Canada CPI

Canada: CPI (Feb)

-

CPI rose by 0.4% m-o-m in February. The consensus expectation was for a rise of 0.5%.

-

The annual rate of inflation fell to 5.2% from 5.9%. This also came in below the expected 5.4%.

-

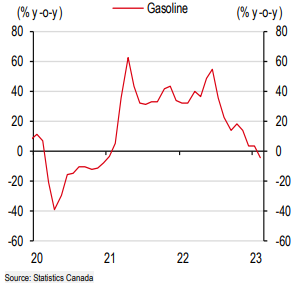

Gasoline inflation fell into negative territory, thus shifting from inflation tailwind to headwind for the first time since January 2021.

Facts

CPI rose by 0.4% m-o-m in February. The consensus was for a rise of 0.5%. In the month, the main upward contributors to the monthly change in prices were telephone services, mortgage interest costs, rent, women’s clothing, and non-electric utensils. The main downward contributors were child care services, natural gas, gasoline, meat, and air transportation.

The annual rate of inflation fell to 5.2% from 5.9% in January, and below the expected reading of 5.4%. The main upward contributors to inflation were mortgage interest costs, food purchased from restaurants, rent, passenger vehicles, and homeowners’ replacement costs, The main downward contributors were gasoline, child care services, passenger vehicle registration fees, purchase of digital media, and video equipment.

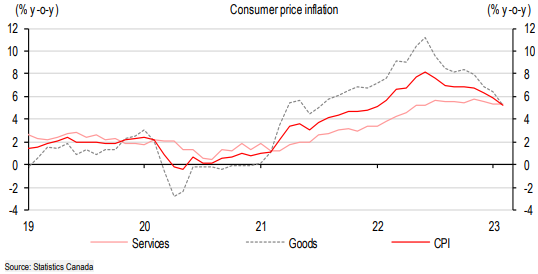

Notably, as shown in Figure 1, the annual rates of headline, goods, and services inflation have all converged at just over 5%. The drop in headline inflation since June 2022 has been primarily due to a drop in goods price inflation.

1. Inflation rates have temporarily converged as easing goods price inflation weighs on headline inflation

Implications

The February CPI report showed that the factors that had pushed inflation up in 2021 and 2022 are dragging inflation lower in 2023. For example, gasoline prices declined on a y-o-y basis for the first time since January 2021. In June 2022, the month that CPI inflation peaked at 8.1% y-o-y, gasoline prices were up by 54.6% y-o-y (figure 2). Thus, gasoline has gone from an inflation tailwind to a headwind. Further downward pressure is likely in March, given the recent decline in oil prices.

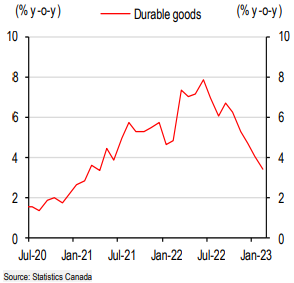

As well, as global supply chain disruptions continue to ease, durable goods price inflation continues to decline (figure 3)

2. Gasoline prices have shifted from inflation tailwind to headwind

3. Durable goods inflation has been falling sharply for the past few months

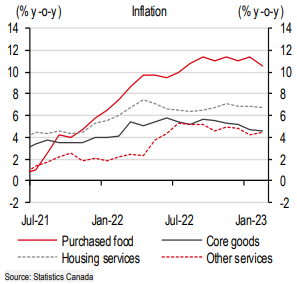

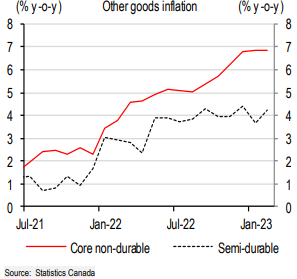

There has been less progress, however, in those components of CPI that are sensitive to domestic demand and that are relevant to the Bank of Canada’s determination of whether monetary policy is restrictive enough. For example, housing services inflation, other services inflation, and food price inflation show few signs of sustained decline (figure 4). As well, beyond the pull-back in durable goods inflation, core goods inflation remains elevated as semi-durable goods and core non-durable goods inflation have stayed high (figure 5).

4. There are few clear signs of a broad decline in inflation

5. Non-durable and other goods prices are still rising quickly

In my view, headline inflation is falling more quickly than anticipated, in part due to base effects, but underlying inflation remains elevated. That said, I think the results are sufficient to allow the Bank of Canada to leave its policy rate unchanged at 4.5% at its 12 April policy meeting in order to continue to assess the evolution of underlying inflation pressures, and the potential effects of the increase in global financial sector uncertainty.

Author

ACY Securities Team

ACY Securities

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis. The key pi