GBP/USD Weekly Forecast: For how long can 200 DMA hold the fort? Focus on US/UK inflation

- GBP/USD buyers staged a comeback after two consecutive weekly declines.

- Hawkish Federal Reserve expectations failed to extend the US Dollar recovery.

- Technically, downside risks still remain intact for GBP/USD amid a big week ahead.

The Pound Sterling buyers defied the downside risks and made a comeback against the United States Dollar (USD), having snapped a two-week downtrend. Despite a positive close over the week, GBP/USD appears to lack the upside conviction heading into a data-intensive week on both sides of the Atlantic.

GBP/USD recovered from a five-week low sub-1.2000

GBP/USD tumbled to fresh five-week lows of 1.1961 in the early part of the week, and thereafter, staged a decent turnaround as the US Dollar struggled to extend its recovery. Expectations surrounding the US Federal Reserve (Fed) policy tightening path continued to play a pivotal role throughout the week, as investors re-evaluated the odds of a dovish Fed pivot or a pause in the central bank’s rate hikes. The upswing in the US Dollar following the February Fed policy outcome lost steam on Tuesday, as USD bulls retreated sharply from five-week highs on less-hawkish commentary from Federal Reserve Chair Jerome Powell. Powell’s remarks on disinflation triggered a risk rally and checked the US Dollar recovery from a 10-month trough, as investors hoped that the start of the disinflationary process could prompt the central bank to slow further down on its interest rate hike campaign.

However, hawkish speeches from a bevy of Federal Reserve policymakers combined with mixed US corporate news soured sentiment in the second half of the week, allowing the US Dollar to stay afloat against its major rivals alongside the US Treasury bond yields. Minneapolis Fed President, Neel Kashkari, said that the Federal Reserve would perhaps have to raise interest rates to at least 5.4% to tame high inflation. Fed Governor, Christopher Waller, warned that interest rates could go higher than expectations. New York Fed President, John Williams, also suggested the same, citing that “we still have some work to do to get interest rates in the right place.” Markets expected the Fed to deliver two 25 basis points (bps) rate increases in March and May meetings, according to CME Group’s FedWatch Tool. However, in the face of the hawkish Fed policymakers, interest-rate options traders started betting big this week on the Fed’s terminal rate touching 6% by September, Bloomberg reported, citing preliminary open-interest data from CME Group.

Risk sentiment took a hit after Wall Street indices tumbled on Wednesday led by a sharp sell-off in Alphabet Inc. The American tech giant sank nearly 8.0% after its new AI chatbot Bard delivered an incorrect answer in an online advertisement. Encouraging news from Disney fuelled a positive shift in the market’s perception of risk and weighed heavily on the safe-haven US Dollar on Thursday. But the downside in the American Dollar remained capped by a solid rebound in the US Treasury bond yields. The choppy trading in the US Dollar extended on Friday, as investors turned cautious ahead of the US Consumer Price Index (CPI) data due next Tuesday.

Amidst the US Dollar consolidation, the Pound Sterling made recovery attempts but further upside appeared elusive following the Bank of England (BoE) Monetary Policy Report (MPR) hearings. BoE Chief Economist, Huw Pill, and policymaker, Jonathan Haskel, testified before the UK Treasury Select Committee alongside Governor, Andrew Bailey, on Thursday. Bailey emphasized that they expect inflation to come down rapidly this year, raising expectations that the central bank could be nearing the end of its tightening cycle. Meanwhile, the British Pound failed to benefit from encouraging UK growth numbers. The Office for National Statistics (ONS) said Friday there was no growth in Gross Domestic Product during the fourth quarter of 2022. However, the economy dodged a second consecutive quarter of contraction, avoiding a technical recession.

On Friday, the University of Michigan's (UoM) Consumer Confidence Index came in at 66.4 in early February, up from 64.9 in January. Moreover, the year-ahead inflation expectations component rose to 4.2% from 3.9% and made it difficult for GBP/USD to gain traction ahead of the weekend.

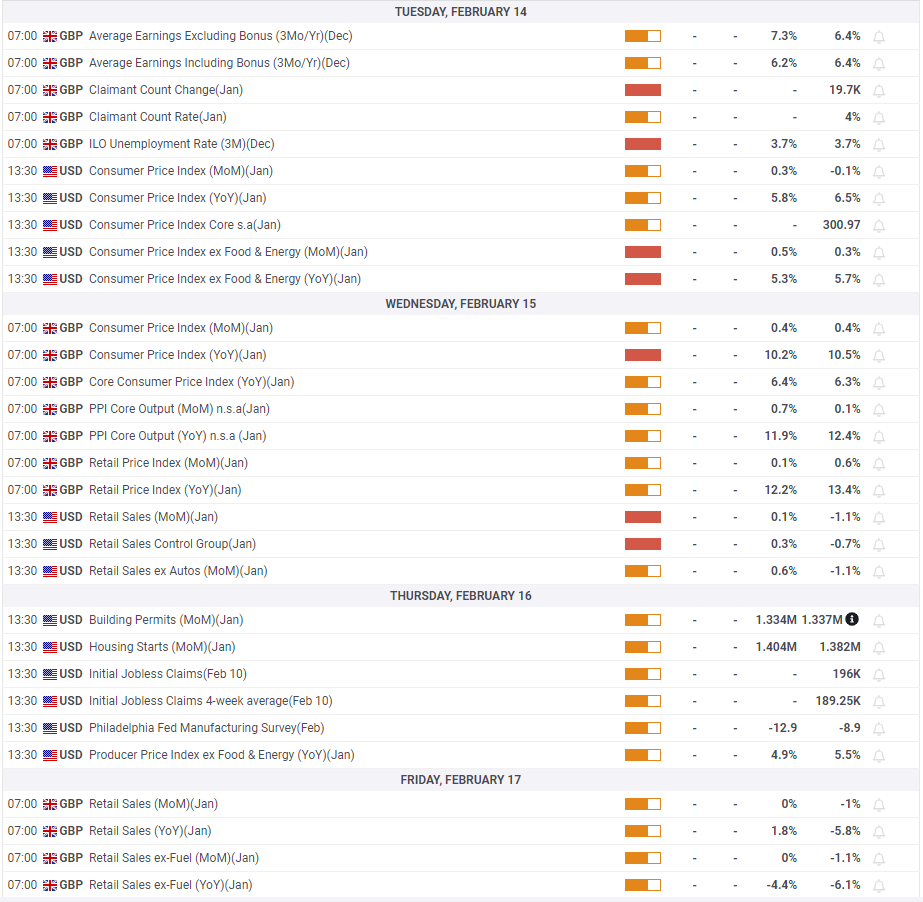

The week ahead: US/UK inflation in the spotlight

After a relatively data-light week, traders brace for a week dominated by high-impact data from both the United States and the United Kingdom. Monday lacks any significant economic data releases and therefore, Tuesday’s employment data from the United Kingdom will be eyed ahead of the all-important United States Consumer Price Index (CPI) data. The US CPI report will hold the key in providing significant insights into the Federal Reserve’s monetary policy outlook, as it is the most influential macroeconomic indicator to measure consumer inflation.

On an annualized basis, the CPI data is forecast to decline to 5.8% in January from December’s 6.5%. The Core CPI, which excludes volatile food and energy prices, is expected to edge lower to 5.3% from 5.7%. Meanwhile, the CPI is seen rising to 0.3% MoM vs. 0.1% previous. The Core CPI data is likely to edge higher to 0.5% when compared to the December reading of 0.4%.

Next on tap will be Wednesday’s UK CPI data, which softened to 10.5% YoY in December vs. 10.6% expected. A further deceleration in the UK inflation could strengthen expectations of a potential pause in the Bank of England’s (BoE) tightening cycle, which could weigh heavily on the Pound Sterling. The US will feature the monthly Retail Sales data, followed by the Industrial Production data and other minority reports on Wednesday.

The UK economic docket is devoid of any data on Thursday but the American traders will look forward to the Producer Price Index (PPI), weekly Jobless Claims and Housing data. On the final trading day of the week, the UK Consumer Spending data will be closely scrutinized for fresh trading impetus on the GBP/USD pair amid a lack of significant US macro news.

Aside from the data releases, speeches from the Bank of England and the Federal Reserve policymakers will drive the rate hike expectations, having a reasonable impact on the currency pair’s valuations.

GBP/USD: Technical outlook

Although GBP/USD managed to stage a rebound after testing the 200-day moving average (DMA) earlier in the week, the near-term technical outlook doesn't yet point to a buildup of bullish momentum. The Relative Strength Index (RSI) indicator on the daily chart stays below 50 and the pair continues to trade below the 50 and 20 DMAs.

In case the pair rises above 1.2200 (50 DMA) and starts using that level as support, it could continue to push higher toward 1.2300 (psychological level, 20 DMA) and target 1.2430 (end-point of the latest uptrend) afterward.

On the downside, 1.2000 (psychological level, static level) aligns as interim support before 1.1940 (200 DMA). A daily close below the latter could be seen as a significant bearish development and trigger an extended slide toward 1.1850 (100 DMA) and 1.1800 (Fibonacci 38.2% retracement of the latest uptrend).

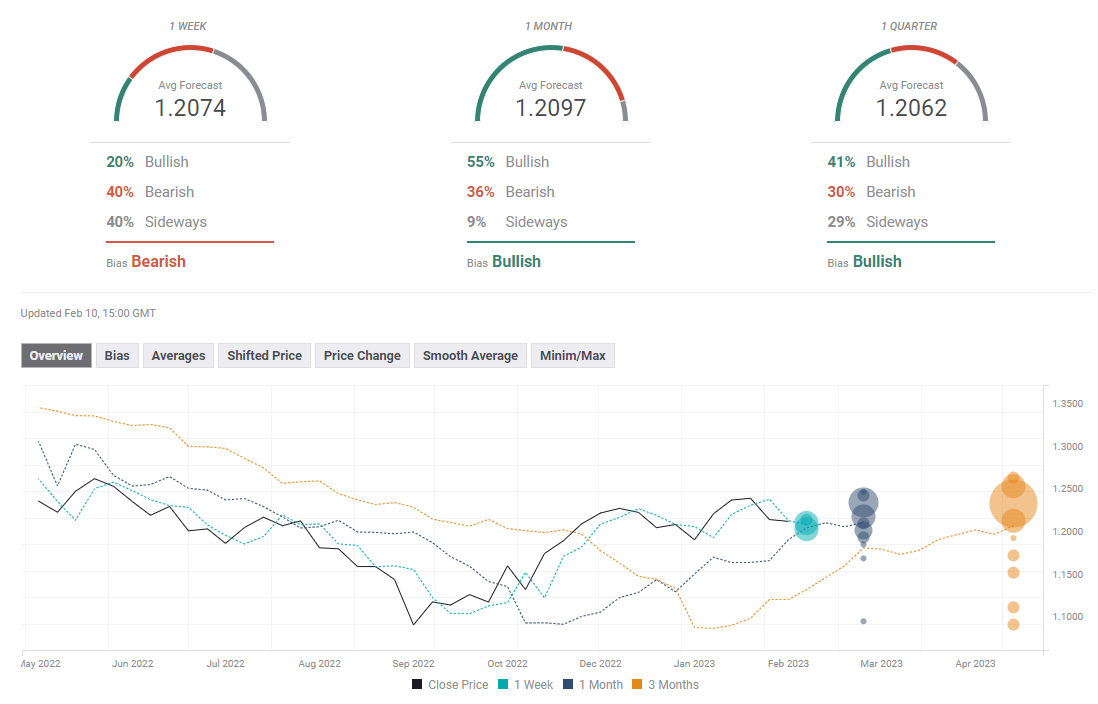

GBP/USD: Forecast poll

FXStreet Forecast Poll confirms the neutral/bearish bias in the short term with the one-week average target aligning at 1.2074. The one-month outlook remains slightly bullish with more than half of polled experts expecting the pair to rise at least to 1.2200 in that time frame.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.