FOMC: Prelude to a rate cut?

- FOMC voted 9-1 to keep the fed funds rate at 2.25% to 2.50%

- The Fed removed “patient” from its policy timing

- Dot plot for rates unchanged at 2.4% this year, drops 0.5% to 2.1% in 2020

The Federal Reserve added little new to its policy prescript in Wednesday’s FOMC statement and economic projections and with the anticipation for a July rate cut long priced into market levels the reaction was decidedly uninvolved.

The FOMC statement changed its wording on future policy changes from “patient” which had been the guidance since January to ‘closely monitor the implications of incoming information” and added a specific reference to “act as appropriate sustain the expansion. “

The Projection Materials offered some mild tweaks to the governors’ economic assessments since the last issue in March.

Gross domestic product remained at 2.1% this year—currently it is tracking at 2.55%--and rises 0.1% to 2.0% in 2020. Core PCE inflation fell to 1.8% this year from 2.00% and next year to 1.9% from 2.0%. The projected fed funds rate in December remained at 2.4% but in 2020 it drops to 2.1% only to climb back to 2.4% in 2012.

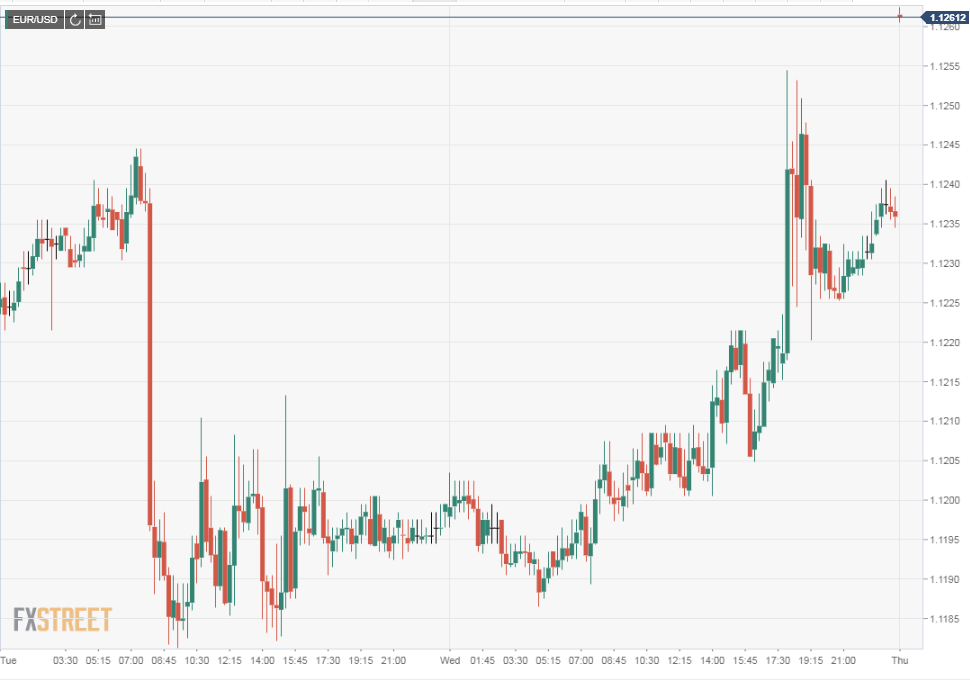

The dollar initially fell sharply losing almost 40 points against the euro to 1.1255, slightly less versus the yen and the sterling. But by the close in New York the currencies retained only about half of their original advantage.

The rate outlook for this year and next, no cuts this year and perhaps two the following would seem to be at odds with market expectations.

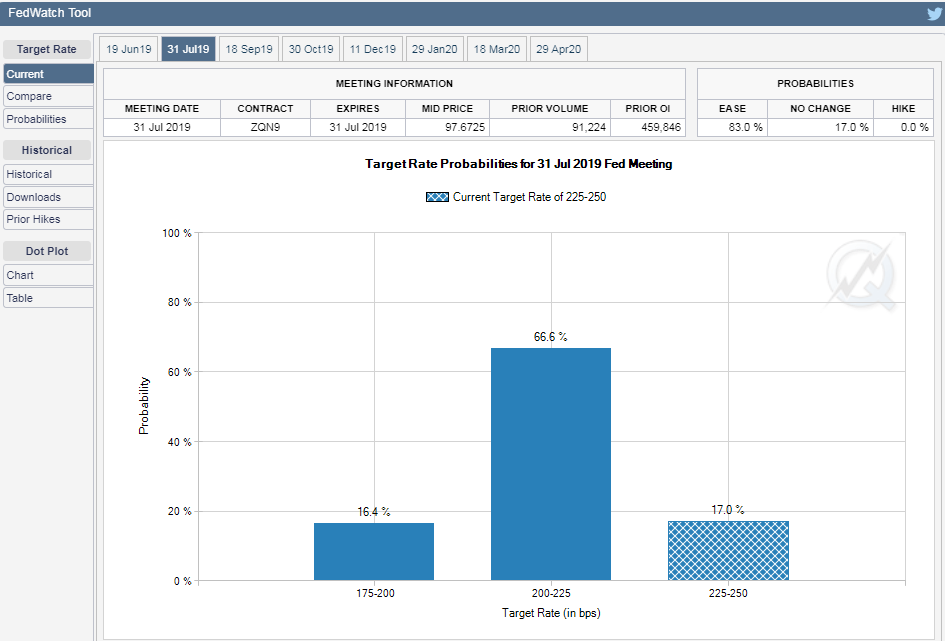

Before the FOMC release the fed funds futures had the potential for a 25 basis point cut by the July 31st meeting at 83%.

CME Group

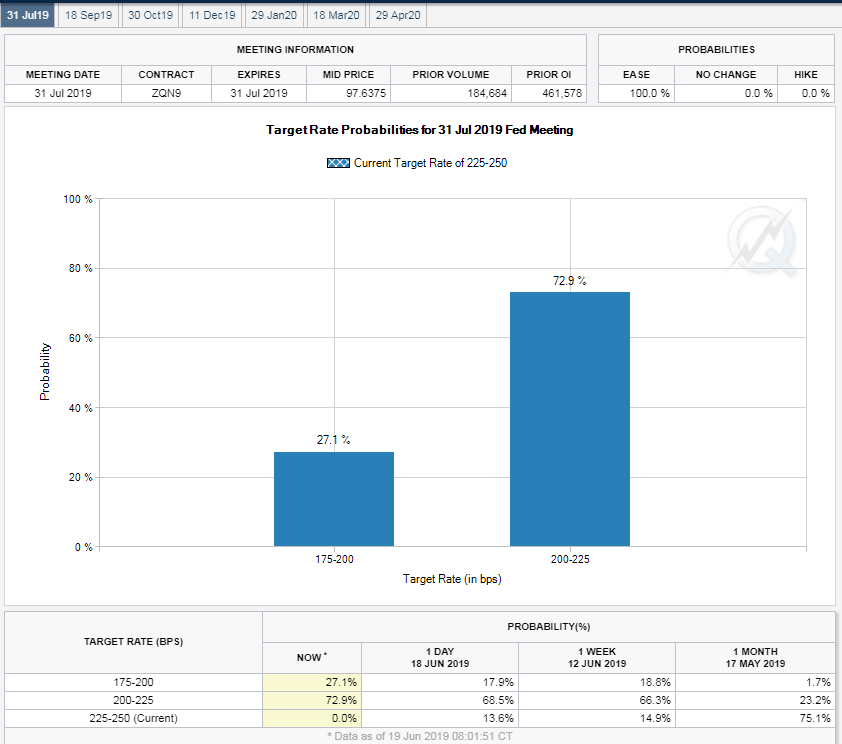

After the statement and Chairman Powell’s news conference the figure was 100%, 71.9% for a target range of 2.00%-2.25% and 29.1% for 1.75% to 2.00%. That is a high chance of one cut less for two but zero chance for none.

CME Group

Treasury yields seconded the futures judgement. The return on the 2-year generic Treasury fell 13 points on Wednesday to 1.74% the lowest this benchmark rate has been since late last November. The yield on the 10-year generic slipped 1 point to 2.02%.

Reuters

Interest rates on Treasuries have been falling since early November last year. By December 18th the day before the FOMC’s last 0.25% hike to a 2.5% upper target the 2-year yield had already fallen 32 basis points from its peak to 2.56%.

The difference between the market expectations for a rate cut in July and Fed reticence is not a large as it seems.

“The case for somewhat more accommodative policy has strengthened,” said Mr. Powell. As the FOMC statement put it “uncertainties about this outlook have increased.”

The Fed is waiting for a deterioration in the hard economic numbers before it moves. The credit market assumes that will happen. In the end it is far easier for the markets to reverse an erroneous judgement than it is for the central bank.

Interest rate projections, the dot plots of the individual members’ expectations, showed that eight of 17 officials predict one 25 basis point cut this year, eight favor the current rate targets and one member wants a rate increase.

In his news conference following the rate announcement Chairman Powell repeatedly mentioned the state of the US economy which he described as good and the potential for the a change in the months ahead. “We are monitoring the [global] cross-currents and see if they weigh on the outlook.”

"Some of the [negative] developments are recent and we want to see if they will sustain...The [US] base line scenario is a good one. Job creation is still well above entry levels to the work force,” he said. “I don’t think the risk of waiting too long [to cut rates] is prominent right now.”

The US-China trade dispute is one of the considerations that the Fed is monitoring.

“News about trade has been an important driver of sentiment in the intermediate period,” commented Mr. Powell after noting that the US statistics that have shown the greatest amount of weakness in the past months have been the sentiment indicators.

The Fed it seems, is willing to keep the possibility of a trade deal and its potential galvanizing impact on the US economy alive.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.