GBP/USD Weekly Forecast: Sellers have control as the focus shifts to UK data and US CPI

- Employment data on Tuesday and the monthly GDP on Wednesday will be the highlights in the UK next week.

- In the US, the CPI on Wednesday will be the centre of attention.

- Risks in the GBP/USD pair are tilted to the downside while below 1.2660.

After a brief and failed correction, the GBP/USD pair resumed its downside movement and dropped to its lowest level in three months on Thursday. It reached a bottom at 1.2440 and then rebounded modestly, struggling to retake the 1.2500 level. The Pound was influenced by relatively dovish comments from Bank of England (BoE) officials. At the same time, positive US economic data continues to support the strength of the Greenback. The focus now shifts to upcoming UK employment and GDP data and the US Consumer Price Index (CPI) in anticipation of the Bank of England and Federal Open Market Committee (FOMC) decisions scheduled for September 20 and 21, respectively.

Between a stronger USD and a cautious BoE

The British Chambers of Commerce (BCC) released a report during the week that essentially mentioned that the UK will avoid a recession, but growth will be practically inexistent. Expectations are for the GDP to grow by 0.4% during 2023. The UK's economic conditions weighed on the Bank of England's tightening expectations and weakened the Pound.

Bank of England officials, including Governor Andrew Bailey, Deputy Governor Jon Cunliffe, and external member Swati Dhingra, gave their testimony to the Treasury Select Committee. According to Dhingra, interest rates are "already sufficiently restrictive." Bailey and Cunliffe stated that policy is restrictive and close to the terminal level. The Governor sees inflation falling "markedly" by the end of the year.

Despite the latest data and BoE comments, a 25 basis point rate hike in September seems likely, and additional hikes by year-end cannot be ruled out if inflation figures surprise to the upside. However, softer expectations regarding tightening from the BoE continue to affect the Pound.

A report that garnered attention from the UK was a decline in house prices. The Halifax House Price Index dropped 2.4% in July to the lowest level in 14 years.

Meanwhile, the US Dollar remains supported by positive US economic data. Recent numbers do not indicate a booming economy, but they also do not suggest a hard or soft landing; in fact, they don't even indicate a landing yet for the overall economy. Concerns about the manufacturing sector were offset this week with an improvement in the ISM Services PMI, which rose to 54.5 in August. Another report showed that Initial Jobless Claims dropped to 216,000, the lowest level since February. Unit Labor Costs for the second quarter were revised from 1.6% to 2.2%.

The US data did not necessarily lead to expectations of a rate hike in September, but it did contribute to the notion of "higher for longer" interest rates. The economic context in the US supports the possibility of further rate hikes if the Federal Reserve deems it necessary to curb inflation. This contrasts with other economies such as the UK, which need a more cautious approach to tightening monetary policy further. The divergence in economic performance strengthens the position of the US Dollar. If these trends persist, the Greenback will retain its momentum.

Week Ahead: UK Employment and GDP, US CPI

During the weekend, China will release inflation data that could weigh on market sentiment at the opening. The G20 meetings kick off this Saturday. The Pound may perform better with a risk-on flow, but it could suffer from a deteriorating market sentiment. Hence, if Wall Street recovers momentum, GBP/USD could benefit.

On Tuesday, the UK employment report is due. The Unemployment Rate is expected to have risen from 4.2% to 4.3% for the three months to July, and Average Earnings, excluding bonuses, are seen moderating their annual increase from 7.8% to 7.6%. This number will be important as a weaker figure would provide more evidence that the peak in interest rates is near.

On Wednesday, more UK data is due, including July Gross Domestic Product (GDP), Industrial Production, and trade data. A decline in Industrial Production is expected. Figures pointing to a deceleration in activity would increase the pressure on the BoE to halt its tightening cycle. The next BoE decision is on September 21.

The week's most important report will be the US Consumer Price Index (CPI) on Wednesday. If CPI continues to slow, the Greenback could suffer as it would solidify expectations of a pause from the Fed at the September 19-20 FOMC meeting. Conversely, hotter-than-expected figures will keep the doors open to more tightening, though not necessarily at the next meeting. Such a scenario could accelerate the Dollar's upside. Fed officials will be in the lockout period, so markets won't hear from them.

The US will release Retail Sales and the weekly Jobless Claims report on Thursday. Additionally, the European Central Bank (ECB) will have its monetary policy meeting. Consensus is divided between a final 25 basis point rate hike and a pause.

On Friday, the Bank of England will release its quarterly survey of "public attitudes to inflation."

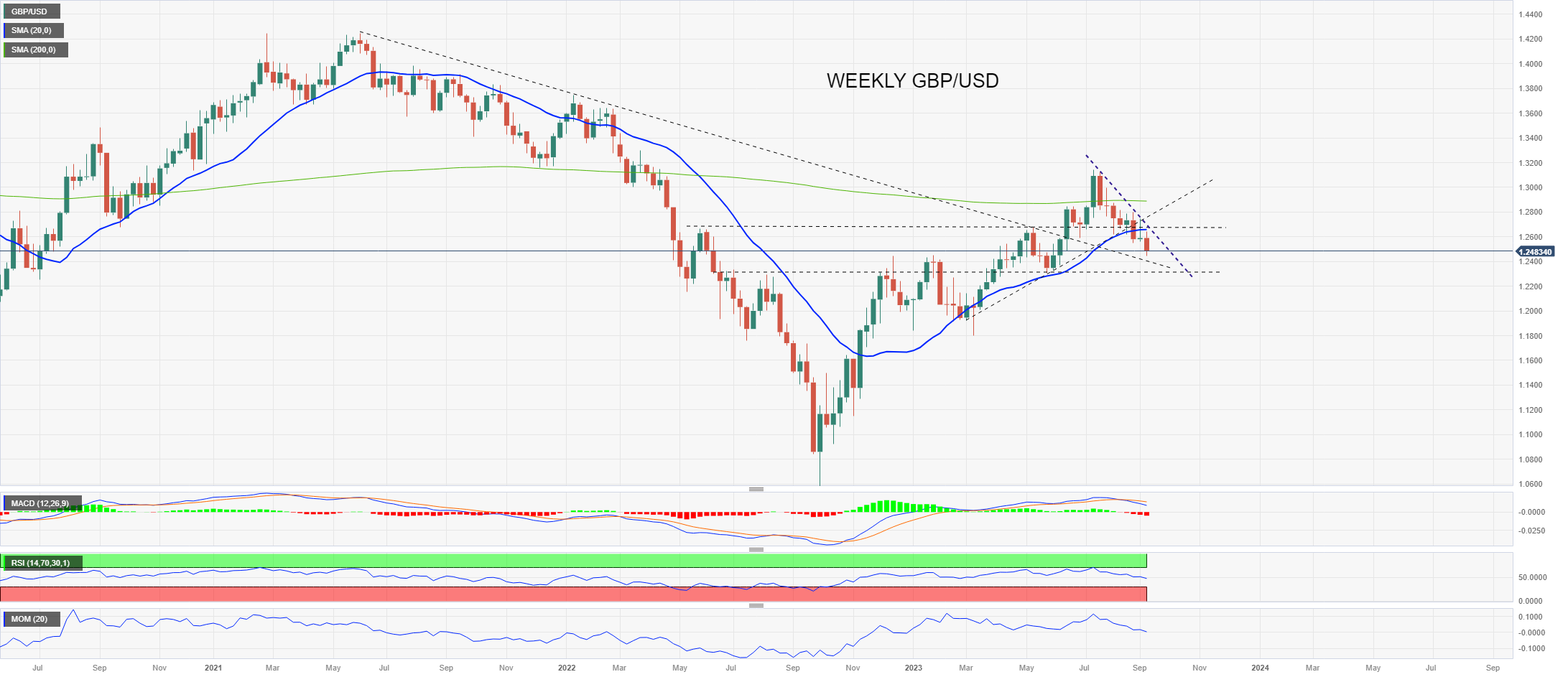

GBP/USD: Technical outlook

The GBP/USD has consistently fallen since late August, and some consolidation appears overdue. However, there are no signs of that happening, and on the contrary, the pair continues to break key support levels. On the daily chart, the price is very close to the 200-day Simple Moving Average (SMA) at 1.2425.

On the upside, the key area is observed between 1.2660 and 1.2680, which represents the confluence of a downtrend line and the 20 and 100-day SMAs. A break above that level would significantly change the outlook for the Pound. As long as the price remains below that area, the bias will remain bearish.

In line with the daily chart, the weekly shows a solid bearish bias, with the third close below the 20-week SMA. The path of least resistance appears to be to the downside, although it is not exempt from corrections or periods of consolidation. The 1.2450 area is a relevant support level that, if held, could trigger some correction. Conversely, a decline below that level would shift attention to the next medium-term support level, around 1.2300.

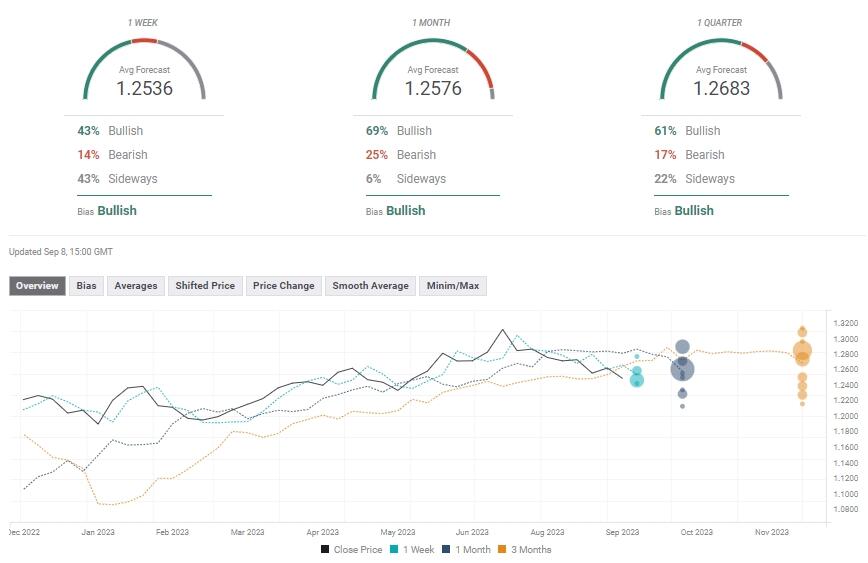

GBP/USD: Forecast poll

According to the FXStreet Forecast Poll, the GBP/USD is expected to remain relatively stable in the near term. The average price forecast for next week is 1.2535, slightly above the current level. The monthly average forecast is at 1.2576.

For the quarter, most forecasters anticipate the pair to move to the upside, with expectations centered around 1.2900. However, the one-month average stands at 1.2685, as some analysts anticipate the price to move below 1.2400 during that period.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.