government gets the cash and in exchange the lender receives a Treasury – collateral backing the loan. The big difference is that one is an expansion of credit and the other is not – bank debt expands the credit (money) supply, whereas collateralized debt does not. Collaterlized debt is simply a redistribution – taking money from one part of the economy and sending it to a different part of the economy. We will get into this in more detail in part 2. Bank debt is much more likely to lead to inflation because the money (credit) supply is expanding. You will now have more money chasing the same amount of goods and services (assuming supply stays the same). However, since loans and leases in bank credit spiked from March – May 2020 , because of the government guaranteed loans, it has consistently contracted on a month-over-month basis (the chart on this is above from earlier in the article).

So, to recap, QE attempts to operate through three different channels, none of which actually partake in the creation of money. This is why the economy has yet to recover from the Global Financial Crisis, let alone the most recent recessionary stint. The world is deprived of dollars and QE has proven unable to fill the gap. This is also why inflation has never been sustained since the Global Financial Crisis of 2007-08, despite numerous periods of inflationary pressures (reflation), like the one that is currently happening. The Fed has no printer, but rather a bookkeeper’s pen. The only new money being created, is done via the banking system. However, there is one question that I have not addressed: if the Fed isn’t printing money, then why has the money supply (M1, M2) increased? This is one of the main arguments that people give to prove the Fed is actually printing money, the fact that the money supply metrics have gone up. I will address why the money supply metrics are not accurate and does not actually prove that the Fed is printing money in part 2.

What does all this mean? Again, the Fed is not creating money. And if they are not creating money, we have a problem because there is a global dollar shortage, one that has yet to be replenished since the GFC. This is why the March 2020 liquidity event happened, because the world needed more dollars than the system could offer. What’s really missing from the system is quality collateral, because when there is enough quality collateral in the system, dollars are flowing. QE is dangerous and makes the system more vulnerable because it not only is not creating money, it is removing quality collateral from the system that it desperately needs. This is what we will explore in part 3, the dangers of QE and its consequences, and by default, the repo and eurodollar market.

Author

Ryan Miller

Ryan Miller Trading Economics

Ryan Miller received a Bachelors Degree in History from William Paterson University. Through his studies of U.S. history, he developed an interest in the implications the financial markets have on the economy.