Regime change: Inside Kevin Warsh's first move to make the Fed unreadable on purpose

The rate did not move. That was the least interesting thing about Kevin Warsh's first meeting in charge of the Federal Reserve (Fed). The Federal Open Market Committee (FOMC) held its benchmark at 3.50%-3.75% for the fourth straight meeting, exactly as priced, and then the new chair used his first press conference to dismantle the machinery the market has leaned on for a decade.

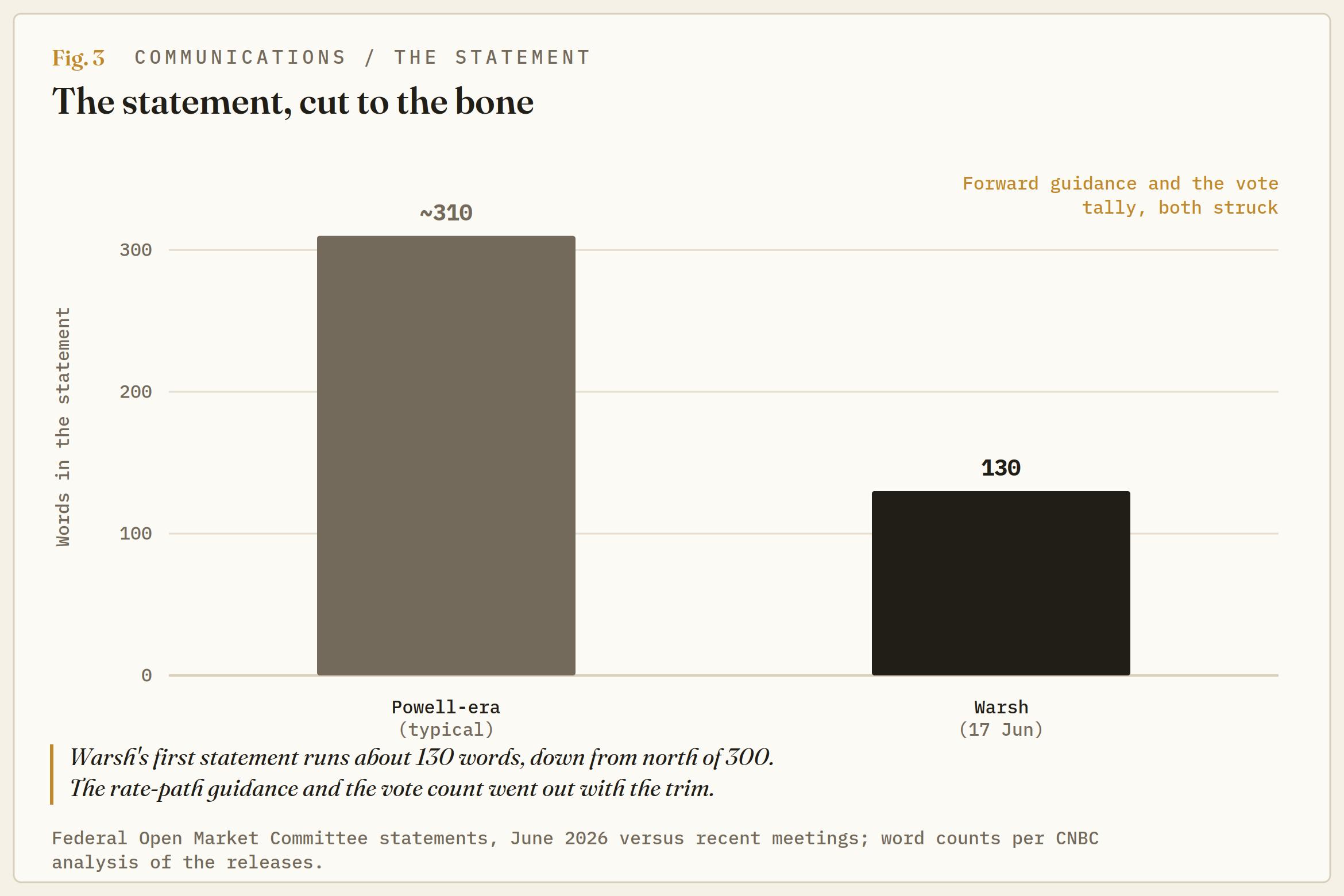

Forward guidance: gone. The Chair's own dot: withheld. The policy statement: cut from north of 300 words to roughly 130, a version Warsh himself called curt. Five task forces commissioned to rethink how the Fed talks, what data it trusts, and how it defines inflation. Add in a heavy hint that the press conference you were watching may not run at every meeting from here. Kevin Warsh promised "regime change" on the way in. On day one, he delivered it, and the tape repriced off the plumbing, not the policy.

For a meeting that changed no policy, the market reaction was violent. The two-year Treasury yield, the cleanest read on the rate path, leapt about 16 basis points past 4.20% to a one-year high. The US Dollar Index posted its best session in almost a year. Gold fell more than 2%, and the major equity indices finished lower, with the Nasdaq the worst of the three. None of that came from what the Fed did. All of it came from what the Fed stopped saying.

A curt statement and a missing dot

The statement was the tell: under Jerome Powell, the FOMC release ran past 300 words and told you, in carefully negotiated language, which way the committee leaned. Wednesday's ran about 130. It dropped the forward guidance that had pointed at a future cut. It dropped the vote tally, noting only that the decision was unanimous. It called the economy solid and inflation elevated, partly on energy supply shocks, and left it there: just the facts, in Warsh's framing, as the committee judges them.

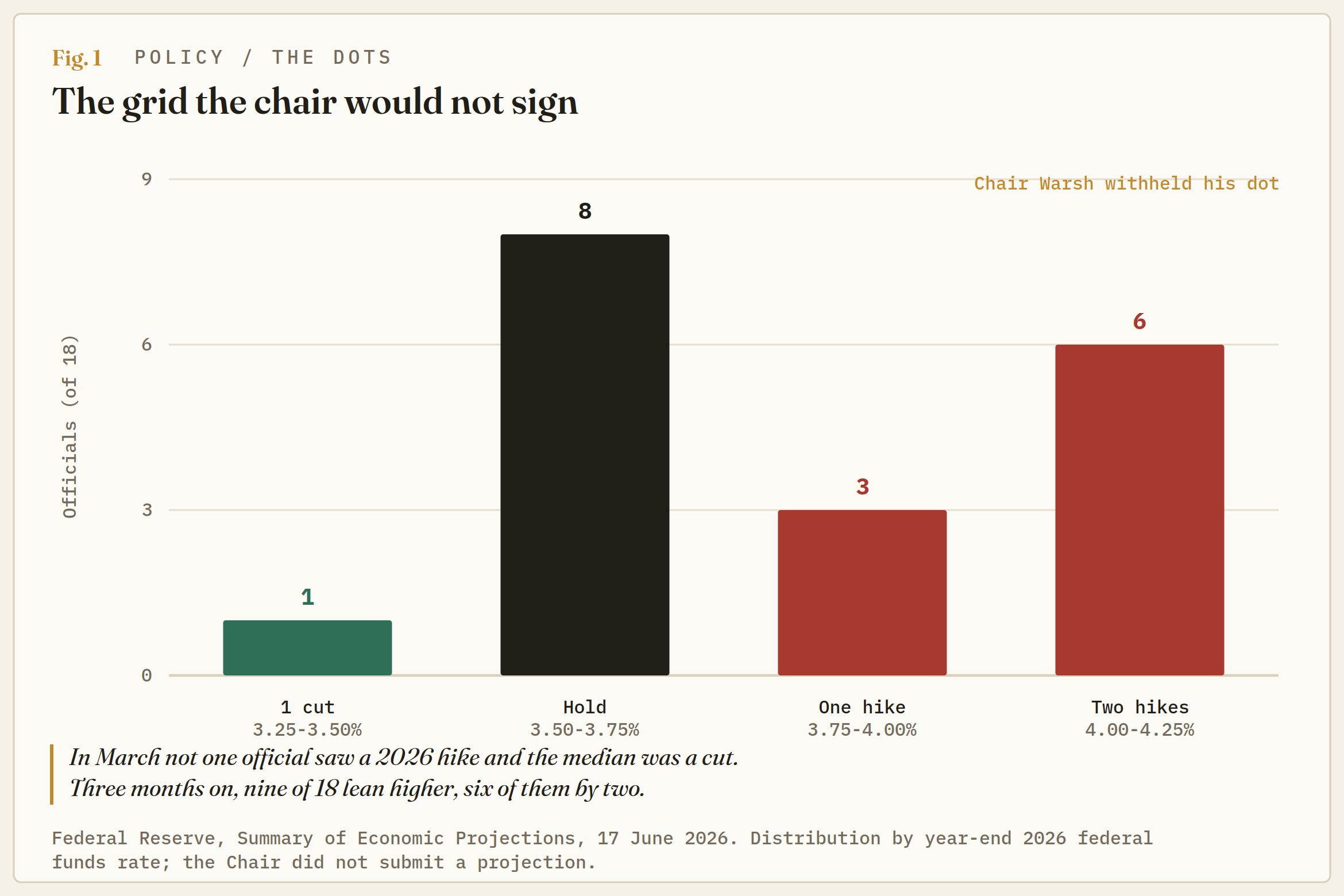

The new chair then declined to add his own dot to the Summary of Economic Projections (SEP), the quarterly grid showing where each official sees rates heading. He has criticised that grid for years, arguing it locks the Fed into a path, so he left a hole in it. Both moves carry the same message: the Fed will tell you less about where it is going, on purpose.

Kevin Warsh wants you trading the data, not the Fed

Pressed on whether less guidance just means more volatility and less transparency for ordinary Americans, Warsh did not flinch. Markets work best, he argued, when they react to incoming data, and worst when they burn their energy guessing how the Fed will react to it. Push the read back onto the economy and prices will carry better information back to the Fed in return. It is a tidy theory with a sharp edge: it deliberately shrinks the Fed's communicative footprint and hands price discovery back to the tape.

The data task force is the same idea turned inward. Kevin Warsh wants to cut the error bars on real-time decisions using private-sector data and techniques he says are more refined than sorting a print into core or non-core. Done well, that is a faster, sharper Fed. Done badly, it is a Fed making big calls off inputs no outsider can see. He insisted the 19 officials around the table, not the task forces, still decide. He was less clear on how the rest of us are meant to audit a reaction function he has just stopped narrating.

The pump is the wrong tell

Start with the projections, because that is the real news.

In March, not one official saw a 2026 hike and the committee still pencilled a cut. On Wednesday, nine of 18 saw the funds rate ending the year higher, six of them wanting two increases, and the committee lifted its end-2026 forecast for the Personal Consumption Expenditures Price Index (PCE) to 3.6%, from 2.7%, with the Consumer Price Index (CPI) already running at a three-year high of 4.2%.

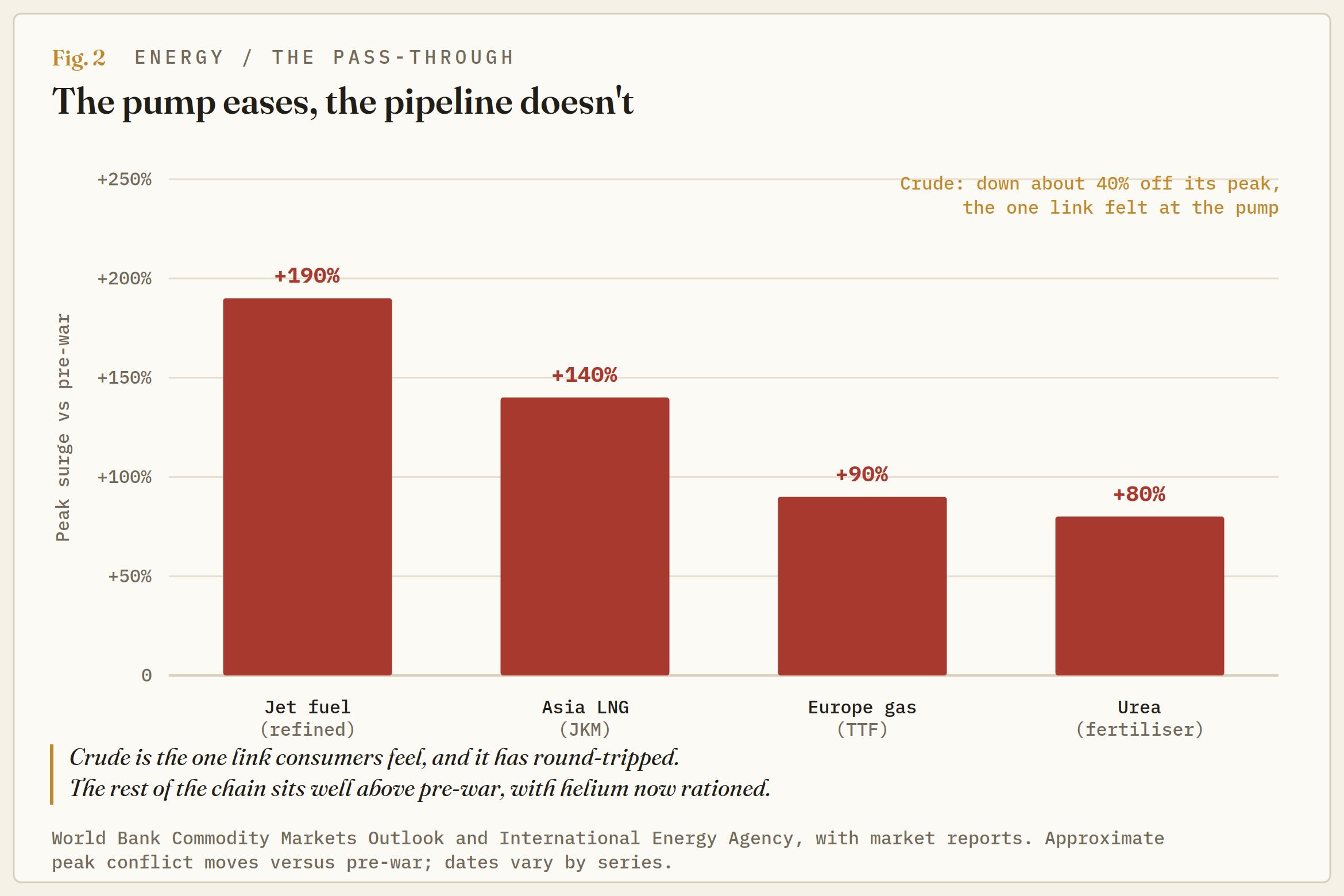

The lazy read is that the Fed is tightening into a receding shock, the mistake Jean-Claude Trichet's European Central Bank (ECB) made in 2008, hiking into an Oil spike that was already rolling over. That read watches the wrong number. The crude tick lower is first-round relief, the part you feel at the pump. But, Hormuz choked the whole energy-and-feedstock complex, not just Crude Oil, and a feedstock shock does not reach the basket all at once; it cascades down-chain with a lag.

Diesel and freight ride into the shelf price of anything that moves on a truck. Naphtha and methanol feed the petrochemicals behind plastics and packaging. Natural gas makes nitrogen fertiliser, and the Gulf supplies roughly half the world's urea, which ran up some 80% off its lows. Even helium, a byproduct of Qatari gas that the chip and hospital industries cannot do without, is being rationed. None of that reverses just because Crude prints lower this week, and two things make it stickier than the usual spike: Fertiliser has no strategic reserve to tap the way Oil does, and the hit lands on a planting-to-harvest clock, so this spring's input shock turns up in food prices in late 2026 and into 2027, long after the pump has calmed.

That pipeline is why the dots moved. The committee is not chasing the crude tick; it is pricing a bill that energy shocks always mail late, into core and food, where it is hardest to unwind.

The convenient thing about saying less

Now the politics, which are not incidental. Kevin Warsh campaigned for this job as a dove and was hired to deliver the cuts President Donald Trump spent two years demanding; Trump savaged Jerome Powell for every meeting that passed without one.

On Wednesday, Warsh delivered none, and Trump shrugged. Before the meeting, the President said he would let Warsh do as he liked and that he would be fine; from Paris afterward, with no cut on the board, he said he is "guided by what he wants," while still insisting higher rates "keep the country down." Read those together, and the deference is conditional. He has not dropped the demand for cuts; he has lent his hand-picked chair some rope. How long that rope runs is the question, and the pipeline above is what shortens it: cheaper gas and an easing headline will give Trump every reason to expect the cuts he was promised, just as the down-chain bill keeps the Fed from delivering them. That is the collision being built. It is also why the machinery matters.

The man who may be forced to hold, or hike, into a President who wants the opposite has just removed every device that would pin him to a path. No guidance, no promise to walk back. No chair dot, no published track to defend. A curt statement and fewer press conferences, a thinner paper trail. Private data an outsider can inspect, more room to justify whatever the next call turns out to be.

There are two honest reads. One is principled: Kevin Warsh has argued for 15 years that an over-talkative Fed breeds policy error and tangles itself in markets, and he is finally fixing it. The other is convenient: an administration that wants a compliant Fed has a chair quietly draining the accountability out of it, just as it may have to do something the President will hate. The reforms look identical under both. Only the motive differs, and motive is the one thing a 130-word statement will never print.

How to trade a Fed that will not tell you

So trade the consequence, not the rhetoric. With guidance gone and the Chair's dot withheld, you can no longer fade a meeting on the dots or lean on a steer buried in the statement; every economic data print between now and the next decision becomes the event.

The cleanest expressions of the higher-for-longer repricing are the front-end Treasury yields and the US Dollar, and both moved hard on Wednesday. The lean in the front end sits with the hawks while the data runs hot, and the line in the sand is the October hike, which futures put at about 60%; hold above it, and higher-for-longer entrenches, with the Dollar bid and Gold offered into rising real yields. Slip below it and the whole hawkish trade starts to unwind. The trap to avoid is the headline. A softer CPI on cheaper gas will read like the all-clear, but the pass-through shows up in core, in food at home, and in the processed-goods stages of the Producer Price Index (PPI), not in the energy line the pump dominates.

Watch those, not the front page; the hike fades when core cools, not when gasoline does. And the same gap is the political tell: the wider the daylight between a calm headline and a hot core, the harder Trump leans for the cut his own data will not justify.

Warsh got the meeting he wanted: a non-event on rates that let him reset the terms of engagement on everything else. Whether the quieter room he has built, fewer words, no dot, data only he can see, is the workshop of an independent central bank or the green room for decisions an administration would rather not see litigated in public, neither the statement nor the press conference will say. The next print, and what he does with it, will start to.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.