"Rearranging the deckchairs on the Titanic": UK's fiscal crisis outlasts another Prime Minister

Keir Starmer's resignation as the United Kingdom (UK) Prime Minister comes ten years after the Brexit referendum vote, a coincidence that financial markets have been quick to note. The British Pound (GBP) trades around 1.3220 against the US Dollar (USD) on Thursday, down 0.23% on the day, remaining under pressure not far from the year's low of 1.3159 reached in late March.

This unprecedented political and economic context warrants a closer reading, one that goes beyond the short-term mechanics of the GBP/USD pair alone.

A decade of political turmoil and its economic legacy

The referendum of June 23, 2016, remains one of the most structurally significant events in contemporary British economic history. Ten years on, the toll is heavy. According to research published by the London School of Economics (LSE), Brexit reduced the United Kingdom's Gross Domestic Product (GDP) by 2% to 3% by the end of 2019, before the effects of the Covid-19 pandemic. More recent analysis suggests this cost may have reached 8% of GDP per capita by early 2025, equivalent to a loss of £3,300 per person per year.

Goods exports to the European Union (EU) fell by 10% to 15% following the implementation of the Trade and Cooperation Agreement (TCA), while business investment is estimated to have been reduced by around 15% in 2024 as a result of prolonged uncertainty.

On the currency front, the British Pound absorbed a structural depreciation of around 10% in the immediate aftermath of the vote, from which it has never fully recovered.

The decline in the currency mechanically pushed up the cost of imports, contributing to a rise in consumer prices estimated at around 3%, representing an additional cost of roughly £870 per UK household per year, according to the same LSE research.

This exchange rate instability accompanied a succession of political crises: Six Prime Ministers followed one another from David Cameron through to Keir Starmer, whose tenure lasted less than two years. Andy Burnham, if confirmed in the weeks ahead, will be the seventh.

The political transition: A coronation in sight, and its implications

The current dynamics surrounding the succession are, for now, relatively orderly. Starmer indicated that nominations for the Labour leadership would open on July 9, to complete the transition before Parliament returns on September 1. Wes Streeting, one of the most credible potential challengers, has already announced his support for Burnham, opening the door to a process without a genuine membership vote, comparable to the handover between Tony Blair and Gordon Brown in 2007.

Analysts at TD Securities note that “the most probable outcome is a managed transfer of power sometime in August, comfortably ahead of the September 1st Parliamentary session,” in the scenario of an uncontested candidacy, which would minimise uncertainty and allow for a smooth transition.

The absence of open competition is broadly seen as a stabilising factor for UK assets in the near term. The British Pound did indeed close Monday as the best-performing G10 currency, up 0.14% against the US Dollar (USD), while yields on 2-year and 10-year UK government bonds (Gilts) fell by 4.5 and 3.4 basis points respectively, in line with their European counterparts. The Financial Times Stock Exchange 100 (FTSE 100) index meanwhile gained 0.72%.

This surface-level rebound nevertheless masks a more complex reality. By Tuesday, the GBP had already retreated and the FTSE 100 was down 0.41%, a sign that initial relief quickly gives way to deeper questions.

The key variable: Who will be the next Chancellor of the Exchequer?

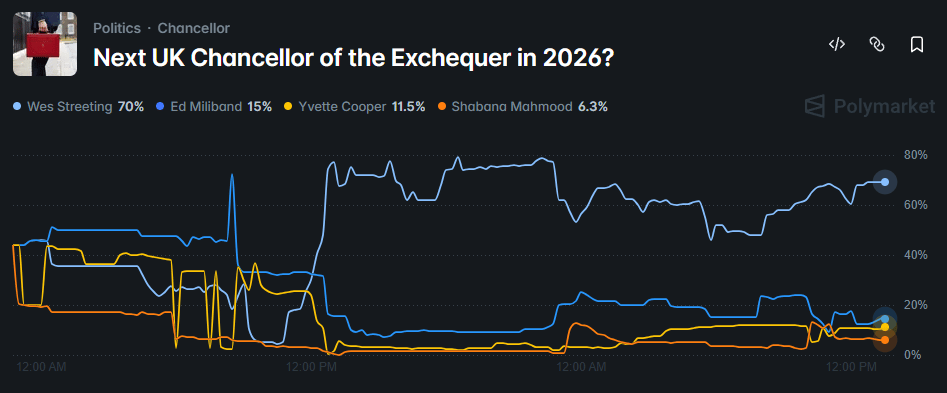

The real question for markets is less the identity of the next occupant of 10 Downing Street than that of the next Chancellor of the Exchequer. Three names are circulating prominently: Wes Streeting, regarded as a market-friendly candidate given his moderate positions. Yvette Cooper is also seen as a continuity option. And Ed Miliband, the former Labour leader from 2010 to 2015, whose left-leaning orientation is considered less favourable by investors.

According to Polymarket, Wes Streeting leads the race with a 70% probability of becoming the next Chancellor, far ahead of Ed Miliband at 15% and Yvette Cooper at 11.5%. Shabana Mahmood, the current Justice Secretary, is also in the running at 6.3%, though markets assign her only an outside chance at this stage.

Deutsche Bank argues that Burnham's choice of Chancellor will act as a signal of his intended fiscal direction, adding that "the risk-reward remains skewed towards a grind firmer in the Pound versus select risk-sensitive currencies."

BNY's Geoff Yu argues that a sustained improvement in GBP performance hinges on renewed cross-border interest, which has been lacking since the second half of 2025, and that such flows are unlikely to pick up until a new Chancellor is appointed.

The fiscal question at the heart of uncertainty

Beyond the political line-up, it is the trajectory of public finances that is crystallising tensions. The United Kingdom already posted public borrowing of £23.3B in May, 30% higher than a year earlier and above the forecasts of the Office for Budget Responsibility (OBR).

Burnham has at times made comments that unsettled Bond markets, notably when he declared last September that the country needed to move beyond being in hock to the Bond market, a remark that temporarily triggered a sell-off in Gilts. He has since walked back that position, stating he is completely committed to the fiscal rules.

Nomura argues that "the path of the GBP may depend more on the BoE outlook than on Burnham," while warning that "tail risks remain in the form of tweaks to fiscal rules or higher taxes."

Nick Rees, Head of Macro Research at Monex Europe, cited by Reuters, offers a blunt but lucid diagnosis: "Right now we’re rearranging the deckchairs on the Titanic. At the end of the day the UK political situation is dictated by its fiscal situation."

Market vigilance also centres on the broader direction Burnham may set in the autumn, as a budget presented later in the year would be the first real test for his administration.

Implications for the British Pound: A structurally challenging environment

Against this backdrop, the British Pound is navigating a difficult underlying trend. Lee Hardman, senior currency analyst at MUFG, sums up the situation: "The key moment will be that autumn period when the new leader takes over and we can see what changes in policy we see, but I think the risks are tilted to the downside."

Kit Juckes, Chief FX Strategist at Societe Generale, echoes this view: "It's more likely than anything else that Sterling remains under pressure as we have higher inflation, higher rates and then we wait for the next round of news." Juckes sees EUR/GBP likely to move one to two percentage points higher and a test of the 1.30 level for GBP/USD seen as possible over the summer.

Several structural factors compound the political equation. Nomura anticipates an interest rate differential narrowing by 125 basis points between the Bank of England (BoE) and the European Central Bank (ECB) by the end of 2027 (75bp ECB hikes, 50bp BoE cuts), which would erode the carry appeal of the British Pound.

Furthermore, weak domestic growth - the International Monetary Fund (IMF) forecasts only 0.8% growth for the UK in 2026 - mechanically limits the prospects for a meaningful GBP recovery.

However, as noted by Rees: “The one caveat I would give to all this is I think markets could quite like Wes Streeting as chancellor. That’s an upside tail risk to the Pound… I think markets could be pleasantly surprised.”

In the near term, an orderly resolution of the leadership crisis may provide a temporary floor for the British Pound, but the potential for a sustained rebound remains contingent on the emergence of a credible fiscal strategy under the incoming administration.

In the daily chart, GBP/USD trades at 1.3218, keeping a bearish near-term tone as spot holds below the 200-day Simple Moving Average (SMA) at 1.3409 and the 100-day SMA at 1.3440, both reinforcing a cap from the broader downtrend resistance structure. The Relative Strength Index (RSI) at roughly 34 still leans toward bearish momentum but stays above oversold territory, suggesting selling pressure persists yet lacks capitulation signals for now.

On the topside, initial resistance emerges at the 200-day SMA around 1.3409, with a stronger barrier clustered near 1.3440 where the 100-day SMA converges with a descending trend line, while a higher downtrend line comes in near 1.3563. On the downside, the first notable support area comes at the 1.3165-1.3145 range, as defined by past lows, followed by the horizontal level at 1.3010, where a retest would likely attract dip-buying interest or, if broken, open the door to a deeper bearish extension.

(The technical analysis of this story was written with the help of an AI tool.)

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.