Wake Up Wall Street (SPY) (QQQ): The UK variety show keeps on chugging along

Here is what you need to know on Friday, October 14:

Here we go again with the UK taking markets on a merry dance. Latest reports indicate Chancellor Kwarteng is for the chop as PM Truss looks to restore some badly needed confidence from markets. Basically, the UK is capitulating to the bond market vigilantes. Oh, sorry, all change again just as I type this. I see he has now officially resigned. What a show the UK is putting on!

Sterling, one would think, would benefit as it seems the massive bill for tax cuts may not be as large as thought, but yet sterling has fallen. Why? Repeat after me, markets hate uncertainty. I know I bang on about that all the time, but it is true. You can plan for bad or good news but not news that keeps changing. The UK keeps moving the goalposts, so investors will just dump it and wait for some clarity.

Back to equities, Thursday was an incredible day, but basically everyone was short or max bearish. They shorted some more, and then got caught and squeezed hard. Liquidity is terrible, so this exaggerated the moves. Earnings season continues to look decent with Pepsi (PEP) and Domino's (DPZ) on Thursday followed up by all the banks beating this morning, except for Wells Fargo. So far the market is not so happy, and most bank stocks are down.

Can this rally now get some legs? That would lead to further covering, and then we get the CTA trend following crowd jumping on board soon enough. Oh, yes, and the more earnings that are released, the more companies can once again return to their buyback programs. Squeezy, squeezy springs to mind.

The dollar ignored much of the equity rally and has resumed its upward path to 113.20 now for the Dollar Index, with USD/JPY daring the BOJ to intervene again. Gold is lower and will continue to suffer as yields rise. Bitcoin is up at $19,600, and Oil is back down to $87.50.

European markets are higher: Eurostoxx +0.3%, FTSE +0.2% and Dax +0.9%.

US futures are mixed: Dow and S&P are flat but Nasdaq -0.4%.

Wall Street (SPY) (QQQ) top news

UK Chancellor Kwarteng loses his job.

Apple (AAPL) and the NFL are still negotiating a deal for TV rights.

Morgan Stanley (MS): EPS beats, revenue misses, stock down.

Citi (C): beats on EPS and revenue, stock down.

JPMorgan (JPM) beats on EPS and revenue, stock up!

Wells Fargo (WFC): beats on EPS, stock is up.

Deutsche Bank (DB) CEO says German banks are well-capitalized.

Tesla (TSLA) cut by Wells Fargo.

Netflix (NFLX) to launch ad tier at $6.99 per month.

United Health (UNH) raises 2023 outlook, stock up premarket.

Beyond Meat (BYND) cuts revenue forecasts and cuts jobs.

Meta Platforms (META) VP Margaret Steward to leave.

Kroger (KR) confirms a deal for Albertsons (ACI).

United Airlines (UAL) looking to buy 100+ planes from Boeing (BA) and or Airbus.

Nutanix (NTNX): WSJ article says exploring a sale.

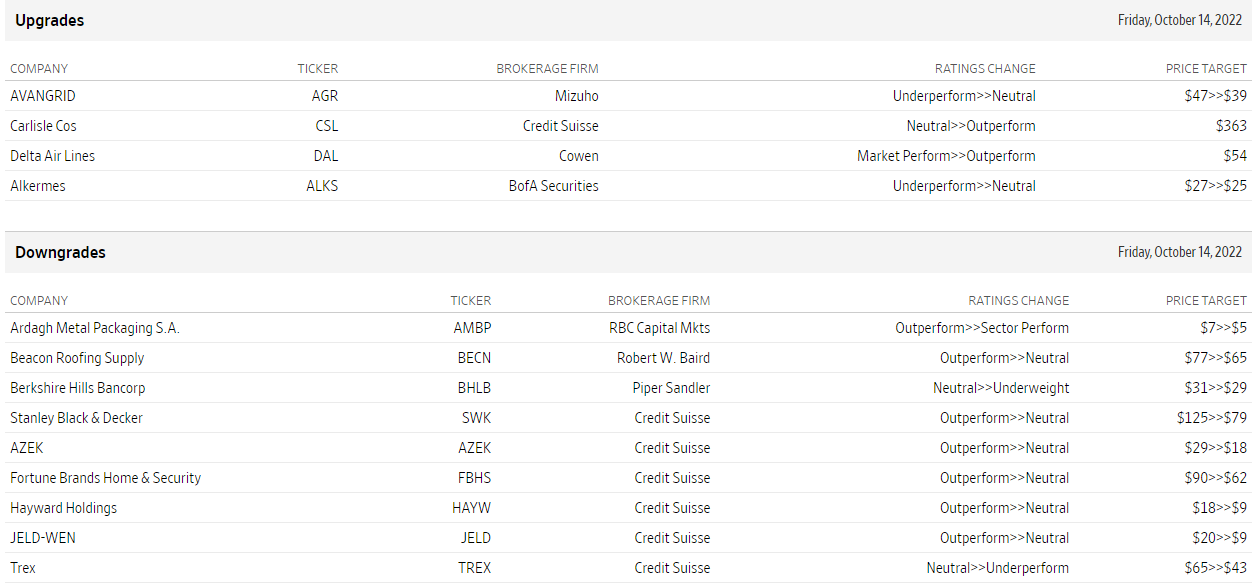

Upgrades and downgrades

Source: WSJ.com

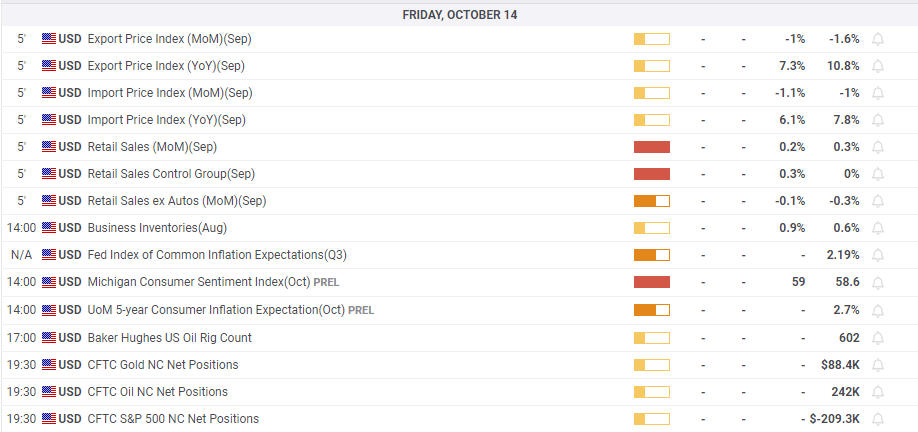

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.