Dollar eases ahead of the FOMC

Overview: The dollar is has been sold against nearly all the world's currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors. The South African rand and Mexican peso are leading the emerging markets currencies higher, and the JP Morgan Emerging Market Currency Index is stronger for the fourth consecutive session. Equity markets are mostly higher, though, in Asia, China, Hong Kong, and South Korean markets saw profit-taking. Australia, Taiwan, and Australia rallied more than 1%. Europe's Dow Jones Stoxx 600 has advanced consistently since last Thursday's ECB meeting. US stocks are trading higher, and that would put the S&P 500 near yesterday's highs. Debt markets quiet, and benchmark 10-year yields are a little softer. The US 10-year yield is near 66 bp. Gold is higher, but below yesterday's high (~$1972). Oil is extending its rebound that began yesterday. Rather than increase, US oil inventory was drawn down, according to API, by 9.5 mln barrels. The official EIA estimate is released later today.

Asia Pacific

China challenged the US 2018 $360 bln tariffs at the WTO and won the ruling by a three-person panel. The judges found that the US tariffs to be excessive and discriminatory and concluded Washington did not make its case for an exemption from the rules. Nor did it accept the US argument for negotiations outside the WTO. Still, for China, it is a pyrrhic victory because blocking the appointment of new appellate judges, the US has paralyzed the conflict resolution process. By appealing, and it can within the next 60 days, the US would render the decision moot.

Still, on the one hand, China scores propaganda points to the US as violating international trade rules. It is the US that is cast as a revisionist. On the other hand, the far-reach of the American president is demonstrated. If Biden wins, Trump is thought to deliver a fait accompli. To show the US is a good citizen in global institutions, which the Trump Administration has eschewed, Biden would have to retract the levies and thereby making a concession to China. Yet, the dilemma does not seem unmanageable, and Beijing might want to be inclined to make some concessions and give Biden a chance to reset the relationship.

Former cabinet secretary Suga was elected leader of the LDP at the start of the week and earlier today became Prime Minister. Although some reshuffling of the cabinet was widely expected, the finance minister (Aso) and the foreign minister (Motegi) remain. Separately, Japan reported its August trade figures. Exports were down less than expected 14.8%, the least in five months. They were off more than 19% in July. Imports did not recover as much as expected and were still 20.8% from a year ago. The net result was a larger than expected trade surplus of JPY248 bln. Ironically, the average monthly trade deficit this year is JPY248 bln. This is not a fluke. It has run a trade deficit in 20-18 and 2019 too.

The dollar is holding a little above the lower end of the recent range near JPY105. There were $1.3 bln in options set to expire today between JPY105.15 and JPY105.25. There is another option for nearly $840 mln at JPY105 that also expires today. A break of JPY105 will likely trigger stop-loss selling, and while initial support is seen around JPY104.80, the greenback did trade down to almost JPOY104 at the end of July. The Australian dollar is firm, but within yesterday's range when it reached nearly $0.7345. Ahead of tomorrow's employment report, the Aussie may be restrained. The PBOC set the dollar's reference rate at CNY6.7825, while the median bank model, according to Bloomberg, was near CNY6.7850. The yuan is at its strongest level since May of last year.

Europe

UK August CPI was soft, but the weakness has been exaggerated by a temporary cut in the sales tax and other discounts and incentives launched to draw British consumers as the economy gradually re-opens. The preferred measure, which includes owner-occupied housing costs, slowed to 0.5% from 1.1%. The core rate was also halved to 0.9% from 1.8%. There are no policy implications, and the BOE will likely look through it at tomorrow's MPC meeting. The BOE is expected to do nothing while laying the groundwork for an adjustment before the end of the year. The politics of Brexit have been the main focus, but today, a logistics trade group warned that a key piece of technology for customs will not be fully tested and ready for the end of the year. This gives a small sense of the complexity of what is involved, even if the divorce (amputation?) was more amicable.

Reports the EU will grant the UK institutions the ability to clear euro trades and derivatives until the middle of 2022. It represents an 18-month extension. The EU is not prepared with its own clearing capacity to replace the UK, but efforts to do so should be expected. That said, it is reasonable to suspect that another extension will be needed.

The eurozone reported a July trade surplus of 27.9 bln euros. It is the largest trade surplus since March. In the first seven months of the year, the average monthly trade surplus stands at 16.14 bln euros, down slightly from the 17.0 bln euros average for the same period last year. Unlike in Japan and Switzerland, where the return on investment (dividend coupon payments, profits, licensing fees, royalties, and the like)) drives the current account surplus, in the EU, it is the trade surplus that fuels the current account surplus.

The euro found support just ahead of the roughly 655 mln euro option struck at $1.1835 that expires today. It is knocking on the $1.1880 area in the European morning. The euro held $1.19 yesterday. A dovish Fed may give the impetus to take it out today, but it may also become a "buy the rumor (of dovish Fed) and sell the fact" type of affair. Late longs may take profits above $1.19. Sterling is trading at four-day highs near $1.2950. There is an option for nearly GBP360 mln at $1.30 that will be cut today. The (38.2%) retracement of its recent sharp drop is near $1.3040.

America

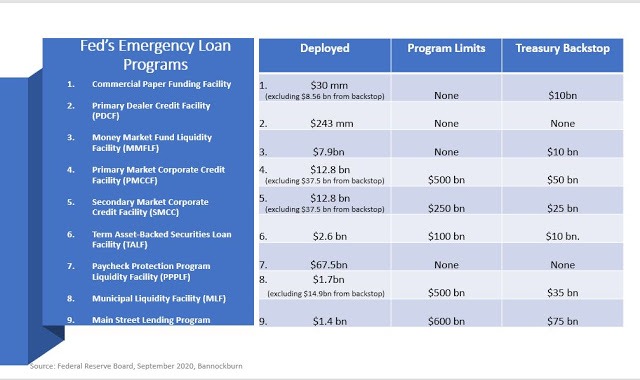

The Federal Reserve meets amid expectations that its concerns about the downside risks to the economy will give its economic assessment and forward guidance its specific gravity. After achieving maximum flexibility by eschewing the point inflation target to an average rate, and purposefully not specifying the period that the average covers, Powell is not about to allow the media to encroach upon it during the press conference. As the chart below, created by my colleague Dimitrios Skambas, shows many of the Fed's facilities launched during the crisis are hardly being used. The Fed's balance sheet has fallen in two of the past three weeks, and in any event, it is about $155 bln small than it was at its peak three months ago, and that is with it buying about $20 bln of Treasuries a week.

While the quarter began off with a bang, the recovery appears to have slowed, and that is the takeaway from the disappointing industrial production report yesterday. It showed only a 0.4% increase in output on the month, less than half of what economists forecast. The upward revision to July's gain from 3.0% to 3.5% compounds that loss of momentum rather than making up for the miss. Manufacturing output missed expectations too. The 1.0% would under normal circumstances be outstanding, but now fit into the flagging momentum meme. Originally reported at 3.4% in July, manufacturing was revised up to 3.9%.

Although the Atlanta and St.Louis GDP trackers ae higher than the NY Fed model (30.8% and 20.21% respectively), the NY Fed model captures the sense, many people have that the economic momentum is fading. It sees the US economy tracking 15.6% annualized growth in Q3 and then slowing to 7.3% in Q4. The median forecast in the Bloomberg survey has change at a nearly 25% annualized pace in Q3 and 5% in Q4. Expectations of the first hike, according to the CNBC survey, were pushed back to February 2023, six-month deference from the July survey. According to that CNBC survey, 48% expect inflation to be over 2% for six months before the Fed hikes, and nearly as many (41%) think it has to be above there for a year.

Ahead of the FOMC meeting, the US reports August retail sales. After a 1.2% increase in July, the median forecast in the Bloomberg survey is for a 1.0% gain, though we suspect risk in on the downside. Core sales, which exclude autos, gasoline, and building materials, are expected to show the weakness. The median forecast is for a 0.4% gain in August following the 1.3% increase in July, 6.0% in June, and 10.4% in May. Canada reports August CPI figures. The low headline rate (0.4% year-over-year possibly after 0.1% in July) is unlikely to distract from the firm underlying rates that may tick up to 1.7% on average from 1.6%.

Hours before Canada was set to retaliate against US tariffs on its aluminum, Washington unexpectedly retreated. The US tariffs were dropped and retroactive to the start of the month. The most recent US data is for June, and imports of raw aluminum from Canada fell 2.6% on the month. Canadian data showed a 19% decline in July. The US tariffs were announced in mid-August. The aluminum industry was opposed to the levies. The US appears to have replaced the tariff with a soft quota. If actual shipments surge above a certain level ("105% of expected") for the remainder of the year, the 10% tariff would be reimposed for that month.

The US dollar continues to encounter offers near CAD1.32. With the cap being formidable, the path of least resistance may be lower. Rising oil and equities amid a weaker US dollar environment more broadly can be setting up for a test on the lower end of the recent range seen in the CAD1.3125-CAD1.3135 area. A break sets the stage of a return of CAD1.30. The greenback is testing the MXN21.00 level. It has not seen it in six months. The dollar finished last week near MXN21.76 and is extending its drop for the seventh consecutive week.Recall that the low for the year was set in February near MXN18.52.

Author

Marc Chandler

Marc to Market

Experience Marc Chandler's first job out of school was with a newswire and he covered currency futures and Eurodollar and Tbill futures.