GBP/USD Weekly Forecast: Brexit?! Sad, but true story for Sterling

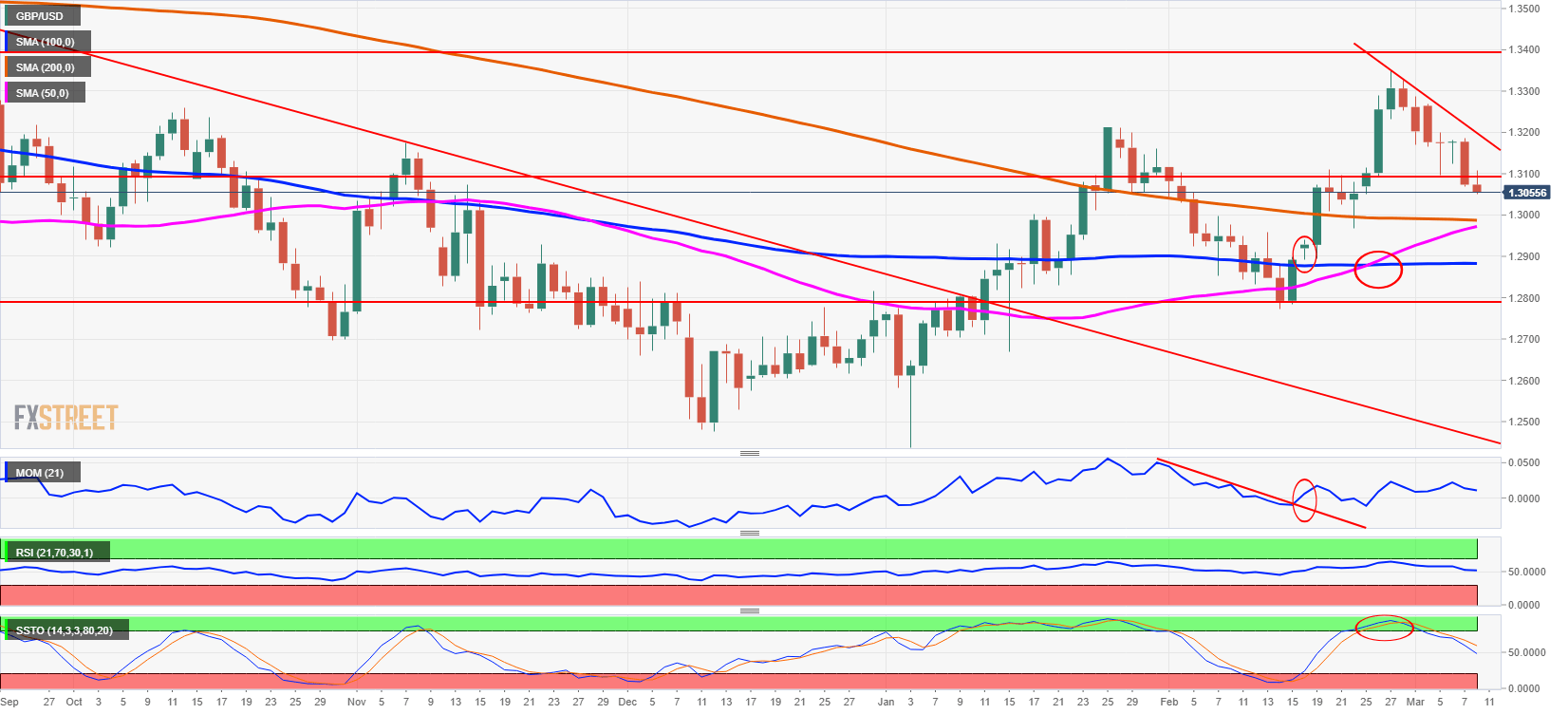

- The GBP/USD is set to close the first week of March 1.1% lower, breaking below 50% Fibonacci retracement support at 1.3090.

- The key macro event is scheduled for Tuesday, March 12 with the House of Commons set to vote on re-negotiated Brexit deal.

- The chances are rising for delayed Brexit to materialize should the smooth Brexit and no-deal Brexit scenarios fail to materialize.

- The FXStreet Forecast Poll reflects a greater amount of uncertainty ahead of UK House of Commons Brexit vote scheduled for next week.

The GBP/USD is trading down about 1.1% over the week on Friday after falling from Monday’s 1.3208 as low as 1.3051 over the week as Brexit uncertainty and the technical setup for a corrective move lower played its part during the first week of March.

Even with the US non-farm payroll report in February missing the market forecast with only 20K new jobs added in February, well off 180K expected, the GBP/USD remained capped below 1.3100 as the US wages rose by 3.4% over the year, slightly more than expected and the unemployment rate in the US dropped to 3.8%. Although the currency market reaction was rather muted the US interest rate futures showed the chances of Federal Reserve cutting the rates in 2019 increasing to 30% from 19% shortly before the February payrolls data with US Dollar negative implications.

The UK government is trying to re-negotiate the Brexit deal with the European Union in the last minute attempt to deliver the changes on the troubled issue of the Irish border backstop that saw members of House of Commons reject the original Withdrawal proposal in January in a stunning defeat for the government.

On the macroeconomic side, the UK construction PMI slumped to a contraction territory with the reading of 49.5 in February while services PMI saw the business activity increase to 51.3. The macro news had a marginal effect on the currency market with the Brexit negotiations conducted behind the closed doors and no major market moving announcements.

The US Dollar strength emerged after the European Central Bank decided on Thursday to launch further stimulus program with the third part of Targeted Long Term Refinancing Operations (TLTROs) while changing the forward guidance on rates saying it won’t change rates until the end of 2019.

The US Dollar rose as much as 1% against the Euro that fell to the lowest level since June 27, 2017, and the Dollar strength saw Sterling falling past 1.3090 representing a 50% Fibonacci retracement of the upmove from 1.1800 to a cyclical high of 1.4374.

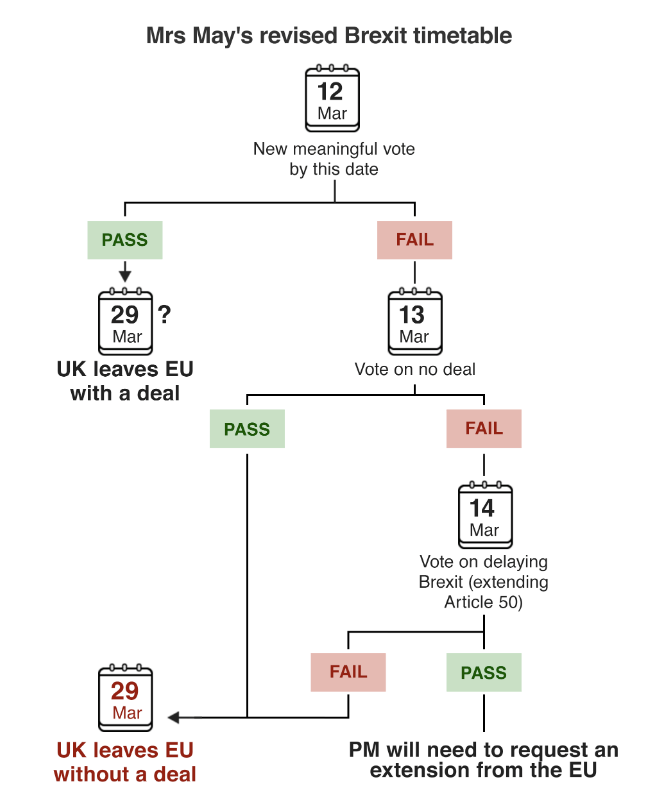

The Brexit re-negotiations are taking place in Brussels with the European Union said to make a new offer to the UK on Brexit backstop that is likely to fall short of the UK demands. With 21 days left before the UK is expected to officially depart from the European Union, the time is tight for any structural changes while the UK House of Commons is scheduled to vote on re-negotiated Brexit deal next Tuesday. While the UK parliament is unlikely to pass the re-negotiated Brexit deal, the chances for delayed Brexit increased in support for Sterling.

For the week ahead, the crucial Brexit deal vote is scheduled for Tuesday, March 12. Passing the Brexit deal opens up the road to scheduled departure of the UK from the European Union on March 29. In case of the UK House of Commons rejecting the deal, another vote on a no-deal Brexit will follow on Wednesday, March 13. Failure to accept a no-deal Brexit, which is the most likely scenario will see the House of Commons vote on delayed Brexit proposal on Thursday, March 14.

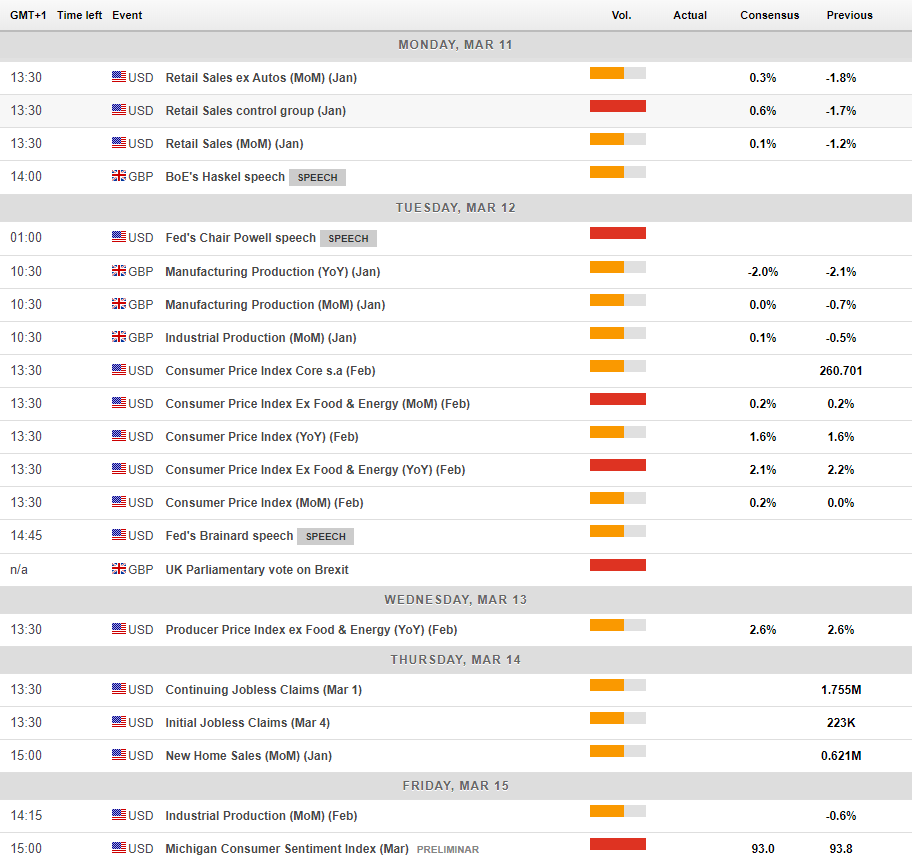

On the macro front, the UK manufacturing output due on the day of the Brexit vote next week is expected to play the minor role and the US retail sales and inflation data are also unlikely to drive the currency markets more than the Brexit deal vote itself.

On the other side of the Atlantic, the US February non-farm payroll missed the market estimate big-time rising only by 20K compared to the expectations of 180K, while wages increased slightly above expectations by 3.4% y/y and the unemployment rate dropped to 3.8%.

While scenarios of approving the Brexit deal is GBP/USD supportive, a no-deal Brexit scenario might become a nightmare for Sterling. After 2-years of Brexit chaos, with days remaining before the official departure of the UK from the EU, nobody really knows what sort of Brexit will finally become reality. That’s sad, but true.

As the Bank of England Monetary Policy Committee member Silvana Tenrayro indicated in her speech on Thursday, the disorderly Brexit is more likely to require loosening of monetary policy than tightening while Sterling would likely appreciate after a smooth Brexit, which would limit inflation pressure.

The US Federal Reserve and the Bank of England officials speaking

New York Fed President John Williams said in a speech at the Economic Club of New York on March 6:

- "Slower growth isn’t necessarily cause for alarm" but instead a "new normal" we should expect.

- From a monetary policy perspective, the US economy is about as good as it gets.

- Fed can afford to be flexible and wait for data to guide our approach.

- I expect the growth to slow to about 2% this year.

- The outlook in Europe and China has become less bright, with a downgrade to European outlook "notable".

- Tightening of financial conditions in 2018 will restrain consumer, business spending in 2019.

- The US economy has a strong labor market, moderate growth, no sign of significant inflation pressure.

- My view is we’re not seeing signs of the scarcity of reserves needed to conduct monetary policy.

- There is no clear answer on the level of reserves Fed will need to conduct monetary policy.

- Interest rates are right where they need to be.

- Inflation risks don't seem to be out there at all right now.

- I don't have a particular lean on where rates should go.

- In a downturn, we could consider quantitative easing, negative rates with cost-benefit tradeoffs of negative rates not as favorable as quantitative easing.

The Bank of England Monetary Policy Committee member Michael Saunders said on March 6:

- It is possible that monetary tightening might be needed in the future, but does not mean we need to tighten now.

- It makes sense to wait and see how Brexit unfolds.

- The UK inflation "reasonably well behaved", growth not strong enough now to create excess demand.

- The policy response to Brexit is not automatic, could be in either direction.

- Effect of the latest BoE rate hikes on households seems much smaller than usual.

- Weaker impact of recent rate rises suggests BOE may need to be more forceful when tightening or loosening policy in the future.

- The link between the Bank rate and changes in household finances less effective when the Bank rate is low.

- Negative interest rates do not really work, quantitative easing offers more scope.

- Gradual tightening does not mean it will be fantastically slow.

- The output gap is closing so policy should not be as loose as has been when we get out of Brexit risk.

- The UK households would probably go back to recent trend if Brexit deadline extended by a couple of years.

- I am agnostic about the direction of monetary policy after a no-deal Brexit.

- I am certain that monetary policy could not prevent a no-deal Brexit from damaging UK economy.

The New York Federal Reserve Vice President Simon Potter said on March 7:

- There is little academic analysis to quantify the effect of FED mortgage purchases on other bonds, stocks.

- There is a little experience to draw on as Fed reverses asset purchases.

- Many might argue that agency Mortgage Backed Securities (MBS) issuers gained benefits at taxpayers’ expense.

- Some agency MBS reinvestment purchases May be needed in the future.

- There is more to learn about selling agency MBS prior to any decision to start doing so.

- MBS purchases provided clear benefits to the economy.

The Federal Reserve Governor and the voting member of the rate-setting FOMC Lael Brainard said at Princeton University, in New Jersey on March 7:

- Increase in risks warrants a downward revision in rate path.

- Policy goal now is to preserve progress made on maximum employment, target inflation.

- The best way to safeguard gains is to navigate cautiously on rates.

- The downside risks to output, employment argue for softer rate path even if economic outlook stays the same.

- The demand appears to have softened against the backdrop of greater downside risks.

- "Prudence counsels a period of watchful waiting," especially with no signs of inflation pickup.

- The economy might warrant a softening in the Fed's policy path.

- With balance sheet normalization well advanced, should wind down redemptions later this year.

- I would not want to cut rates and shrink the balance sheet at the same time.

- The inflation trends may be below the Committee's objective.

- We should be equally attentive to the risk of downside erosion in inflation expectations.

- Trade disputes, Brexit, US government debt ceiling among risks to forecast.

- Fed policymakers are carefully monitoring leveraged loans, bonds vulnerable to downgrade and funds that hold those assets.

- It is clear that the potential US economic growth rate is lower than before.

- I do not want to prejudge what kind of rate moves would be appropriate late in the year.

- The active movement from mortgage-backed securities to treasuries on the Fed balance sheet is not a short-term consideration.

- Fed policymakers should look at temporary price level targeting and other proposals on the inflation target.

- Fed will not be done addressing larger inflation framework review until late this year or beyond.

The Bank of England Monetary Policy Committee member Silvana Tenreyro said on March 7:

- Disorderly Brexit is more likely to require loosening of monetary policy than tightening.

- It is easy to envisage other scenarios requiring the opposite response.

- Sterling would likely appreciate after a smooth Brexit, which would limit inflation pressure.

- We will need a small amount of tightening over the next 3 years after smooth Brexit.

- Before voting for rate hikes, need to be confident of demand growing faster than supply, an increase in domestic inflation pressure.

- Trade tensions and the US tariffs on China are the biggest drivers of the global slowdown.

Brexit vote scenarios

Related story

Technical analysis

GBP/USD daily chart

Technically the GBP/USD broke below 50% Fibonacci retracement line at 1.3090 and the currency pair is tilted to the downside. The technical oscillators including Momentum and the Relative strength index are flattening out while Slow Stochastics made a bearish crossover within the Overbought territory and it is sliding lower. The most important technical feature though is the golden cross of the 50-day moving average crossing over the 100-day moving average (DMA). The golden cross is a strongly bullish technical signal that is expected to push Sterling higher long-term. In the short-term, the GBP/USD though is in corrective mode around 1.3090 before re-testing 1.3050 and a strong psychological support level of 1.3000.

On the upside, the GBP/USD needs to close above 1.3090 representing 50% Fibonacci retracement of post-Brexit recovery from 1.1800 to 1.4374 before targeting 1.3390 representing 61.8% Fibonacci retracement of the same upmove.

The economic calendar ahead

From the currency market perspective, the most important event scheduled for the GBP/USD is Tuesday’s vote on Brexit deal. Should the UK parliament fail to approve the re-negotiated Brexit deal on Tuesday, the votes on no-deal Brexit on Wednesday and a delayed Brexit on Thursday are to follow.

In the US, the February labor market report is expected to dent the US Dollar strength in the upcoming week although data on the US retail sales and the US inflation are expected to dominate the agenda together with the Federal Reserve’s chairman speech on Tuesday.

The US and the UK economic calendar for March 11-15

FXStreet Forecast Poll

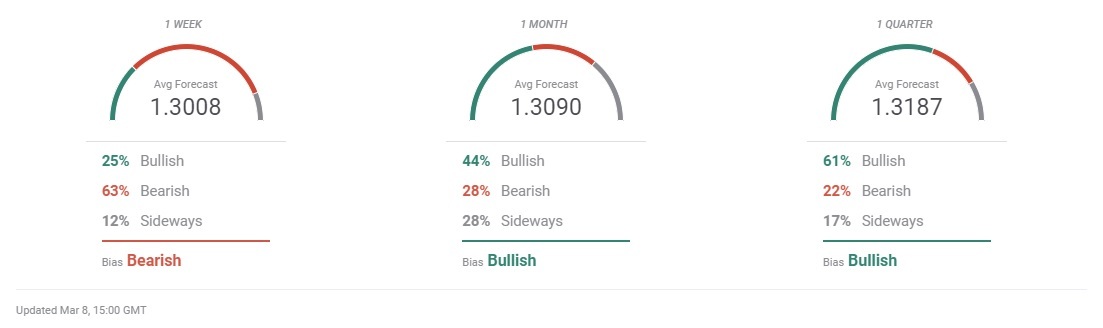

The short-term FXStreet Forecast Poll for GBP/USD turned bearish expecting 1.3008 in one week time from now, down from a sideways of 1.3268 last week and 1.3024 forecast two weeks ago. The forecast remains strongly bearish with a bullish-to-bearish ratio at 25%-63% down from 36%-43% one week ago.

For 1-month ahead, the forecast turned bullish thanks to the trend of falling GBP/USD with the forecast of 1.3090, down from 1.3150 FX rate predicted last week. Bullish-to-bearish forecast is 44%-28% and 28% of sideways predictions.

The vast majority of the forecasters in the FXStreet Forecast Poll is bullish over the 3-months horizon with GBP/USD prediction moving further up to 1.3187, down from 1.3256 last week and up from 1.3118 predicted two weeks ago. The bullish-to-bearish ration rose to 61%-22%, up from 51%-42% forecasts last week.

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.