Wake Up Wall Street (SPY) (QQQ): Equity markets continue to lose ground

Here is what you need to know on Wednesday, August 31:

Equity markets took another move lower on Tuesday despite some early optimism. That was quickly batted away by some good economic data. Yes, we are at the stage of good news is bad news for equities. The reason of course was the good news in terms of JOLTS and consumer confidence means the US economy can take another 75 basis point rate hike, and odds have now priced that as the most likely outcome for September.

Higher rates are generally not good for equity valuations, and so it proved when markets moved lower with the Nasdaq underperforming. Already this morning we have had more excessive CPI from Europe, which has seen yields move higher again and hit the European equity markets. For now, US equities are looking flat on the open, but yields have ticked a small bit higher in European trading. With all eyes beginning to turn to Friday's employment report, it is hard to see much change until then. Perhaps the only positive might be some choppy trading as risk may be curbed until then.

Oil suffered on Tuesday and again on Wednesday as old rumors resurfaced about an imminent return of Iranian oil to the market. It is likely to not be imminent, and OPEC+ will curb supply even if it does, but oil dropped notably and is down this morning on growth concerns in China. Meanwhile, Hungary has signed to take gas from Gazprom in a deal that has ramifications for the EU. Hungary has long been a thorn in the bloc, and this deal further alienates the sides.

Bitcoin is back above $20,000, Gold is at $1,711, and the dollar index is stronger at 109.

European markets are lower: Eurostoxx flat, FTSE -0.8%, and Dax -0.2%.

US futures are higher: -0.3% for the S&P, the Dow is -0.2% and the Nasdaq is -0.7%.

Wall Street top news (QQQ)(SPY)

China's top developers see sales drop nearly a third in August.

Iran's Foreign Minister is in Moscow, says he needs more guarantees from the US for the nuclear deal. Russia says it supports the deal and the cancellation of sanctions on Iran.

Bed Bath & Beyond (BBBY) is down 10% as it files to sell shares in the future.

Hewlett Packard Enterprises (HPE) up on earnings.

HP is down as revenue misses.

SNAP down on losing executives to Netflix (NFLX).

Crowdstrike (CRWD) up on earnings.

Express (EXPR) misses on revenue and cites tough conditions.

Designer Brands (DBI) is up on strong earnings.

Chewy (CHWY) slumps on cutting guidance.

Charge Point Holdings (CHPT) up on earnings.

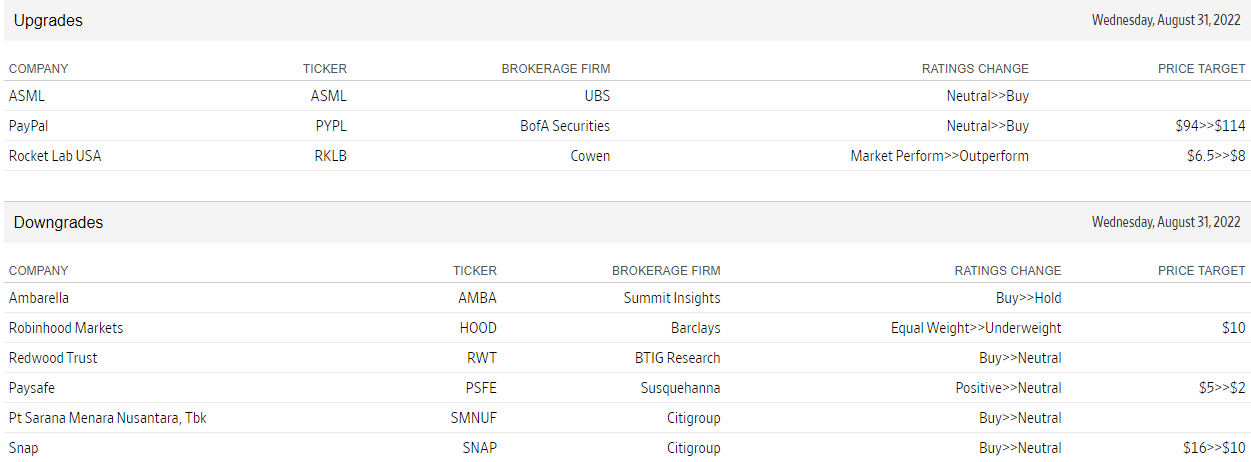

Upgrades and downgrades

Source: WSJ.com

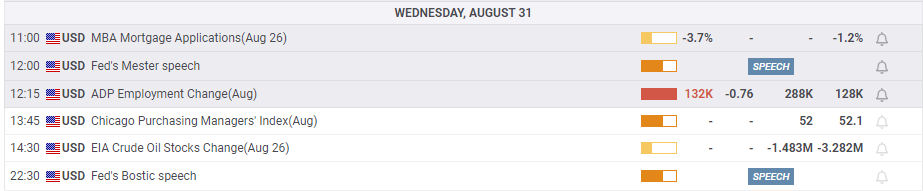

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.