China can make to justify refusing the US overtures

Outlook:

To set the stage, Congress passed the new budget deal and Trump is expected to sign it today, although you never know for sure until the ink is drying. Trump also announced he will claim a national emergency on border security and raid other funded programs to get the money, something that is unconstitutional. We still don’t know how strongly Congress will push back. This is entertaining but not a financial market factor, although any time Trump is casting around for a disruption to distract attention from something that reflects badly on him, we should worry. What reflects badly on him this time is the government shut down that left him with a worse Wall funding amount than he had before, getting beat by a girl, and a judge taking away leniency for campaign chief Manafort for lying, again.

We get a fair amount of fresh data today, including industrial production, TICS, the Empire State manufacturing survey and the University of Michigan consumer sentiment. All of these are expected to be disappointing. Canada gives us existing home sales (read yesterday’s prediction of housing crisis). Barring a surprise, none of these will have a big effect on equities or the dollar, not with the China trade deal front and center.

Bloomberg reports TreasSec Mnuchin tweeted that talks were “productive,” but this is weak tea. If we had a meaningful deal, surely Mnuchin would be shouting from the rooftop. Maybe he has to get home to persuade Trump, but more likely is that the deal is unsatisfactory to the US stance, if there is a memorandum of understanding at all. We may find out today but don’t count on it. If it’s bad news, everything will depend on the Trump response over the weekend. Trump is impulsive and erratic. He may be restrained by cooler heads that will remind him that he will get blamed for another stock market plunge if he flies off the handle and imposes the 25% tariff immediately. It’s not hard to see him doing that, or some version of the same thing—more threats, a new deadline, etc.

It’s not hard to imagine the case China can make to justify refusing the US overtures. A central feature of the US stance is that China has to downgrade or even give up the sovereignty embedded in state-owned enterprises. That sovereignty takes the form of getting all the trade secrets and management techniques of foreign partners. So, asking China to stop doing that is an outright assault on the Chinese form of communism, and that’s not happening. Rock and hard place.

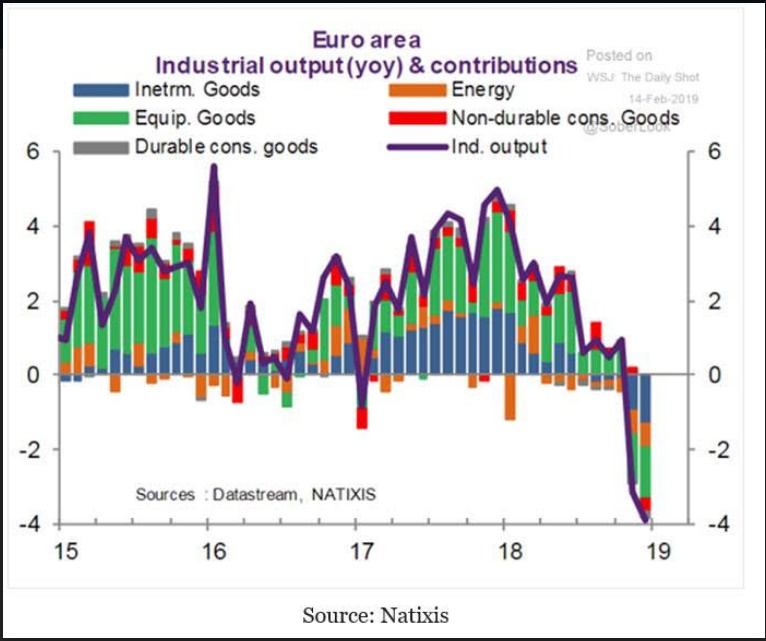

We may not get a new trade crisis this weekend, but the probability is not zero, either. We will likely start getting talk of recession again any minute. Normally this would be dollar-negative but conditions elsewhere are as bad or worse, with the possible exception of Japan. See the chart of eurozone industrial output by sector (from the DailyShot). Egad! We complain about the US slowdown but Europe is barely escaping outright recession.

We continue to see the euro as oversold but sentiment is not abating as it normally does, and the UK is in such a shambles that even the staunchest of bulls can’t get a grip. So, we can’t see an end in sight to dollar strength. Not until an outright rate cut becomes a consensus opinion.

Tidbit: Front-page news in New York is another bully, Amazon, pulling out of its deal to build a $2.5 billion facility in the city that would provide 25,000 jobs—because protesters complained about a $3 billion “corporate welfare” tax break and other grievances. Amazon said it will take its dolls and dishes and go somewhere else—after all, some 200 cities spent a fortune preparing proposals to get that business. Here’s the kicker—the governor and mayor were given no notice. Amazon made the decision without any effort to mitigate.

We wonder how much the unionization issue was at fault. Europeans would be amazed, but here a company can take a non-union stance. That’s what Amazon did. Some unions supported the deal anyway, but others opposed it. At a city council meeting, according to the NYT, a council member proposed Amazon drop its opposition to unionization. The Amazon rep refused. We are a little fuzzy on the point—laws allow unionization regardless of what the company prefers, and the only recourse a company has to having its workers form a union and engage in collective bargaining is to close shop. So that’s what Amazon did.

Does this imply unionization is coming back as a social/political force? Not if the big monopolies can help it. As the Dems gather strength, this could become a talking point and platform issue in the next election. Don’t laugh—the first debate for Dem candidates is already scheduled for June. Unions were mostly for Trump last time, believing his lies about being pro-union, belied by his executive order reining in federal unions and his own track record of preferring non-union labor in his own business and countless lawsuits against unions. In short, unions got snookered.

If Clinton had been competent, she would have focused on this point. But the Dems took unions for granted or neglected them—their power was waning anyway, ever since Reagan broke the air traffic controllers in the 1980’s. Unions have a bad record of abusive conduct in the US but if we are going to make a big deal about income inequality, it’s hard to do without promoting unionization all over again. And Amazon is coming under attack for not paying a penny in federal income tax in 2018 despite making $5.6 billion in 2017. This is like GE not paying any federal income tax a few years ago (before it hit the ropes). The Dems should stop taking about taxing wealth and start talking about setting this apple cart aright again.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat