All eyes on ECB

Market Brief

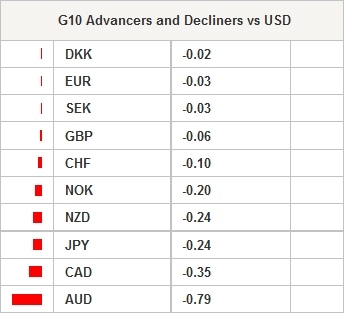

Asian markets firmed with strong US corporate earnings and rising oil prices supporting risk taking. In addition, the third and final US presidential debate ended lowering political uncertainty risk. Perhaps the one lingering issue concerning this debate was Republican Donald Trump’s suggestion that he would reject the outcome of the Nov. 8th presidential election. An unprecedented challenge to American democracy and the reason why traders are buying the skew on such currencies as AUDUSD and USDMXN. Now this risk can be pushed off till a later date. Wall Street gained for the second straight session as energy prices lead the way on the back of higher oil price. There was also a solid surprise from financial including earnings from Morgan Stanley. Yet with the ECB meeting ahead, Asian regional equity markets are tempering any over optimism. The Nikkei rallied 1.39 as the JPY was weaker against the USD and the Softbank-Saudi Arabia deal to create a $100bn investment fund. The Hang Seng rose 0.048, while the Shanghai Composite had a hard time keeping its head above water. In the FX markets, the USD was stronger against the G10 and EM currencies. AUDUSD led the losers, falling from 0.7734 to 0.7660 as economic data disappointed. Australian September employment change fell -9.8k vs. 15k exp. The weak read has increased speculation that the RBA will cut rates again.

In the UK, labor markets continued to disprove the critics. The UK unemployment rate remained at the lowest level since 2005 at 4.9%, while wage growth increased 2.2%. Brexit should eventually drive unemployment higher yet at this point there is scant evidence of a mass migration of jobs.

Yesterday, the BoC kept rates unchanged but actively discussed additional easing. While the risk remains toward further accommodated we anticipate the BoC will hold off any additional cuts.

In Brazil, the BCB reduced the SELIC rate by 25bp starting an easing cycle. The Copom will likely move cautiously as will significantly macro uncertainties on the horizon. We can expect additional rate cuts at the November 30th meeting but then a pause.

In the US, housing starts came in well below consensus dropping -9.0% m/m to 1.047mn against 1.173mn expected in September. This weak read will be a negative drag on growth lowering Q3 GDP estimates.

Today's ECB monetary policy decision will dominate trading. We do not expect any changes to policy (likely wait till December meeting) or changes to QE. Even an announcement of adjustments to technical parameters, such as a removal of yield floor is a low probability event (although not to be ruled out). This will put the emphasis on the Q&A session to see ho Draghi handles questions on framework, extensions and inflationary outlook.

Elsewhere, the Central bank of Turkey will announce its monetary decision today. Given the political uncertainty and interference as government officials have hinted, there is unease and with the TRY weakness there is a high likelihood of no move.

ECB aside, traders will be watching UK retail sales and US Philly Fed and existing home sales.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 17235.5 | 1.39 |

| Hang Seng Index | 23396.14 | 0.39 |

| Shanghai Index | 3084.46 | -0.08 |

| FTSE 100 Index | 7011.49 | -0.14 |

| DAX Index | 10656.24 | 0.09 |

| SMI Index | 8066.28 | -0.33 |

| S&P 500 Index | 2138 | -0.004 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1268.42 | -0.06 |

| Silver | 17.63 | -0.22 |

| VIX | 14.41 | -5.9 |

| Crude wti | 51.07 | -1.02 |

| USD Index | 97.97 | 0.04 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| SZ Sep Trade Balance | - | 3,02E+09 | CHF/06:00 |

| SZ Sep Exports Real MoM | - | -2,10% | CHF/06:00 |

| SZ Sep Imports Real MoM | - | -3,50% | CHF/06:00 |

| JN Sep F Machine Tool Orders YoY | - | -6,30% | JPY/06:00 |

| DE Sep Retail Sales MoM | 0,20% | -0,20% | DKK/07:00 |

| DE Sep Retail Sales YoY | - | 0,20% | DKK/07:00 |

| JN Sep Convenience Store Sales YoY | - | 0,60% | JPY/07:00 |

| SW Sep Unemployment Rate | 6,30% | 6,60% | SEK/07:30 |

| SW Sep Unemployment Rate Trend | - | 7,00% | SEK/07:30 |

| SW Sep Unemployment Rate SA | 6,90% | 7,20% | SEK/07:30 |

| EC Aug ECB Current Account SA | - | 2,10E+10 | EUR/08:00 |

| EC Aug Current Account NSA | - | 3,15E+10 | EUR/08:00 |

| UK Sep Retail Sales Ex Auto Fuel MoM | 0,20% | -0,30% | GBP/08:30 |

| UK Sep Retail Sales Ex Auto Fuel YoY | 4,40% | 5,90% | GBP/08:30 |

| UK Sep Retail Sales Inc Auto Fuel MoM | 0,30% | -0,20% | GBP/08:30 |

| UK Sep Retail Sales Inc Auto Fuel YoY | 4,70% | 6,20% | GBP/08:30 |

| EC 20.oct. ECB Main Refinancing Rate | 0,00% | 0,00% | EUR/11:45 |

| EC 20.oct. ECB Deposit Facility Rate | -0,40% | -0,40% | EUR/11:45 |

| EC 20.oct. ECB Marginal Lending Facility | 0,25% | 0,25% | EUR/11:45 |

| EC Oct ECB Asset Purchase Target | 8,00E+10 | 8,00E+10 | EUR/11:45 |

| US 15.oct. Initial Jobless Claims | 250000 | 246000 | USD/12:30 |

| US 08.oct. Continuing Claims | 2,05E+06 | 2,05E+06 | USD/12:30 |

| US Oct Philadelphia Fed Business Outlook | 5 | 12,8 | USD/12:30 |

| US Oct Bloomberg Economic Expectations | - | 41,5 | USD/13:45 |

| US 16.oct. Bloomberg Consumer Comfort | - | 42,1 | USD/13:45 |

| US Sep Existing Home Sales | 5,35E+06 | 5,33E+06 | USD/14:00 |

| US Sep Existing Home Sales MoM | 0,40% | -0,90% | USD/14:00 |

| US Sep Leading Index | 0,20% | -0,20% | USD/14:00 |

Currency Tech

EURUSD

R 2: 1.1616

R 1: 1.1428

CURRENT: 1.1013

S 1: 1.1046

S 2: 1.0913

GBPUSD

R 2: 1.2857

R 1: 1.2477

CURRENT: 1.2229

S 1: 1.2090

S 2: 1.1841

USDJPY

R 2: 111.45

R 1: 107.49

CURRENT: 103.91

S 1: 102.80

S 2: 100.09

USDCHF

R 2: 1.0093

R 1: 0.9950

CURRENT: 0.9881

S 1: 0.9632

S 2: 0.9522

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

Author

Peter A Rosenstreich

Swissquote Bank Ltd

Peter Rosenstreich is Swissquote Bank’s Head of Market Strategy and manages the global strategy desk; he has held various positions in several banking institutions in the United States, Europe & Asia.