Forex: Trump, the 'Deal Maker in Chief'? – Polymarket points to a 56% chance of tariffs on China

Today marks the inauguration of Donald Trump as the 47th President of the United States, casting a dramatic spotlight not only on his anticipated directives about immigration and a national energy emergency but also on potential seismic shifts in trade policies. The financial markets, particularly the FX markets, are on tenterhooks, keenly anticipating his pronouncements on tariffs, which could impose significant strains on major U.S. trade partners. In the recent nomination hearings, Scott Bessent, the incoming Treasury Secretary, underscored the necessity of tariffs to rectify unfair trade practices, augment government revenue, and act as a potent lever in trade negotiations.

The US dollar has softened as the week starts, a shift that coincides with a renewed sense of optimism following reportedly encouraging discussions between President-elect Donald Trump and Chinese President Xi Jinping. A recent Chinese announcement underscored a mutual commitment to fortify Sino-US relations. The diplomatic activity intensified over the weekend as Chinese Vice-President Han Zheng engaged in pivotal talks in Washington with US Vice-President-elect J.D. Vance and tech titan Elon Musk, laying the groundwork for Trump's inauguration today. This series of high-level engagements has eased the dollar's ascent, hinting at a more harmonious path forward for US-China relations, which reverberates through the dynamics of the global currency markets.

However, it's important to note that the dollar has already lost its vigorous momentum, primarily due to movements in the US Treasury market. After peaking at 4.81% earlier last week, the 10-year US Treasury yield has since retreated by over 20 basis points. This shift followed the release of December's CPI and PPI data, underscoring a continuing slowdown in underlying US inflation, just as Trump gears up for his second term. This development prompts reevaluating recent market fears regarding long-term inflation risks, driving a significant sell-off in global bond markets.

If the bilateral trade negotiations truly held substantial promise, one would expect to see a much softer dollar as a result. However, the market may still be skeptical about their potential success or impact, reflecting a cautious sentiment despite these apparent friendly discussions.

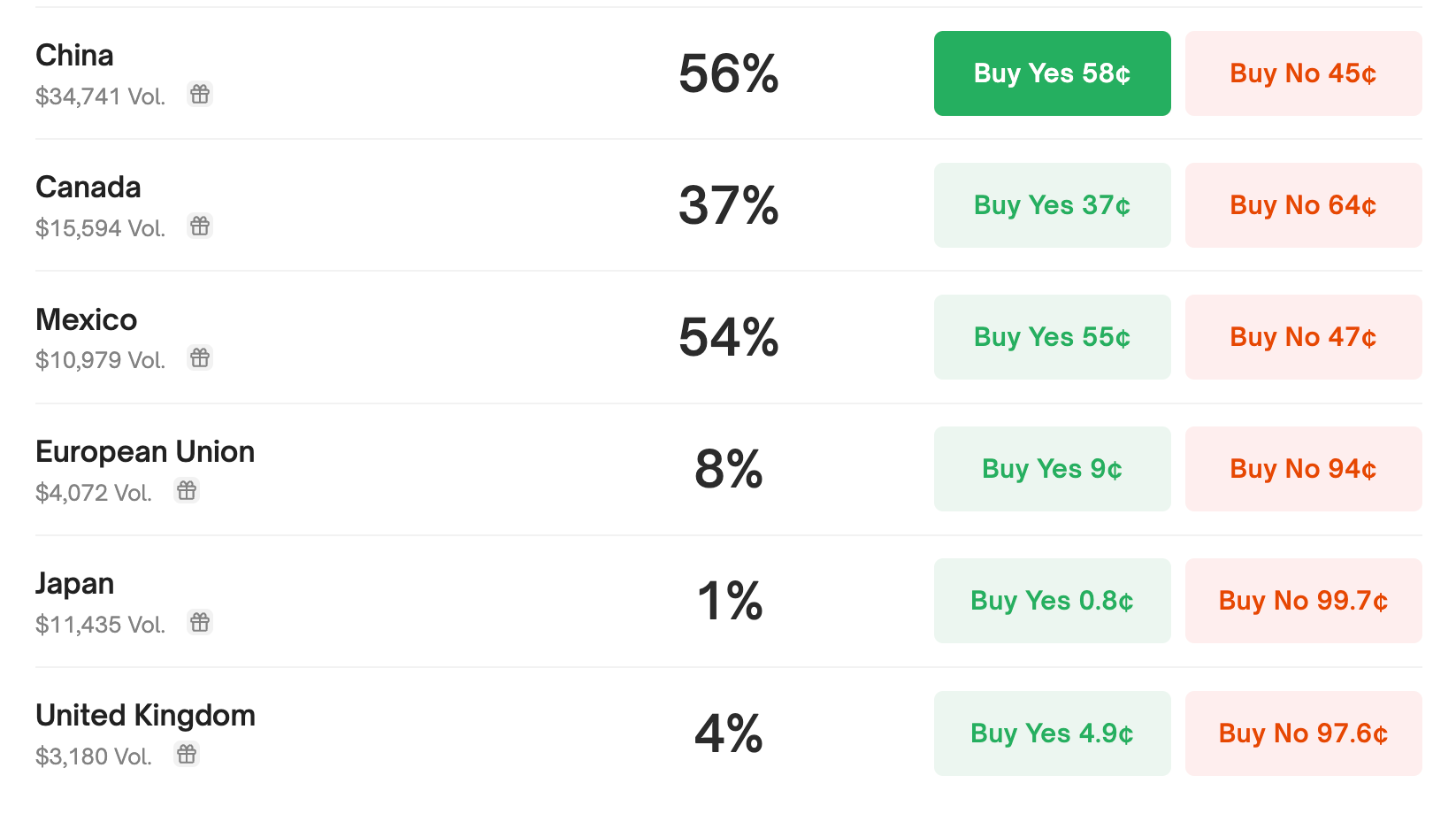

Market participants closely monitor betting platforms like Polymarket and Kalshi to gauge the probability of tariff impositions in Trump's first week. Current forecasts peg a 56% probability for China, 54% for Mexico, 45% for Canada, and a mere 8% for the European Union.

Polymarket

Tarrif's posture has fueled a nearly 10% rally in the dollar since late September, positioning it just shy of its recent zenith.

Yet, the merest hint that Trump might favour a more tempered tariff approach could prompt a corrective slide in the dollar, setting the stage for a recalibration of market expectations that could unfold over a more extended period.

However, suppose tariffs are implemented swiftly and extensively. In that case, the Eurozone and the Euro should brace for impact, especially considering the betting markets have pegged the likelihood of EU tariffs at a mere 8%. This contrasts starkly with remarks by Isabel Schnabel of the European Central Bank over the weekend, who suggested that an EU trade conflict under the new U.S. administration is "very likely." Such statements from a key ECB figure highlight the potential severity and immediacy of trade tensions, underscoring the precarious position of the Euro in the face of impending U.S. policy shifts.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.