Inflation Expectations Moderate

In my last article, I mentioned the big difference between the NY Fed and Atlanta Fed’s model for Q1 GDP growth. I tended to side with the Atlanta Fed’s model because it has a longer track record and was closer to the street’s average estimate. Today both estimates updated. The Atlanta Fed’s model stayed at 0.9% which is slightly less than 1% below where the street is. The NY Fed’s model was lowered from 3.2% to 2.8%. Its Q2 estimate was also lowered from 3.0% to 2.5%. It seems likely that a weak quarter will be reported now that even the bullish NY Fed estimate is coming closer to the mainstream consensus. The only way for an above 3% growth quarter to occur would be for another anomaly like the one seen in Q3 where soybean exports added 0.9% to growth.

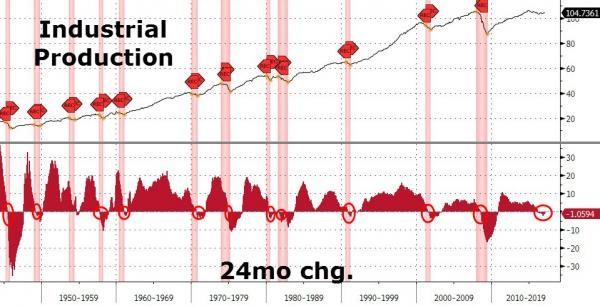

Industrial production missed expectations for 0.2% growth. It showed no month over month growth in February. Even though it missed expectations, it wasn’t a bad report because it was driven down by low utility usage because of the warm February. Utility production fell 5.7%. That will go back up in March because it has been very cold. Factory production increased 0.5% and mining output increased 2.7% because of oil & gas drilling. The rig count has been increasing which signals the fracking firms have lowered their cost basis. That’s bad news for OPEC.

Taking a step back, industrial production has been moderately weak as you can see from the chart below. This is the first time industrial production has declined for 24 months without being in a recession. At the same time, it’s understandable why the economy isn’t in one because the decline has been so shallow. Based on this chart, it’s still reasonable to be on alert for a recession this year.

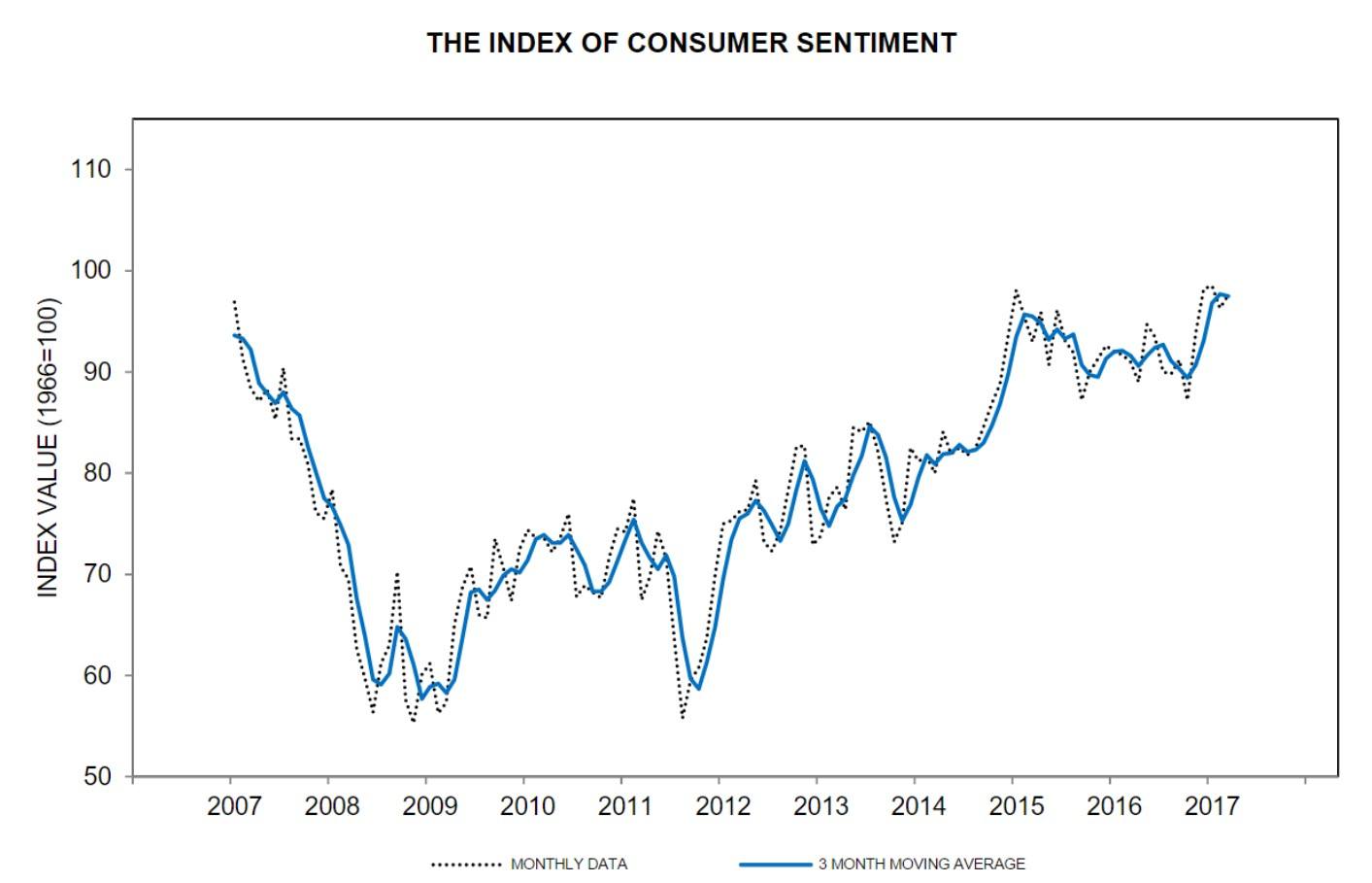

The other major economic report which came out Friday was the consumer sentiment survey. It was a good report as the sentiment increased 1.3% from last month to 97.6%. The current conditions index was up 2.7% from last month and the expectations index was up 0.2% from last month. While this is good news, I’m starting to think the survey is becoming worthless because it is so partisan in nature. There’s no way the economy is terrible for Democrats and great for Republicans. It’s not possible to have such a difference. 87% of Republicans and only 22% of Democrats think the economy will do well in the next five years. They clearly are basing their answers off whether they like Trump. That’s not helpful for investors and economists. I want to know their opinion on the economy based off what they are feeling about their own circumstances. Everyone already knows that some people like Trump and some don’t; that makes the latest sentiment reports less meaningful.

There has been a sharp decline in the 10-year bond yield this week which shows investors have a bearish outlook on inflation. It has fallen about 12 basis points from its cycle high to 2.50%. As I’ve said, the Fed is raising rates just as oil prices are falling and overall inflation gets back to moribund levels. The Fed is hoping for inflation, but it’s not strong enough to justify hiking rates every meeting this year like Gundlach has suggested. On Monday, the NY Fed released the consumer inflation expectations survey. The expectation for the year ahead inflation stagnated at 3% and three-year inflation expectation increased to 3.0% from 2.9%. Part of the reason why the 10-year fell Friday is because the University of Michigan showed declining inflation expectations. 5-year inflation expectations fell to 2.2% from 2.5% last month which is the lowest since 1980. This survey suggests the Fed’s hawkishness may be a mistake.

As I mentioned, oil prices are falling because of American shale production. The CPI is soon going to be negatively affected by oil because of base effects (year over year change). As you can see from the chart below, in 2016 oil started boosting CPI. March will be the last month this happens if oil stays at about where it is now. This could push CPI lower. The core CPI ignores food and energy because they are more volatile. However, it would be monetary malpractice to completely ignore costs that effect the average person simply because they’re volatile commodities. If I was at the Fed, this change would cause me to be more dovish.

Another aspect which may cause the Fed concerns is that rent inflation is accelerating while hourly earnings aren’t. This puts Americans in a bind as their bills are increasing faster than their pay. If the Fed raises rates, it could help with rent inflation, but hurt hourly earnings. If it’s more dovish, rents and pay will increase. Neither choice solves the problem. I think the Fed’s QE boosted asset prices which has caused a bubble in housing. QE did nothing for the average worker as businesses simply bought back more shares. Any issue with inequality is directly related to QE.

The Fed may hint that equity volatility is too low and claim it raised rates to prevent a bubble from forming. However, if it was serious about stopping bubbles, it would unwind the balance sheet. My expectation is nothing will be done and when another crisis hits, it will be expanded.

Conclusion

It looks more likely that GDP growth in Q1 will be weak now that the NY Fed’s model lowered its forecast. Inflation expectations aren’t high enough to necessitate rate hikes. I’m not personally against rate hikes because I think rates have been too low for too long. My point is asking the question of why now is a good time to raise them, given the fact that the Fed hasn’t done so in years. Quantitative Easing has caused the decision on interest rates to be tougher than normal because rent inflation is up while hourly earnings are stagnant. Some doves want to keep rates low to boost hourly earnings, but they aren’t keeping rent inflation in mind when they state that policy goal. Every action has numerous consequences, so having a myopic focus on one indicator is a fool’s game.

Don Kaufman: Trade small and Live to trade another day at Theotrade.

Author

TheoTrade Analysis Team

TheoTrade, LLC

Don Kaufman, Co-Founder, Chief Derivatives Instructor (Trader Stocks, Options, Futures) Don is one of the industry's leading financial strategists and educational authorities.