Bank of Canada Rate Decision Preview: Rewards of Economic patience

- Overnight rate expected to be unchanged after rate decision.

- Canadian economy projected to improve following US-China trade pact.

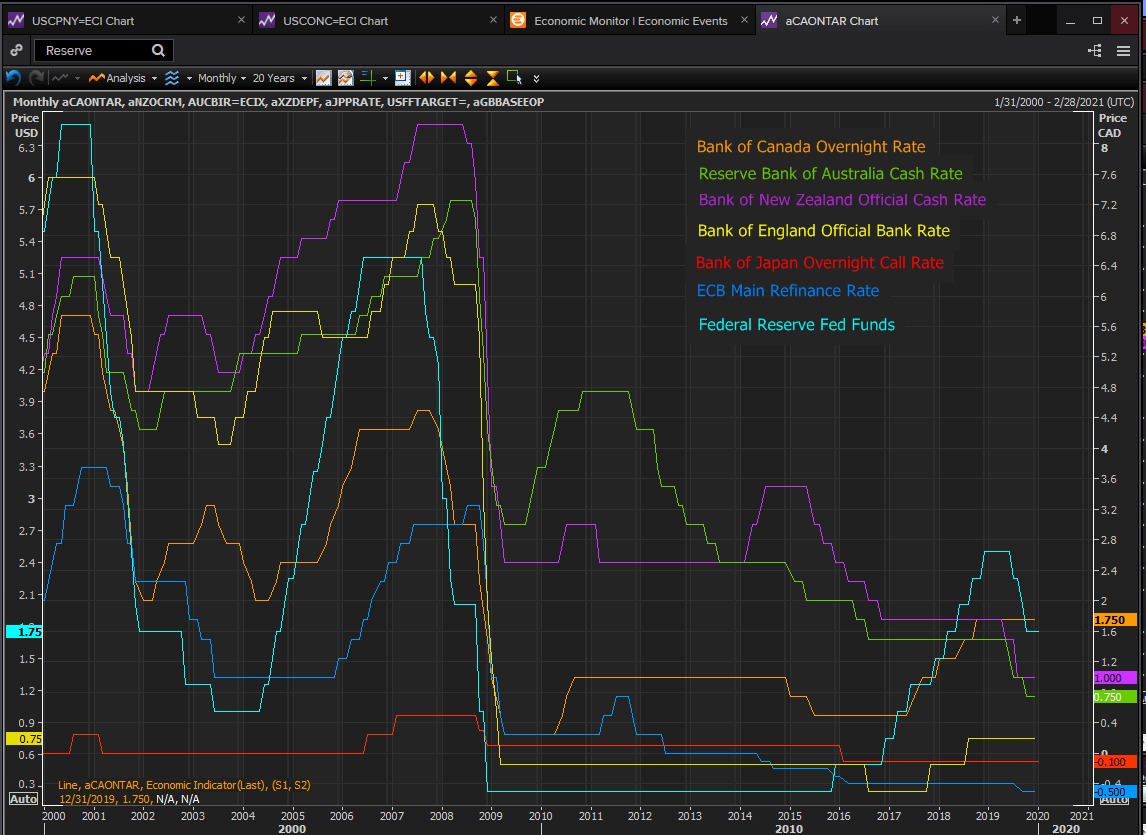

- BOC has the highest base rate of the seven major central banks.

The Bank of Canada will issue its decision on its base overnight rate on Wednesday January 22nd at 10:00 EST, 15:00 GMT. The bank will also release its quarterly Monetary Policy Report. Governor Stephen Poloz will hold a press conference at 11:15 EST, 16:15 GMT.

Forecast

Bank of Canada is forecast to leave the overnight rate at 1.75% where is has been since it was increased 25 basis points on October 24th 2018. The bank makes rate policy decisions at eight fixed date meeting a year. The next is March 4th.

The Monetary Policy Report is “*A quarterly report of the Bank of Canada’s Governing Council, presenting the Bank’s base-case projection for inflation and growth in the Canadian economy, and its assessment of risks.”

*Bank of Canada website.

Bank of Canada and the summer rate swoon

The Bank of Canada was unwilling to participate in the summer’s economic insurance policy first instituted by the Reserve Banks of New Zealand and Australia and followed by the American Federal Reserve.

New Zealand began on May 8th dropping its base rate by a quarter point from 1.75% to 1.5% Australia followed on June 5th with 25 basis points and the US on July 31st. New Zealand and Australia cut twice each ending at 1.0% and 0.75% respectively. The Fed reduced three times finishing at a 1.5% to 1.75% target range.

Primary motivation for each of the banks was the potential for the US-China trade dispute, then at its height, to damage their economies particularly if it devolved into a full-fledged trade war with permanent high tariffs and restricted exports. Both antipodean economies have extensive export relations with China and if the mainland economy was suffering from the argument with the United States their part in the dispute might be a recession.

The three other major central banks, the Bank of Japan, the ECB and the Bank of England did not participate in the summer insurance cuts but the reasons were specific to their situations. The ECB and the BOJ already had negative base rates and prospect of a global recession should the US and China not make an agreement was not enough to delve further into the dubious benefits of deeper negative rates. The BOE was in the throes of its long-running Brexit crisis and with an official bank rate of only 0.75% was saving its limited ammunition for the home front.

Reuters

Canadian economy

In the mid to late summer Canada appeared reasonably healthy for a largely resource based economy in the midst of a global slowdown and a damaging trade argument between its largest trading partner and the world’s largest commodity importer.

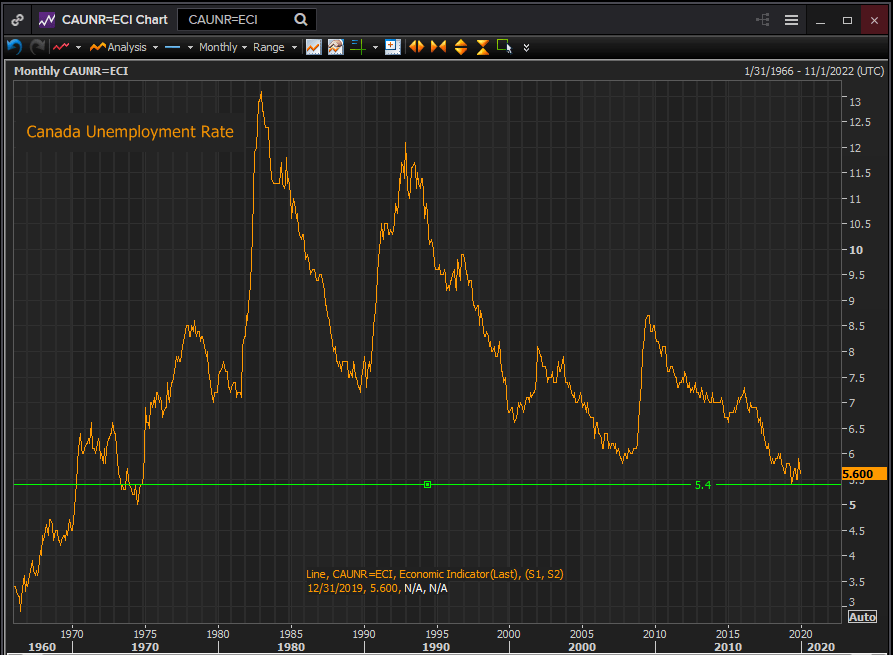

Unemployment had dropped to 5.4% in May, 5.5% in June and 5.7% in July and August all the lowest in 45 years.

Reuters

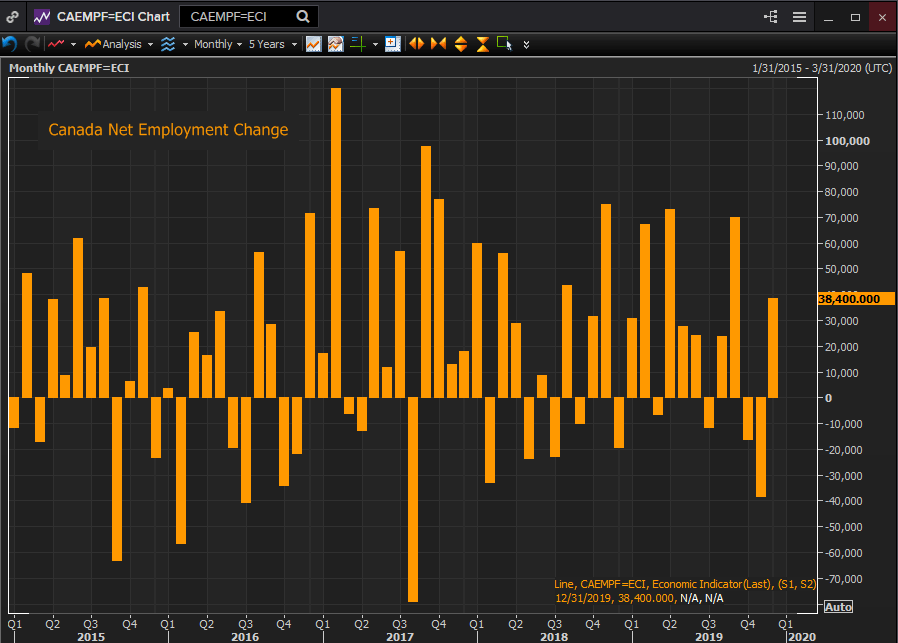

Job creation had resumed in August and September at 81,100 and 53,700 after combined losses of 26,400 in June and July. Housing starts had averaged 225,000 in July and August and rising house prices suggested a solid home market. With the Ivey purchasing managers’ index 54.2 in July and 60.6 in August, the business outlook seemed sanguine. If retail sales had weakened in May and June, -0.2% and -0.1%, they had recovered in July to 0.4% and August to 0.1% and with a strong labor market retail purchases were unlikely to drop in any significant fashion.

Reuters

A number of these statistics, Ivey PMI, housing starts, job creation and retail sales deteriorated into the fall but by that time the US and China had announced their pending agreement, since signed in Washington and the RBNZ, the RBA and the Fed has all resumed a neutral stance. The moment for insurance cuts had passed.

Conclusion and the Canadian dollar

The Bank of Canada’s reluctance to join the summer rate cuts in unlikely to be reversed now that the original China trade motivation has reached a positive solution.

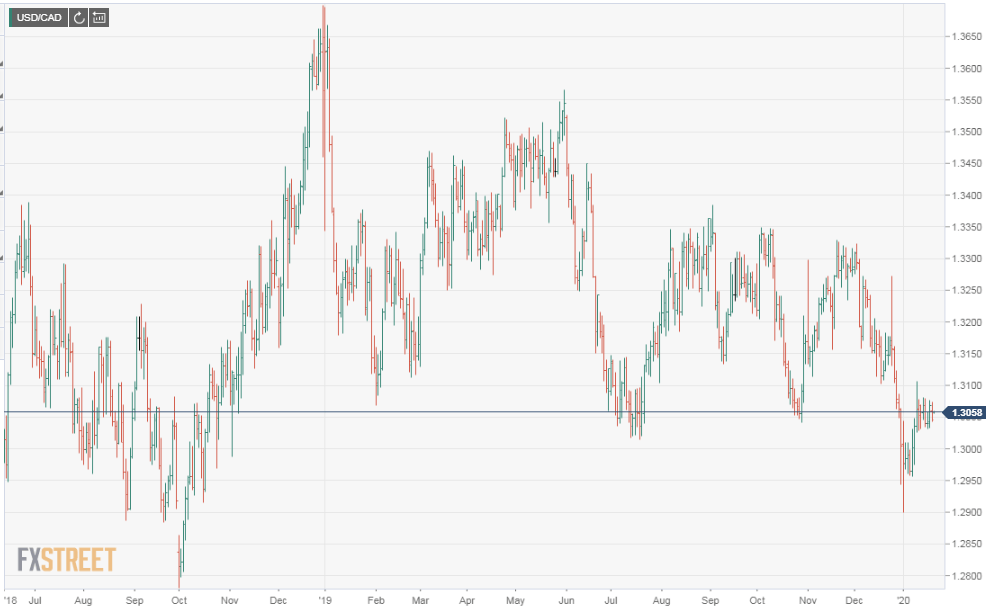

Rate stoicism brought some strength to the loonie in the second half of last year. From a range of 1.3400 to 1.3550 versus the US dollar for much of April and May the average for the USD/CAD fell to 1.3050 to 1.3350 until the end of year plunge to below 1.2950, an anomaly that was quickly reversed in January*.

With the Federal Reserve estimating stable rates through the end of the year, the Canadian dollar will probably not be receiving any more boosts from policy changes.

Questions will now turn to the relative benefits of the China trade deal to the Canadian and American economies. In this the southern partner should have the advantage. Its manufacturing and business community has been struck more heavily and consequently their recoveries should be sharper and more energetic giving the US dollar its advantage as the first quarter wears on.

*Because the Canadian dollar is quoted and traded against with the US dollar a rise in the loonie means a fall in the USD/CAD and the reverse.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.