Risk of Yen intervention lurks during holiday trading period

- Verbal intervention puts a halt to Yen’s freefall

- But risk of FX intervention is elevated as dollar remains supported

- Will Japan take action during holiday-thin trading?

A roller-coaster ride

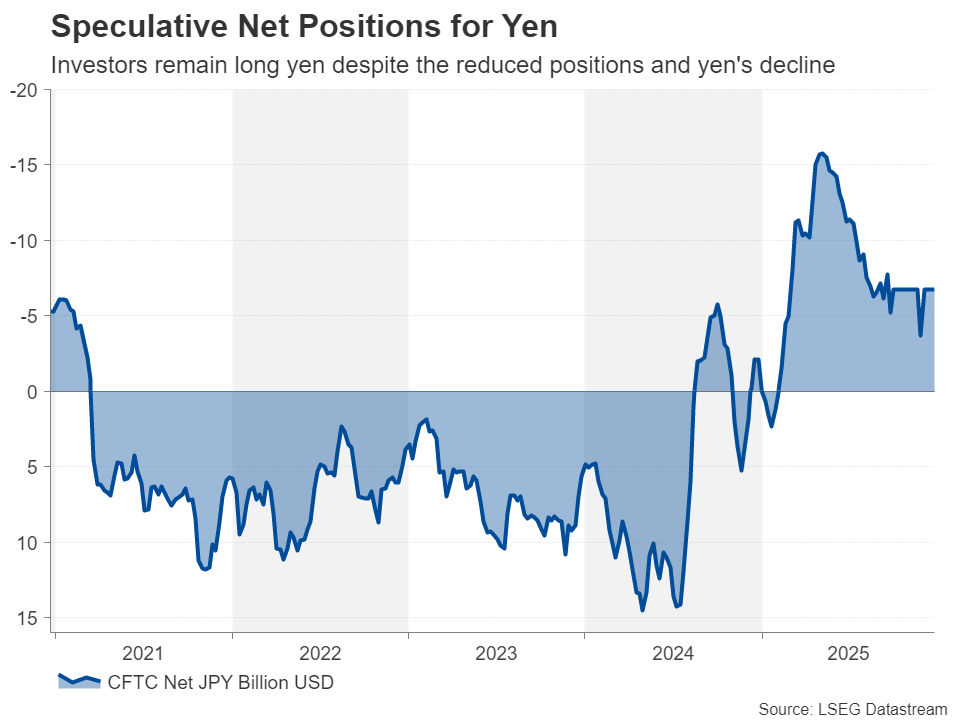

After a bullish start to the year, the yen has now almost erased all its gains from the first four months of 2025 and looks set to end close to where it started – stubbornly stuck in the 154.00-158.00 range. Two 25-bps rate hikes during the year have not had the desired effect of placing the yen on a sustained uptrend, even as net long positions have been positive for most of the year.

Investors have been disappointed by the lack of clarity over the rate-hike path by the Bank of Japan, as the overly cautious approach to policy normalization has left the yen at the mercy of speculators. To be fair, the trade war and political instability at home were not foreseen at the beginning of the year, although neither were they completely unexpected.

Rate hike obstacles

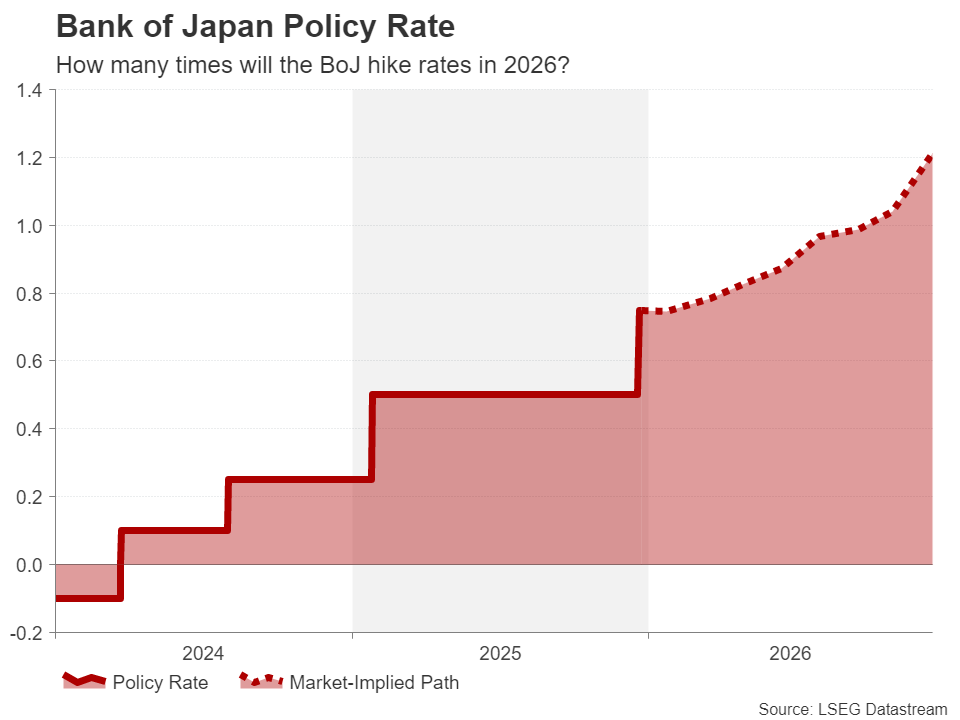

Nevertheless, the change in government and higher tariffs on exports to the US were significant headwinds for the Japanese economy and subsequently for the BoJ’s rate-hike agenda. But with both of those risks now having subsided, BoJ policymakers are feeling more confident about raising interest rates further over the coming year.

Investors have priced in almost two rate rises for 2026, which would take the policy rate to 1.25%. But there is talk that the BoJ is aiming for rates to reach at least 1.5%, so a further hawkish tilt next year is possible.

Doubts about rate-hike path

So why isn’t the yen heeding the hawkish soundbites? It’s likely that after the multiple disappointments about the BoJ’s approach to rate increases, many investors are holding onto their view of “I’ll believe it when I see it”. But there are other factors too.

Japan’s economy is seen as too exposed to global economic or geopolitical risks, particularly anything that could harm US growth. In essence, rate hikes could easily become derailed again, hence why investors are not holding their breath about any aggressive tightening, especially as the new government of Sanae Takaichi is opposed to this.

Weak Yen is a problem for the government

However, Takaichi has softened her stance to rate hikes following the yen’s recent bout of weakness and is unlikely to stand in the way of the BoJ if it means lending support to the currency. But perhaps more importantly, it is the worries about Japan’s mounting debt why markets are not convinced that the BoJ will be able to go very far with its tightening plans.

When adding to the equation the receding expectations of steep rate cuts by the Federal Reserve, amid a very resilient economy, the prospect of US-Japanese yield spreads narrowing substantially over the next year or two isn’t looking too great.

Policy divergence is front and center

This could change of course if Japanese data, particularly the CPI readings, surprise to the upside in 2026, and US economic indicators disappoint. A slowdown in the US economy, led by a deteriorating labour market, cannot be ruled out, despite recent data suggesting that jobs growth is already recovering.

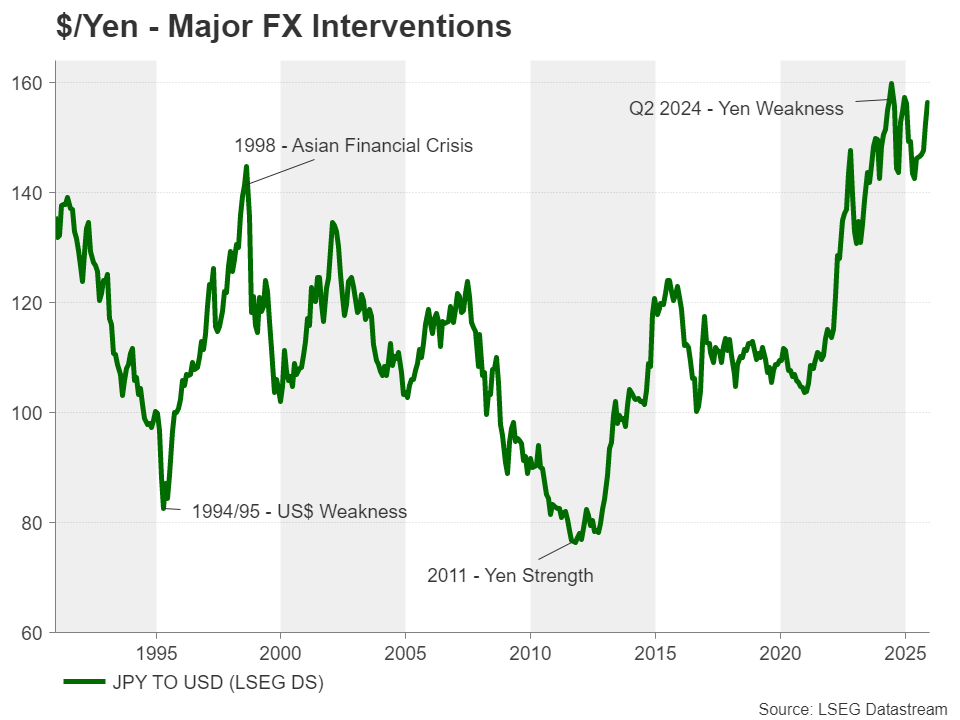

But in the meantime, the only thing preventing the yen from sliding further is the threat of intervention by Japanese authorities. The language from Japanese officials, including the country’s top currency diplomat and the finance minister, has been getting stronger in recent days. The sternest warning came on Monday when Finance Minister Satsuki Katayama said she has a “free hand” to take “bold action” against such moves.

Thin liquidity is a volatility risk for Dollar/Yen

However, speculators may decide to take advantage of the low liquidity days during the Christmas and New Year holiday period when many traders will be away from their desks and trading will be extremely thin. Any attempt to drive the US dollar beyond 158.00 yen – a level that tends to put Japanese officials on alert – could be met by intervention.

Any breach would likely see dollar/yen’s advance slow as it approaches 160.00. But given that authorities intervened twice in 2024 when this level was violated, fresh action is almost certain should this recur.

In the event of direct intervention in the exchange rate, dollar/yen could tumble below its 50-day simple moving average (SMA) at 154.72, potentially triggering a broader selloff, which would then push the pair towards the 153.00 area.

Summing up, a lot is riding on the US dollar maintaining its broader downtrend during the last few remaining trading days of 2025. Anything that spurs a bounce back in the dollar could threaten the yen’s own rebound, making intervention more likely.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.