CFTC Positioning Report: Speculators turned bullish on the Dollar

The latest CFTC position report for the week ending June 3 reveals that investors are still focused on the White House's trade policy and the health of the US economy, particularly its labour market. Furthermore, markets continued to process another cautious message from the FOMC Minutes.

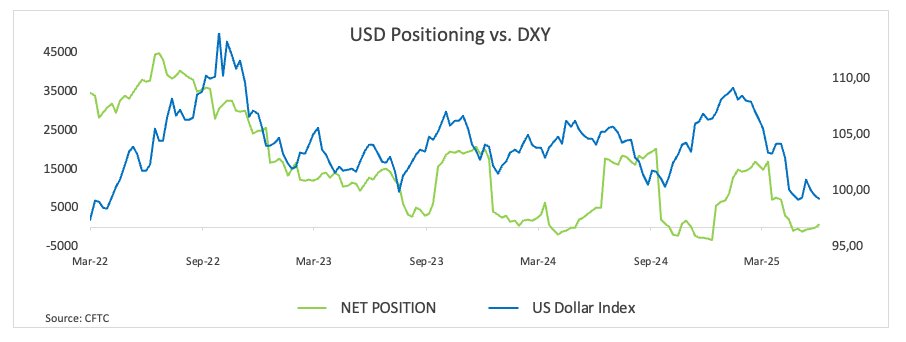

Non-commercial investors have adopted a bullish stance on the US Dollar (USD), with net longs making a comeback after a six-week hiatus, rising to just over 600 contracts. The decision was made in the context of a slight decline in open interest, which now stands at approximately 28K contracts. The US Dollar Index (DXY) has fallen below the 99.00 support level, indicating a potential shift into a consolidative range in the market.

Speculative net longs in the Euro (EUR) have increased, reaching three-week highs of nearly 82.8K contracts. In a notable development, commercial players, particularly hedge funds, have increased their net short positions to approximately 138K contracts, marking the highest level observed since early September 2024. Open interest has now exceeded 781K contracts, reaching a peak not seen in over three years. EUR/USD has gained further upward momentum, extending the move further north of 1.1400 the figure.

Non-commercial net longs in the British Pound (GBP) have surged, reaching approximately two-month highs of nearly 103.7K contracts, alongside a significant rise in open interest. GBP/USD has demonstrated resilience, steadily advancing toward its upper range, surpassing the 1.3500 hurdle.

Speculators have reduced their net long positions in the Japanese Yen (JPY), reaching an eight-week low of slightly more than 151K contracts. Commercial traders have reduced their net short position to approximately 175.5K contracts, marking the lowest level since early April. At the same time, open interest has fallen to approximately 366K contracts, which marks a two-week low. USD/JPY’s gradual decline encountered contention in the mid-142.00s during that timeframe.

Speculative net longs in Gold have reached seven-week highs, totalling approximately 188K contracts, alongside a decent decline in open interest. The prices of the precious metal continued to show a gradual recovery, yet a significant resistance level seems to have formed near the $3,400 mark per troy ounce.

Speculators have ramped up their net long positions in WTI, hitting two-week highs with around 168K contracts. Additionally, open interest has exceeded the 200K mark for the first time since March 2022. WTI prices made an effort to break out of the consolidative phase, nearing the $64.00 per barrel threshold. Market participants continue to monitor trade dynamics, geopolitical events, and OPEC+ actions closely.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.