G20 eases stance on protectionism, USD tumbles

Forex News and Events

USD sell-off ahead of busy week for Fed members (by Arnaud Masset)

The USD started the week on the back foot against the backdrop of easing US yields and growing investor impatience over Trump’s tax cut and fiscal stimulus reforms. High-yielding currencies were buoyed this morning as the low volatility environment encouraged investors to load on risk. In the G10 complex, the Aussie and the Kiwi were the best performers, rising 0.44% and 0.63% respectively. The Japanese yen consolidated last week’s gains but did not rise further as market participants resumed the “hunt for yield”.

The single currency continues to gain ground despite the uncertainty stemming from ongoing French elections. It seems now that the market is already pricing in a defeat from Marine Le Pen or at least indicating that it will not jeopardise the future of the eurozone. The spread between German and French two-year yields continues to narrow. After reaching 0.45%, the spread narrowed to 0.33% as German yields recovered.

After an uneventful G20 meeting in Baden-Baden, investors will have limited data to sink their teeth into. Otherwise, it will be a relatively light week, with the exception of a few speeches from Fed members, which could potentially create some waves in the FX market. We expect the USD sell-off to take a breather in the short term; however further down the road, we are not ruling out further dollar weakness as patience grows thin over Trump’s promised economic boost.

G20 stumbles, China will be the long term beneficiary (by Peter Rosenstreich)

The stakes on risk to global trade have risen on the back of the G20’s failure to reject rising protectionism. In a surprise twist, the G20 published a communiqué removing the wording: “resist all forms of protectionism” - highlighting the diverse group's ineffectiveness to work together to form a compromise. In a complete role reversal, US Secretary Mnuchin refused to cull protectionism, while China's President Xi was vocal in supporting free trade. The compromised statements included commitment to “strengthening the contribution of trade to our economies”. The effect on markets was muted however, the risk of destabilising US trade policy has increased. Trump’s administration has been preoccupied with domestic policy failures, forcing international issues to the side. US Secretary of State Tillerson was in China to ease bilateral tensions. However, key issues such as North Korea, FX policy concerns and trade were not discussed.

Trump's next move on currency & trade policy is anyone’s guess. Instead of delivering on his campaign promise to label China a currency manipulator and slap a massive tariff on Chinese’s imports from “day one”, Trump has only targeted China for cheap political points. We suspect that Trump is bluffing in regards to an aggressive Chinese policy, yet the risk of radical unilateral action cannot be ruled out. In the long run, we suspect that the biggest gainer from Trump's non-traditional actions (unstable political partner & withdrawal from Trans-Pacific Partnership etc ) will be China, gaining total dominance in the Asian region. In this regard, we continue to value China assets. USDCNY remains stable around 6.90, on a slightly weaker fix at 6.89.

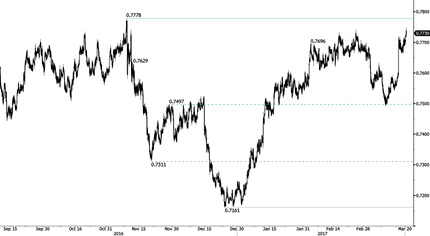

AUDUSD - Key resistance at 0.7778.

The Risk Today

Peter Rosenstreich

EUR/USD is challenging the resistance implied by its rising trendline (around 1.0795). A break of upside would signal persistent buying pressures. Key resistance is still given at a distance 1.0874 (08/12/2017 high). Strong support can be found at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD has successfully tested the support at 1.2110 and continues to bounce higher. A break of key resistance (at 1.2429) is needed to open the way for further strength. Yet, the pair remains in a clear downtrend suggesting short term correction. Key resistance can be located at 1.2570 (24/02/2017 high). Hourly support is at 1.2324 (03/17/2017 low). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY has failed to break key resistance given at 115.62 (19/01/2016 high confirming persistent selling pressure. The pair remains stuck in sideways trading pattern between 111.36 and 115.62. Hourly support given at 112.47 (nitraday low). Hourly resistance can be located at 113.57 (16/03/2017 high). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF has paused after sharp exit from uptrend channel. Hourly support is given at 0.9862 (31/01/2017 low) has been broken. Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to consolidate. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

Resistance and Support:

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.0652 | 121.69 |

| 1.0954 | 1.3121 | 1.0344 | 118.66 |

| 1.0874 | 1.2771 | 1.0171 | 115.62 |

| 1.0760 | 1.2422 | 0.9979 | 112.75 |

| 1.0454 | 1.1986 | 0.9862 | 111.36 |

| 1.0341 | 1.1841 | 0.9550 | 106.04 |

| 1.0000 | 1.0520 | 0.9444 | 101.20 |

Author

Arnaud Masset

Swissquote Bank Ltd

Arnaud Masset is a Market Analyst at Swissquote Bank. He has a strong technical background and also works in the development of quantitative trading strategies.