Wake Up Wall Street (SPY) (QQQ): Powell pivot powers markets higher

Here is what you need to know on Thursday, December 1:

December is already upon us, and it must be time for the Santa rally then. Santa came early on Wednesday in the shape of one J. Powell, who delivered a parting gift. The Fed Chair started relatively grinch-like with talk of a higher terminal rate but left with gifts under the tree. The time to pause may come as early as December, and this good cheer lit Christmas candle fireworks under equities. The Nasdaq advanced 4.4% on the good tidings. The PCE data just out has confirmed that, and so expect equities to continue this rally.

The US Dollar, meanwhile, is still sick as it breaks 1.05 versus the Euro. The US Dollar Index moves down to 104.90. Oil is boosted by the weak US Dollar and China reopening, up another 2% to $82.30 now. Bitcoin is up to $17,100, and Gold is higher to $1,786.

European markets are mixed, FTSE and Eurostoxx are both -0.4%, but the Dax is +0.9%.

US futures are higher, S&P 500 and Dow are both +0.3%, and the Nasdaq is +0.5%.

Wall Street top news

Fed Chair Powell says the time to slow pace may be in December.

PCE shows inflation is cooling.

Reuters headlines

Dollar General Corp (DG): The company raised its annual same-store sales forecast, encouraged by strong demand for cheaper groceries and household essentials from budget-conscious shoppers amid stubbornly high inflation.

Tesla (TSLA) is set to unveil its long-delayed Semi, a 18-wheeler heavy duty vehicle.

Tesla will issue software updates for more than 435,000 vehicles in China to fix an issue with side marker lights that could in extreme circumstances lead to a collision, a regulatory body said.

Netflix (NFLX) to let more subscribers preview content - WSJ.

Salesforce Inc (CRM): The San Francisco-based company said on Wednesday that Bret Taylor would step down as co-chief executive officer in January.

Snowflake Inc (SNOW): The data cloud company on Wednesday posted a bigger quarterly loss, hit by a sharp jump in its research and development and marketing expenses.

Apple Inc (AAPL): Elon Musk on Wednesday tweeted that the misunderstanding about Twitter potentially being removed from Apple's App Store was resolved following his meeting with the iPhone maker's Chief Executive Tim Cook.

Chevron Corp (CVX): The oil major continues to work with the U.S. government to comply with sanctions on Venezuelan crude oil exports, Chief Executive Michael Wirth said on Wednesday.

Ford Motor (F): The Detroit-based carmaker will invest an extra 149 million Pounds to raise electric vehicle power unit capacity at its engine factory in northern England by 70%, as the US carmaker accelerates its push to go electric.

Ryanair Holding Plc (RYAAY) & Shell Plc: The Irish airline signed a sustainable aviation fuel supply agreement with Shell, but Chief Executive Michael O'Leary said it would take a "revolution" to hit his target of powering 12.5% of flights with the fuel by 2030.

Taiwan Semiconductor Manufacturing Co (TSM): The chipmaker will offer advanced 4-nanometer chips when its new $12-billion plant in Arizona opens in 2024.

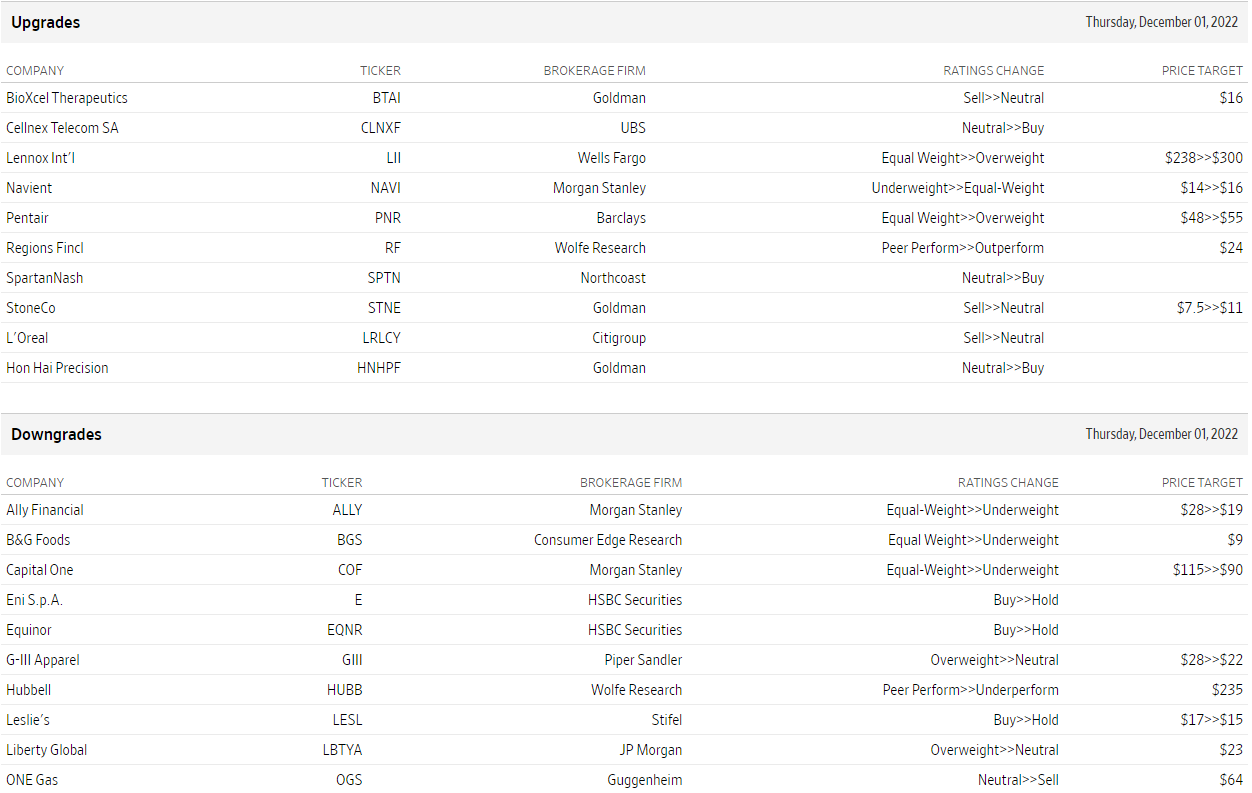

Upgrades and downgrades

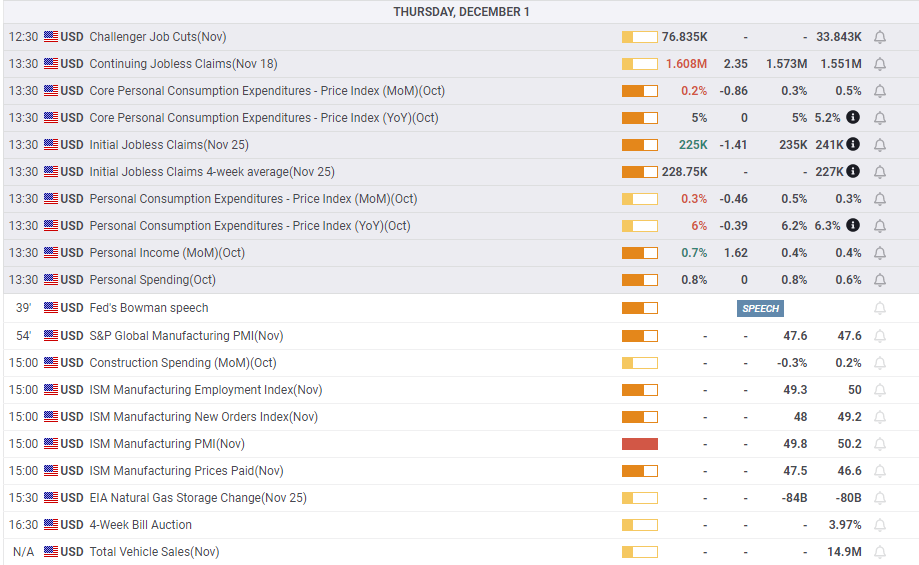

Economic releases

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.