Federal Reserve January 28-29 Meeting Preview: Stable policy and an uncertain future

- Steady rate policy expected at first meeting of 2020.

- US economy and Fed forecasts foresee little change.

- Economic impact of trade and China virus may be a topics for Chairman Powell.

The Federal Reserve will finish its scheduled two day policy meeting of the Federal Reserve Open Market Committee (FOMC) on Wednesday January 29. The central bank will announce its decision for the fed funds rate at 2:00 pm EDT, 18:00 GMT. Chairman Jerome Powell will read his statement and hold a news conference beginning at 2:30 pm EDT, 18:30 GMT

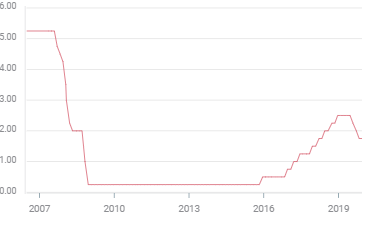

Fed Funds Rate

Federal Reserve policy and the US economy

The course of the American economy has not altered since the previous FOMC meeting on December 10-11 last year.

Fourth quarter growth is expected to be 2.1% when the preliminary figures are released by the Bureau of Economic Analysis on Thursday, hardly a stir from the 2.0% and 2.1% rates in the second and third quarters.

If job creation slipped in the final month of 2019 to 145,000 from 256,000 in November, and the monthly average for the year of 176,000 is down from 235,000 in January they are still well above the 125,000 -150,000 new entrants to the labor market each month and these numbers come at the end of an exceptional three years for the US labor market. The six month average of 189,000 is remarkable for an economy the 11th year of expansion.

Wages remain buoyant as would be expected with a record 3.5% unemployment. The December annual gain of 2.9% was the first month without at least a 3% increase in 15. Manufacturing work, hurt by the US-China trade dispute, fell precipitously in 2019 to 46,000 hires from 264,000 the prior year but there is hope for reversal with the new trade agreement.

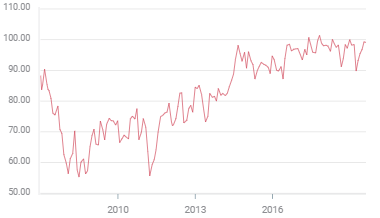

Consumer sentiment is strong. The Michigan and Conference Board surveys are at the higher end of their ranges of the last three years, which are themselves among the best on record.

Michigan Consumer Sentiment

FXStreet

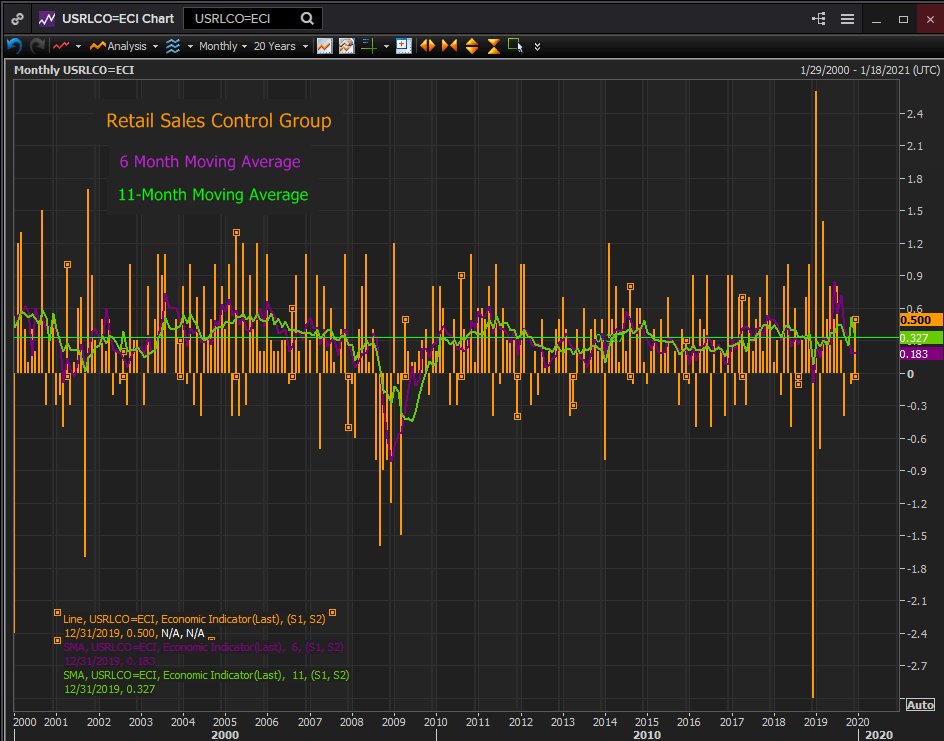

Consumption is healthy. The retail sales control group, the Bureau of Economic Analysis consumer spending component rose 0.5% in December and its 11-month average of 0.327% is about mid-range for the last 3 years*.

Reuters

Business confidence in the 70% of the economy comprising the service sector is serviceable if down from its record levels in late 2018 and early 2019. It is commensurate with a 2% growth rate.

Core PCE inflation was 1.6% on the year in November and is expected to remain there in January. Though it is below the Fed's 2% target and has been so since last January the differential is not large enough to be a policy concern.

The twin but related problems for the economy are the sharp decline in job creation in the manufacturing industries and the near cessation of business investment. The source of both has been the fear of a global trade war, which even if unlikely, was sufficient to make factory managers and planners opt for caution. The revival of manufacturing and investment awaits the success of the trade deal.

For the Fed governors and rate policy the chief point is that the trends and performance in the US economy remain unmoved from six weeks ago. There has been no deterioration in the labor market. Initial jobless claims have returned to near their five decade lows after elevating in December. Consumer spending and attitudes are good and promise to remain so as long as wages and jobs are plentiful.

The labor economy that was the object of the Fed’s three summer and fall rate cuts has kept its footing and can only improve as the trade agreement with the mainland takes effect.

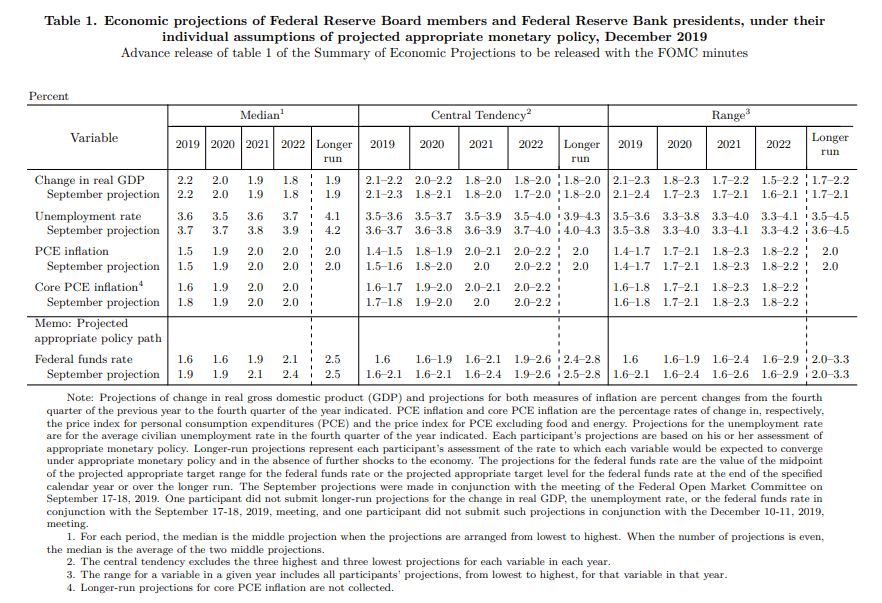

Federal Reserve economic projections

The economic predictions that closed out 2019 are likely to be among the bank’s most accurate in some time. Growth was expected at 2.2% and if the Atlanta Fed GDPNow estimate for the fourth quarter of 1.9% is accurate last year’s expansion will be 2.275%.

Of more interest for the market is the stationary fed funds projection at its1.6% mid-point through the end of the year. At the moment, and for the past month and a half, there is nothing in the US economy that would elicit a change.

Federal Reserve Projection Materials

Conclusion

With rate policy a foregone event market interest will focus on the economic outlook for the first half of the year and its two outstanding questions, the impact and timing of the trade deal and the burgeoning effect of the Coronavirus on the Chinese economy and by default the US and the rest of the globe.

For the first Chairman Powell will offer informed anticipation that it will achieve its goals and that China’s agricultural purchases and export orders will enliven if not totally revive both sectors. Positive economic opinions from Chairman Powell will accrue to the US dollar.

The effect of the health crisis on the mainland and the world economy depends on the still unknown severity and longevity of the illness. On that Chairman Powell may be better informed about the present but will have little more read on the future than the rest of us.

*Because of the partial federal government shutdown in January 2019 retail sales figures were delayed. December was reported as -3%, an unheard of figure for the holiday season and January came in at 2.6%, with many of the misplaced sales from December recored late. A 12-month moving average in December 2019 includes the January figure but not the December providing a false image of the year.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.