Are Small Businesses Financially Vulnerable?

Executive Summary

Businesses have increased debt loads over the course of the current economic cycle, generating some concern from Fed officials and market watchers. In a previous report, we examined the health of non-financial corporate (NFC) businesses by developing an index of eight financial measures. We determined that the financial health of the corporate sector was not worrisome at present, despite having deteriorated somewhat in recent years. But what about the financial health of the non-corporate sector, i.e., small businesses?

Using the methodology in our last report, we create an index to gauge the financial health of the non-financial non-corporate (NFNC) business sector. Debt in the NFNC sector has trended higher over the expansion, but, unlike the corporate sector, remains within its historic range when measured against GDP. By most metrics, the finances of NFNC businesses appear to be in decent shape. The majority of debt is long term, asset values have been rising faster than debt, and interest coverage remains historically high. Yet, our overall index of NFNC health shows the financial position of smaller businesses is weakening on net, as debt continues to increase, interest rates rise and profit growth slows.

More to the Business Sector than Just Corporations

In a recent report, we developed an index to gauge the financial health of the non-financial corporate sector.1 The methodology we employed allowed us to succinctly aggregate eight metrics of corporate financial health into a single index. In short, we concluded that the financial health of the NFC sector has deteriorated, at least at the margin, in recent years.

Corporations account for about 55% of the national income that is currently produced in the United States. But other legal forms of business organization—largely proprietorships and partnerships— are important parts of the business sector as well. Specifically, non-corporate businesses accounted for $3.4 trillion of the $16.8 trillion in national income that was produced in the U.S. economy in 2017. In this report, we use the methodology we developed in our previous report to analyze the financial health of the non-financial non-corporate sector.

Individual Financial Metrics of the Non-Corporate Sector: A Mixed Bag

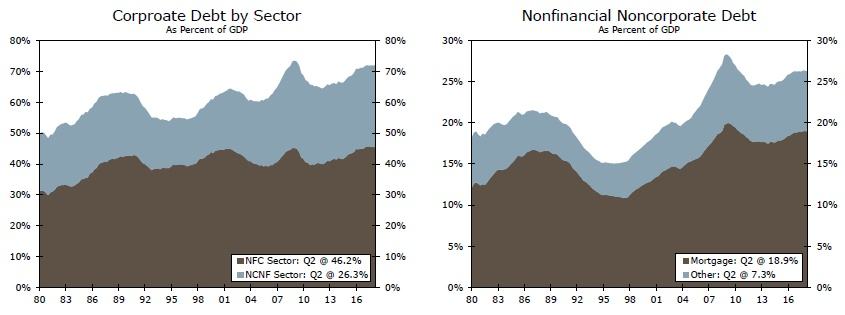

We noted in our previous report that the debt-to-GDP ratio of the NFC sector currently stands at an all-time high of 46%. The debt-to-GDP ratio of the NFNC sector has also trended gradually higher over the past few years to about 26 percent at present (Figure 1). Consequently, the debt-to- GDP ratio of the overall business sector is currently about a percentage point lower than its all-time high of nearly 74% that was set in Q1-2009. As shown in Figure 2, mortgages account for the lion's share of the outstanding debt of the NFNC sector. Mortgage debt among NFNC businesses ramped up significantly in the decade or so preceding the financial crisis, but mortgage debt in the sector is a bit lower today (as a percent of GDP) than it was about ten years ago.

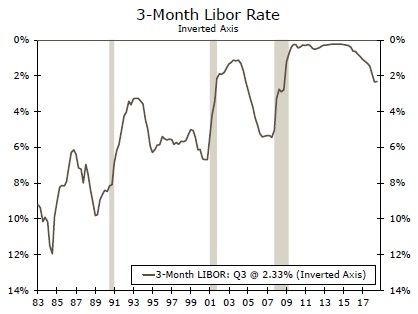

So what can we say about the financial health of the NFNC sector? Let's start by looking at each of the financial metrics we identified in our previous report. For starters, three-month LIBOR, which we use as a proxy for short-term interest rates, has risen due to the 200 bps of Fed tightening that has occurred over the past three years. Everything else equal, higher borrowing costs are associated with a deterioration in financial health (Figure 3)2.

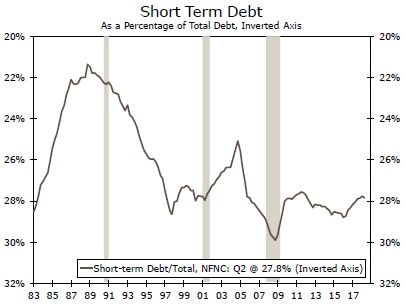

As noted above, mortgages, which are long-term debt, account for the majority of NFNC loans outstanding. Consequently, short-term debt comprises less than 30 percent of the overall debt profile of the NFNC sector, and this ratio has been generally stable over the past few years (Figure 4). Moreover, the generally low level of the ratio implies that NFNC businesses are not overly sensitive to rising interest rates on the short end of the yield curve.

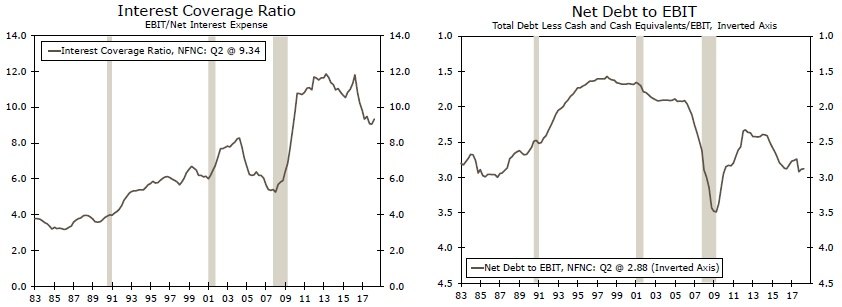

Nevertheless, the interest coverage ratio of the NFNC sector has slipped in recent quarters, which indicates some deterioration in the financial health of the NFNC sector, everything else equal (Figure 5). The ratio shot up markedly in the early years of the current expansion as proprietors' income rebounded sharply and as interest expenses receded due to accommodative monetary conditions. But interest expenses are rising now that the Fed has been tightening monetary policy over the past three years. Furthermore, the modest increase in leverage in the NFNC sector in recent years has led to some deterioration in the sector's net debt-to-EBIT ratio (Figure 6).

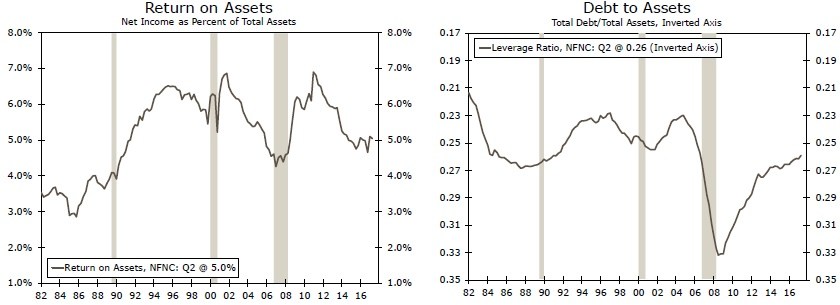

Real estate (both residential and non-residential) accounts for 60% of the assets in the NFNC sector, so real estate prices have had an influence on some of our financial metrics. On one hand, return on assets in the sector has trended lower in recent years as real estate values have risen (Figure 7). On the other hand, however, the rise in real estate prices has caused the value of assets to rise relative to the value of debt. Consequently, the debt-to-asset ratio of the NFNC sector has receded over the past few years, which implies an improvement in the sector's financial health, everything else equal (Figure 8).

Finally, the quick ratio (i.e., the ratio of current assets less inventories to short-term liabilities) of the NFNC sector has been essentially unchanged at a high level during the current expansion (Figure 9).

To recap, there are four metrics for the NFNC sector that have experienced some weakness in recent years (LIBOR, the interest coverage ratio, the net debt-to-EBIT ratio and return on assets). Two metrics have remained more or less unchanged (short-term debt as a percent of total debt, and the quick ratio). One metric has noticeably improved (the debt-to-asset ratio). Finally, there is one metric that we analyzed for the NFC sector that is not included in the analysis for the NFNC sector. Specifically, proprietorships and partnership do not have a market value for their equity (at least not easily observable), so we do not have a market-to-book ratio for the NFNC sector.

Should We Worry?

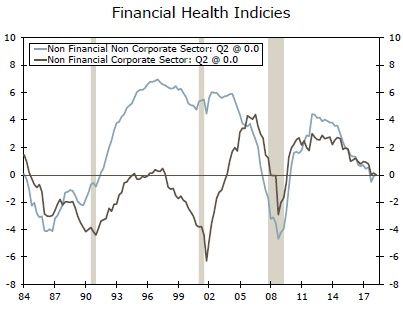

So where do these seven financial metrics leave us in regard to the overall financial health of NFNC businesses? Applying the same methodology that we used in our previous report, we constructed a financial health index for the NFNC sector (Figure 10). As we found with the NFC sector, there has been some deterioration in the financial health of NFNC businesses in recent years. Not only has net debt in the NFNC trended higher, but higher interest rates have pushed the interest coverage ratio lower. In addition, return on assets has also receded.

Our analysis suggests that the "high water mark" for the NFNC sector was reached in the mid-1990s through the middle years of the past decade. In those years, NFNC businesses had lower debt-toasset ratios as well as a lower net debt-to-EBIT ratio. The amount of short-term debt that they held (as a percentage of total debt) was a bit lower than it is today, and their return on assets was somewhat higher in those years.

That said, we are not overly concerned about the financial health of the NFNC sector at this time. The interest coverage ratio generally remains at a high level and NFNC businesses have plenty of current assets relative to their short-term liabilities (i.e., the quick ratio stands at a high level). But like the larger NFC sector, we will be keeping a close eye on the NFNC sector going forward for signs of further financial slippage.

Conclusion

Corporate sector debt has come under the microscope recently, but debt has also been increasing among non-corporate businesses. Although a number of measures of the health of the NFNC sector look to be in fairly good shape, finances have deteriorated modestly over the past few years. Similar to the corporate sector, higher interest rates have contributed to a decline in interest coverage, while earnings have not kept pace with new debt. As a result, the non-corporate business sector appears to be a bit more vulnerable to a slowdown or shock to the economy than it was a few years ago.

As the Fed continues to raise rates and profits come under pressure as growth slows, we would expect to see further weakening in the health of the non-corporate sector. Further deterioration could limit the NFNC sector's wherewithal to invest and hire, as well as weigh on the banking system if the sector has difficulty paying back loans. Accordingly, we will be paying close attention to the health of the non-corporate sector in addition to the corporate sector.

Author

Wells Fargo Research Team

Wells Fargo